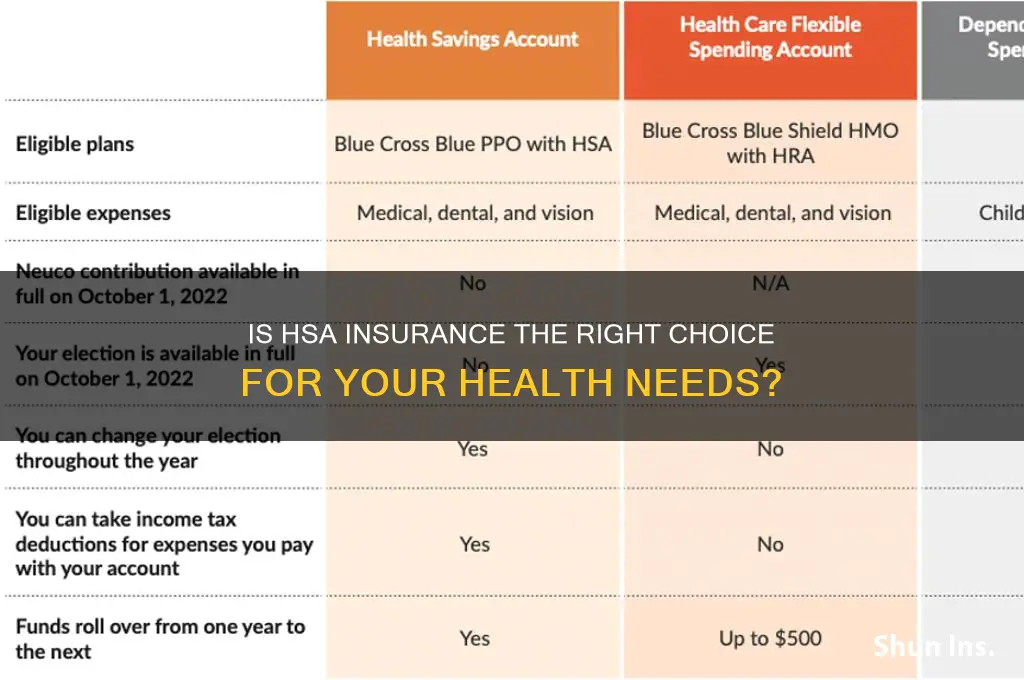

Health Savings Account (HSA)-compatible insurance plans have gained popularity for their unique combination of high-deductible health plans and tax-advantaged savings accounts. When considering whether HSA insurance is right for you, it’s essential to evaluate your healthcare needs, financial situation, and long-term goals. HSAs offer triple tax benefits—contributions are tax-deductible, funds grow tax-free, and withdrawals for qualified medical expenses are also tax-free—making them an attractive option for those who want to save for future healthcare costs while reducing taxable income. However, HSA plans typically come with higher deductibles, meaning you’ll pay more out-of-pocket before insurance coverage kicks in, which may not suit individuals who require frequent medical care. If you’re generally healthy, have the ability to save consistently, and prefer a plan that offers both immediate and long-term financial benefits, HSA insurance could be a smart choice. Conversely, if you anticipate high medical expenses or prefer lower upfront costs, you might want to explore other insurance options. Ultimately, weighing your health, budget, and savings priorities will help determine if HSA insurance aligns with your needs.

Explore related products

What You'll Learn

- Eligibility Requirements: Understand income limits, tax filing status, and other criteria for HSA qualification

- Cost Comparison: Evaluate premiums, deductibles, and out-of-pocket costs versus traditional plans

- Tax Benefits: Explore tax-free contributions, growth, and withdrawals for qualified medical expenses

- Long-Term Savings: Assess HSA as a retirement health savings tool with investment options

- Network Coverage: Check if your preferred doctors and hospitals are in-network for HSA plans

![]()

Eligibility Requirements: Understand income limits, tax filing status, and other criteria for HSA qualification

To qualify for a Health Savings Account (HSA), you must first be enrolled in a high-deductible health plan (HDHP). This isn’t just any health insurance—it’s a specific type with a minimum deductible of $1,600 for individuals or $3,200 for families in 2024. If your plan doesn’t meet these thresholds, you’re ineligible for an HSA, no matter how much you’d like to contribute. This requirement ensures that HSA users are primarily responsible for their healthcare costs before insurance kicks in, aligning with the account’s purpose of pairing savings with high-deductible coverage.

