Income protection insurance is a type of insurance that pays you a regular income if you can't work due to illness, injury, or disability. It is designed to protect your income and help cover essential living costs such as rent, mortgage payments, and bills. The policy covers a set percentage of your existing gross annual salary, typically between 50-70%. Whether income protection insurance is worth it depends on individual circumstances, such as how likely one is to experience an illness or injury that prevents them from working, and whether they can cover their monthly costs if they are unable to work.

| Characteristics | Values |

|---|---|

| Purpose | To provide financial security in the event of sudden illness or injury |

| Coverage | Varies; typically between 50-70% of income; some policies offer up to 90% for the first six months |

| Cost | Varies depending on age, health, job type, medical history, and lifestyle; can be as low as £10 per month |

| Payout Period | Typically 2-5 years, but some policies offer payments up to a specific age, e.g., 65 |

| Waiting Period | Varies; typically between two weeks to two years; some insurers offer immediate or day-one cover |

| Exclusions | Intentional self-harm, pregnancy (unless disability lasts more than 90 days after), not following medical advice |

| Alternatives | Mortgage protection, critical illness cover, life insurance, disability insurance |

| Considerations | Risk assessment, ability to cover costs without insurance, likelihood of claiming |

Explore related products

$6.99

What You'll Learn

![]()

Cost of living

Income protection insurance is a policy that covers you if you cannot work due to sickness, injury or disability. When you make a claim, your insurer pays you a regular income until you return to work or retire, or for a fixed period. This can help cover essential living costs such as mortgage or rent and bills, reducing the financial strain on you and your family.

The cost of living is an important consideration when taking out an income protection policy. While working, you would expect your salary to increase over time to keep up with the rising cost of living. However, an income protection policy that pays out a fixed proportion of your salary today may not account for future rises, and the amount you receive will be worth less and less over the years. To address this, you can add an 'index-link' to your income protection, allowing it to increase with a measure of inflation, such as the Consumer Prices Index (CPI) or the Retail Prices Index (RPI). This ensures that your income protection keeps pace with the rising cost of living, maintaining its value over time.

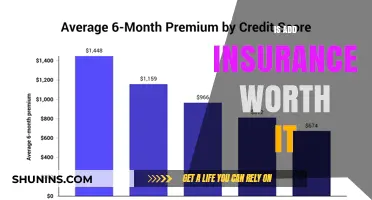

The cost of income protection insurance varies depending on individual circumstances, with factors such as age, health, job type, and waiting period influencing the monthly premium. Older individuals, those in riskier professions, and those with pre-existing health conditions can expect to pay higher premiums. The length of the waiting period before payments start also affects cost, with longer waiting periods resulting in lower premiums.

When considering income protection insurance, it is essential to carefully review the policy details. Understand the waiting period, the proportion of income covered, and any limitations or exclusions. Additionally, be aware of the difference between standard and guaranteed premium policies. Standard policies allow the insurer to increase premiums over time, while guaranteed premiums remain fixed.

While income protection insurance provides peace of mind and financial security, it is not the only option. Alternatives include critical illness cover, which provides a lump sum for specific illnesses, and life insurance, which supports your loved ones financially if you pass away. Additionally, mortgage protection insurance covers your mortgage payments if you become unable to afford them due to illness, injury, or redundancy.

In conclusion, income protection insurance can be worth it for individuals seeking financial security and peace of mind. However, it is crucial to carefully consider the specific policy details, alternative options, and the potential impact of the rising cost of living on the value of the payouts.

The Safety Net: Crop Insurance and Its Vital Role for Farmers

You may want to see also

Explore related products

![]()

Policy exclusions

Income protection insurance is a type of insurance that pays you a regular, tax-free income if you become unable to work due to injury, illness, or other factors, like job loss. It is designed to cover your living costs, such as mortgage or rent payments, groceries, childcare, and more.

However, it is important to note that income protection insurance does not cover all possible scenarios. There are several policy exclusions that you should be aware of before purchasing this type of insurance. Here are some common policy exclusions:

- Pre-existing medical conditions: Income protection insurance typically does not cover pre-existing medical conditions. This means that if you have a medical condition before purchasing the insurance, any future claims related to that condition may be denied.

- Intentional self-harm and attempted suicide: Most policies exclude coverage for injuries or illnesses resulting from intentional self-harm or attempted suicide. This exclusion is intended to discourage people from harming themselves intentionally to claim insurance benefits.

- Pregnancy and related complications: Pregnancy and related complications are usually not covered by income protection insurance. However, some policies may provide coverage if the disability resulting from pregnancy lasts for an extended period, such as 90 days or more.

- Redundancy and job loss: Income protection insurance generally does not cover redundancy or job loss. If you lose your job, you will not be able to claim income protection benefits. In such cases, you may need to consider alternative types of insurance, such as unemployment cover.

- High-risk activities and hobbies: If you engage in high-risk activities or hobbies, such as bungee jumping, motorsports, or skydiving, your policy may exclude coverage for injuries sustained while participating in these activities. Insurers consider these activities to have a higher likelihood of resulting in a claim, and therefore, they are often excluded from coverage.

- Non-disclosure or misrepresentation: If you do not disclose relevant information or misrepresent your circumstances when taking out the policy, your insurer may deny any future claims. It is crucial to be honest and provide accurate information to ensure the validity of your policy and coverage.

It is important to carefully review the terms and conditions of any income protection insurance policy before purchasing it. Each insurance company may have different exclusions, and understanding these exclusions will help you make an informed decision about the level of coverage that is appropriate for your specific needs and circumstances.