Beyond your health plan, your tax filing status plays a critical role in HSA eligibility. If you’re claimed as a dependent on someone else’s tax return, you cannot open or contribute to an HSA, even if you meet all other criteria. This rule often catches young adults still on their parents’ insurance but filing independently. Conversely, if you’re over 65, you’re no longer eligible for an HSA unless you’re enrolled in an HDHP through a spouse’s employer or your own self-employment plan. Age and dependency status are non-negotiable factors that can instantly disqualify you, regardless of income or health plan type.

Income limits do not directly determine HSA eligibility, but they influence your contribution strategy. While there’s no income cap for contributing, higher earners may face limitations on tax deductions if they exceed annual contribution limits ($4,150 for individuals, $8,300 for families in 2024). Additionally, those with incomes below certain thresholds may qualify for cost-sharing reductions under the Affordable Care Act, which can make an HDHP less appealing. For example, if your income is under 250% of the federal poverty level, you might find traditional plans with lower deductibles more cost-effective, even if they disqualify you from an HSA.

Other eligibility criteria include not being enrolled in Medicare or Tricare, and not having disqualifying additional health coverage (like a flexible spending account for medical expenses). However, dental, vision, and preventive care plans are typically allowed. A practical tip: if you’re unsure about your eligibility, use the IRS’s HSA eligibility checklist (Publication 969) or consult a tax professional. Missteps here can lead to penalties, such as taxes and a 20% fee on ineligible contributions, so accuracy is key.

Finally, consider your long-term financial goals when assessing HSA eligibility. While the triple tax advantage (tax-deductible contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses) is appealing, it’s most beneficial for those who can afford to maximize contributions and let the account grow over time. If you’re in a low-income bracket or anticipate frequent medical expenses that exceed your ability to save, an HSA might not align with your immediate needs. Eligibility is just the first step—ensuring the account fits your financial strategy is equally crucial.

Understanding SR22 Insurance Requirements in Utah: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Cost Comparison: Evaluate premiums, deductibles, and out-of-pocket costs versus traditional plans

Health Savings Account (HSA)-eligible plans often feature lower monthly premiums compared to traditional insurance, making them attractive for budget-conscious individuals. However, this savings comes with a trade-off: higher deductibles. For example, a 30-year-old might pay $200 monthly for an HSA plan with a $3,000 deductible, versus $400 for a traditional plan with a $1,000 deductible. The key is assessing your annual healthcare usage. If you rarely visit the doctor, the lower premiums could save you hundreds annually, even after accounting for the higher deductible.

When evaluating out-of-pocket costs, consider not just the deductible but also coinsurance and copays. HSA plans typically require you to pay full price for services until the deductible is met, whereas traditional plans may offer copays for doctor visits or prescriptions. For instance, a routine checkup might cost $150 out-of-pocket under an HSA plan but only $30 with a traditional plan. If you anticipate frequent medical visits, the cumulative out-of-pocket costs in an HSA plan could outweigh the premium savings.

A strategic approach to HSA plans involves maximizing tax advantages to offset costs. Contributions to an HSA are tax-deductible, grow tax-free, and can be withdrawn tax-free for qualified medical expenses. For a family contributing the maximum $7,750 annually (2023 limit), this could translate to over $2,000 in tax savings, depending on your tax bracket. Over time, these savings can build a substantial fund to cover deductibles and other expenses, effectively reducing the financial burden of higher out-of-pocket costs.

Finally, consider your long-term financial goals. HSA funds roll over indefinitely, making them a valuable tool for future healthcare expenses or even retirement. If you’re healthy and can afford to pay for occasional medical needs out-of-pocket, an HSA plan could be a wise investment. Conversely, if you prefer predictable costs and immediate coverage for routine care, a traditional plan might be more suitable. The decision hinges on balancing current affordability with future financial security.

Settling Dog Bite Claims Without Insurance: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Tax Benefits: Explore tax-free contributions, growth, and withdrawals for qualified medical expenses

One of the most compelling reasons to consider a Health Savings Account (HSA) is its unparalleled tax advantages. Unlike traditional savings accounts, HSAs offer a triple tax benefit: tax-free contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses. This unique structure can significantly enhance your financial strategy, especially if you’re mindful of healthcare costs. For instance, if you contribute $3,000 annually to your HSA and invest it in a growth-oriented fund averaging 7% returns, your account could grow to over $50,000 in 20 years—all tax-free. This makes HSAs not just a tool for covering immediate medical expenses but a long-term investment vehicle.

To maximize these benefits, it’s crucial to understand the rules governing qualified medical expenses. The IRS defines these as costs for diagnosis, cure, mitigation, treatment, or prevention of disease, including prescription medications, dental care, and even certain over-the-counter items like bandages or thermometers. Notably, expenses like cosmetic surgery or gym memberships typically don’t qualify unless prescribed by a physician. Keep detailed records of your expenses and receipts, as this documentation is essential for tax purposes and audits. For example, if you use HSA funds for non-qualified expenses, you’ll owe taxes plus a 20% penalty unless you’re over 65, in which case the penalty is waived.

Another strategic approach is to pay for current medical expenses out of pocket and let your HSA grow over time. This method allows your contributions to accumulate and compound tax-free, creating a substantial nest egg for future healthcare needs or even retirement. After age 65, you can withdraw HSA funds for any reason without penalty, though non-medical withdrawals are taxed as income. For instance, if you’ve built a $100,000 HSA balance by retirement, you could use it to cover Medicare premiums, long-term care expenses, or even everyday costs, effectively turning your HSA into a tax-efficient retirement account.

However, not everyone is eligible for an HSA. To qualify, you must be enrolled in a high-deductible health plan (HDHP) and not covered by other non-HDHP insurance. For 2023, the minimum deductible for an HDHP is $1,500 for individuals and $3,000 for families, with maximum out-of-pocket limits of $7,500 and $15,000, respectively. If you’re unsure whether an HSA aligns with your health plan, consult your insurance provider or a financial advisor. Additionally, consider your current and projected healthcare needs—if you rarely visit the doctor, an HSA paired with an HDHP could save you thousands in premiums annually.

In conclusion, the tax benefits of an HSA make it a powerful tool for both short-term healthcare savings and long-term financial planning. By understanding the rules, strategically managing contributions, and aligning your health plan with your needs, you can unlock its full potential. Whether you’re saving for immediate medical expenses or building a tax-free retirement fund, an HSA offers flexibility and advantages that few other accounts can match. If you’re eligible and proactive about healthcare costs, it’s worth exploring whether an HSA is the right choice for you.

Dodd-Frank's Impact: Transforming Insurance Industry Regulations and Practices

You may want to see also

Explore related products

![]()

Long-Term Savings: Assess HSA as a retirement health savings tool with investment options

Health Savings Accounts (HSAs) are not just for covering immediate medical expenses; they can be a powerful tool for long-term savings, particularly for retirement health costs. Unlike Flexible Spending Accounts (FSAs), HSAs allow funds to roll over indefinitely, offering a unique opportunity to grow your savings through investments. This feature transforms the HSA from a simple expense account into a potential retirement health fund, especially when paired with strategic investment options.

To maximize an HSA’s long-term potential, consider these steps: first, ensure you’re contributing the maximum allowable amount annually—$3,850 for individuals and $7,750 for families in 2023, with an additional $1,000 catch-up contribution for those over 55. Second, choose an HSA provider that offers low-fee investment options, such as mutual funds or index funds, to accelerate growth. For example, investing in a target-date fund aligned with your retirement age can provide a hands-off, diversified approach. Third, treat your HSA as a dedicated retirement health account, avoiding withdrawals for non-essential expenses to allow compound interest to work its magic.

A key advantage of HSAs is their triple tax benefit: contributions are tax-deductible, earnings grow tax-free, and withdrawals for qualified medical expenses are also tax-free. This makes HSAs more tax-efficient than traditional retirement accounts like 401(k)s or IRAs, particularly for healthcare costs, which are projected to consume a significant portion of retirement income. For instance, a 65-year-old couple retiring in 2022 is estimated to need $315,000 for healthcare expenses, according to Fidelity Investments. An HSA can help bridge this gap.