Reporting Insurance Fraud: Tennessee's Guide

You may want to see also

Explore related products

![]()

Risk factors

Income protection insurance is a policy that pays out a regular, tax-free income if you can't work due to illness, injury, or disability. It is designed to cover essential living costs such as mortgage or rent, bills, and other everyday costs. The policy usually pays out between 50% to 70% of your income until you return to work, retire, or pass away.

- Age: The older you are, the more you will have to pay for income protection insurance, as your risk of getting ill increases.

- Health: If you are in good health, you will pay less for income protection insurance. Pre-existing conditions are typically not covered.

- Job type: If you have a risky or physically demanding job, you will likely pay more for income protection insurance.

- Hobbies and lifestyle: Dangerous hobbies, smoking, and heavy drinking can increase the cost of income protection insurance.

- Waiting period: The longer you can wait before making a claim, the cheaper your premiums will be.

- Ability to work: If you are unable to do any kind of work, you are more likely to receive a payout, but there is a higher risk of the policy not paying out.

- Inflation: Income protection policies that do not account for future salary increases due to inflation may result in lower payouts over time.

- Redundancy: Income protection insurance does not cover redundancy or being sacked from a job.

- Alternative sources of income: If you have substantial savings or sufficient sick pay from your employer, income protection insurance may not be necessary.

The Farmers Insurance Signal App: Understanding Reset Scenarios

You may want to see also

Explore related products

![Property and Casualty Insurance License Exam Study Guide: Property Casualty Insurance Book and Practice Test Questions [3rd Edition]](https://m.media-amazon.com/images/I/71MhA+5nDML._AC_UY218_.jpg)

![]()

Alternatives

If you're unsure about taking out income protection insurance, there are several alternatives to consider. Here are some options:

Savings

It is recommended to have enough money saved to cover at least three months' worth of living expenses in case of emergencies. However, savings can quickly disappear if you're out of work for an extended period. Therefore, you should consider whether your savings would sufficiently cover you if you were unable to work and whether you are comfortable using them.

Employer's Sick Pay Package

If your employer offers a generous sick pay package, you may not need income protection insurance. It is worth checking your employment contract to understand the details of your employer's sick pay policy. Some employers provide full pay for up to a year, while others offer a combination of full and half pay before reducing sick pay to the statutory minimum.

Mortgage Protection

Mortgage protection insurance covers your mortgage payments if you can no longer afford them due to illness, serious injury, or redundancy. This type of insurance ensures that you can keep up with your mortgage payments without dipping into your savings or other income sources.

Critical Illness Cover

Critical illness insurance provides a lump sum payout if you are diagnosed with certain serious illnesses or disabilities. This type of insurance can help cover medical expenses or other financial needs during your treatment and recovery. It is often recommended for those with dependents or a mortgage to ensure financial protection.

Life Insurance

Life insurance provides financial support to your loved ones in the event of your death. It can be used to cover outstanding debts, such as a mortgage, or provide ongoing financial support to your family. Life insurance can be set up to pay into a trust to cover inheritance tax (IHT) bills, but it is recommended to seek legal and financial advice before doing so.

Unemployment Cover

If you're concerned about job loss, unemployment cover is an alternative to income protection insurance. This type of insurance provides a replacement income if you lose your job, helping you to cover your living expenses until you find new employment.

Remember, when considering alternatives to income protection insurance, it is important to carefully assess your financial situation, including your income, expenses, and any existing coverage you may have. Seeking advice from an independent financial adviser or insurance broker can help you make informed decisions about your protection needs.

Understanding Your Insurance Report: A Guide

You may want to see also

Explore related products

$14.99

![]()

Payouts

Income protection insurance is designed to cover you while you're still alive, so if your family relies on your income, it's important to consider how your family would cope long-term if you were to pass away. It's a type of insurance that pays you a regular, tax-free income if you can't work due to illness, injury, or disability.

The payout you receive from income protection insurance is typically a percentage of your income, ranging from 50% to 70% of your existing gross annual salary. The benefit period, or the length of time the insurer will provide monthly payments, is often two to five years, but some policies may continue payments up to a specific age, such as 65. The monthly benefit received can be used to cover essential living costs, such as rent or mortgage payments, groceries, utilities, and medical costs.

In the United States, income protection insurance is commonly referred to as disability insurance, and it serves the same purpose as income protection insurance found in countries like the UK, Australia, and New Zealand. It is important to note that income protection insurance does not typically cover redundancy or being fired from a job; separate coverage, such as unemployment insurance, is needed for those situations. Additionally, income protection insurance does not usually cover pregnancy or complications from pregnancy unless the disability lasts for an extended period after the pregnancy.

The cost of income protection insurance varies depending on individual circumstances, but it can be as low as £10 or even $1 per day. Factors influencing the cost include age, health, job type, income, medical history, and lifestyle choices. The waiting period before receiving benefits can also impact the cost, with shorter waiting periods resulting in higher premiums.

While income protection insurance can provide financial peace of mind, it is important to carefully consider your personal circumstances, such as your likelihood of experiencing an illness or injury that prevents you from working, and whether you can cover your monthly expenses if you are unable to work.

Activating Gap Insurance: A Comprehensive Guide for Farmers Insurance Policyholders

You may want to see also

Frequently asked questions

Income protection insurance pays you a regular, tax-free income if you can’t work due to illness, injury, or disability. It is sometimes called IP cover.

Income protection insurance is worth considering if your household relies on your income to pay the bills and living costs. It is also worth considering if you have a high-paying, specialized job, or if you have dependents who rely on your income.

The cost of income protection insurance varies depending on factors such as your age, income, job type, medical history, and lifestyle. It can cost as little as £10 or $1 per day.

Some alternatives to income protection insurance include mortgage protection, critical illness cover, life insurance, and unemployment cover.