However, there are cautions to consider. Not all HSA providers offer robust investment options, and some may charge high fees that erode returns. Additionally, while HSAs can be used for non-medical expenses after age 65 without penalty, such withdrawals are subject to income tax, reducing their efficiency as a retirement tool. To avoid this, focus on using HSA funds exclusively for healthcare in retirement, allowing other retirement accounts to cover living expenses.

In conclusion, an HSA’s investment capabilities make it a compelling option for long-term health savings, particularly for retirement. By contributing maximally, choosing the right provider, and adopting a disciplined investment strategy, individuals can build a substantial fund to offset future healthcare costs. While it requires careful planning and a long-term perspective, an HSA can be a cornerstone of a comprehensive retirement strategy, ensuring financial security in later years.

Insuring a Concrete Boat: Essential Tips for Unique Vessel Coverage

You may want to see also

Explore related products

![]()

Network Coverage: Check if your preferred doctors and hospitals are in-network for HSA plans

One of the first steps in determining if an HSA-compatible insurance plan is right for you is to verify whether your trusted healthcare providers are in-network. In-network providers have agreed to discounted rates with your insurance company, which can significantly reduce out-of-pocket costs. Start by compiling a list of your current doctors, specialists, and hospitals. Then, cross-reference this list with the plan’s provider directory, typically available on the insurer’s website. If your preferred providers are not in-network, you’ll face higher costs, potentially negating the savings an HSA offers. This step is non-negotiable for anyone considering an HSA plan, as network coverage directly impacts both financial and healthcare continuity.

For those with chronic conditions or ongoing treatments, in-network coverage becomes even more critical. For example, if you see a specialist regularly, such as an endocrinologist for diabetes management, ensure they are in-network to avoid paying full price for visits. Similarly, if you have a preferred hospital for procedures or emergencies, confirm its status. Some HSA plans have narrow networks, limiting options to specific providers or facilities. If your preferred providers are out-of-network, calculate the potential cost difference and weigh it against the tax benefits of an HSA. Tools like the insurer’s provider search portal or a call to customer service can clarify coverage details.

A practical tip is to prioritize flexibility if you’re unsure about future healthcare needs. Some HSA-compatible plans, like PPOs, offer out-of-network coverage at a higher cost, providing a safety net if your preferred providers aren’t included. However, HDHPs (High-Deductible Health Plans) paired with HSAs often have HMO-style networks, which require in-network care except in emergencies. If you’re open to switching providers, use this as an opportunity to explore highly-rated in-network options. Websites like Healthgrades or Vitals can help you find reputable in-network doctors based on patient reviews and specialties.

Finally, consider the long-term implications of network coverage. If you’re planning to start a family, for instance, ensure obstetricians and pediatricians are in-network. Similarly, if you’re over 50, verify that geriatric specialists or facilities are covered. Network changes can occur annually, so review your plan during open enrollment to confirm continued coverage. While an HSA’s tax advantages are appealing, they’re only worthwhile if the plan’s network aligns with your healthcare needs. Skipping this step could lead to unexpected expenses, undermining the very savings an HSA is designed to provide.

Burying a Loved One in Chicago Without Insurance: A Practical Guide

You may want to see also

Frequently asked questions

HSA (Health Savings Account) insurance pairs a high-deductible health plan (HDHP) with a tax-advantaged savings account. You contribute pre-tax dollars to the HSA, which can be used to pay for qualified medical expenses. The HDHP typically has lower premiums but higher out-of-pocket costs until the deductible is met.

To be eligible for an HSA, you must be enrolled in a qualified high-deductible health plan (HDHP), not be covered by other non-HDHP health insurance, not be enrolled in Medicare, and not be claimed as a dependent on someone else’s tax return.

Yes, HSA insurance can be a good fit if you’re generally healthy and don’t anticipate frequent medical expenses. The lower premiums of an HDHP can save you money, and you can build up your HSA for future healthcare needs or even use it as a retirement savings tool.

While you can use HSA funds for non-medical expenses, doing so before age 65 triggers taxes and a penalty. After age 65, you can use HSA funds for any purpose without penalty, though non-medical expenses will be taxed as income.

Your HSA is portable, meaning it stays with you even if you change jobs, insurance plans, or retire. You can continue to use the funds for qualified medical expenses regardless of your employment or insurance status.