Indemnity health insurance is a type of coverage that pays a fixed amount to the policyholder or their healthcare provider when a covered service is used. This differs from other types of health insurance, such as preferred provider organizations (PPOs) or health maintenance organizations (HMOs), which typically involve more complex networks of providers and variable costs based on usage. Indemnity plans are often chosen for their simplicity and predictability, as policyholders know exactly how much they will receive for each service. However, they may also come with higher premiums and less flexibility in terms of provider choice. When considering whether indemnity health insurance is better, it's important to weigh these factors against individual needs and preferences.

Explore related products

What You'll Learn

- Cost Comparison: Indemnity vs. other types of health insurance plans

- Coverage Flexibility: How indemnity plans allow for out-of-network care

- Claim Process: Steps involved in filing claims with indemnity insurance

- Provider Choice: Freedom to choose healthcare providers with indemnity plans

- Premium Factors: What affects the cost of indemnity health insurance premiums

![]()

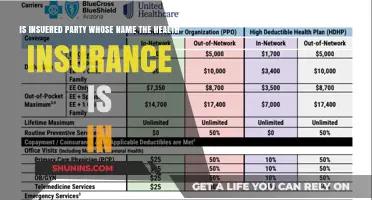

Cost Comparison: Indemnity vs. other types of health insurance plans

Indemnity health insurance plans often stand out due to their unique cost structure compared to other types of health insurance. Unlike managed care plans, such as HMOs (Health Maintenance Organizations) and PPOs (Preferred Provider Organizations), which typically involve fixed premiums and copayments, indemnity plans reimburse policyholders for a percentage of their actual medical expenses. This reimbursement model can lead to significant cost differences, especially for individuals with high healthcare needs.

One of the primary advantages of indemnity plans is their flexibility. Policyholders can choose any healthcare provider they prefer, without being restricted to a network of approved providers. This freedom can be particularly beneficial for individuals who require specialized care or have specific medical needs that may not be adequately covered by managed care plans. However, this flexibility comes at a cost. Indemnity plans often have higher premiums and may require policyholders to pay a larger portion of their medical bills upfront, which can be a financial burden for some individuals.

In contrast, managed care plans typically offer lower premiums and more predictable out-of-pocket costs. These plans often have negotiated rates with healthcare providers, which can result in significant savings for policyholders. Additionally, managed care plans may include preventive care services and wellness programs at little or no additional cost, which can help individuals maintain their health and potentially reduce their overall healthcare expenses.

When comparing the costs of indemnity plans to other types of health insurance, it's essential to consider the total cost of care, including premiums, deductibles, coinsurance, and copayments. While indemnity plans may have higher premiums, they can also provide more comprehensive coverage and greater flexibility in choosing healthcare providers. Managed care plans, on the other hand, may offer lower premiums but could limit access to certain providers and services.

Ultimately, the decision between an indemnity plan and other types of health insurance depends on an individual's specific healthcare needs, budget, and preferences. For those who prioritize flexibility and comprehensive coverage, an indemnity plan may be the better choice, despite the potentially higher costs. However, for individuals who are looking for more predictable out-of-pocket expenses and are willing to accept some limitations on provider choice, managed care plans may offer a more cost-effective solution.

Health Insurance Coverage for Paranoid Personality Disorder: What You Need to Know

You may want to see also

Explore related products

![]()

Coverage Flexibility: How indemnity plans allow for out-of-network care

Indemnity health insurance plans offer a unique advantage in the form of coverage flexibility, particularly when it comes to out-of-network care. Unlike managed care plans that restrict you to a specific network of healthcare providers, indemnity plans allow you to seek medical attention from any licensed provider, regardless of whether they are in-network or out-of-network. This flexibility can be especially beneficial for individuals who live in rural areas or have specialized medical needs that may not be adequately met by in-network providers.

One of the key benefits of indemnity plans is that they typically do not require you to choose a primary care physician (PCP) or obtain a referral to see a specialist. This means that you have the freedom to seek care from any provider you choose, without having to navigate through a gatekeeper system. Additionally, indemnity plans often cover a wider range of healthcare services, including alternative and complementary therapies, which may not be covered by managed care plans.

However, it's important to note that while indemnity plans offer greater flexibility, they may also come with higher out-of-pocket costs. Since out-of-network providers are not contracted with the insurance company, they may charge higher rates, and you may be responsible for paying the difference between the provider's charge and the insurance company's allowed amount. Furthermore, indemnity plans may have a higher deductible and coinsurance, which can increase your overall healthcare expenses.

Despite these potential drawbacks, indemnity plans can be an excellent choice for individuals who value flexibility and choice in their healthcare. If you are considering an indemnity plan, it's important to carefully review the policy details, including the coverage limits, exclusions, and out-of-pocket costs, to ensure that it meets your specific healthcare needs and budget.

Exploring the Essentials: Health Insurance in South Africa

You may want to see also

Explore related products

![]()

Claim Process: Steps involved in filing claims with indemnity insurance

Filing a claim with indemnity insurance involves several key steps that policyholders must follow to ensure a smooth and successful process. The first step is to notify the insurance company of the claim as soon as possible after the incident or loss occurs. This notification can typically be done through the company's website, mobile app, or by contacting their customer service department directly. It is important to provide accurate and detailed information about the claim, including the date and nature of the incident, as well as any relevant documentation such as police reports, medical bills, or repair estimates.

Once the claim has been reported, the insurance company will assign an adjuster to investigate and assess the claim. The adjuster may request additional information or documentation, and may also schedule an inspection of the damaged property or a medical examination of the claimant. It is crucial to cooperate fully with the adjuster and provide any requested information promptly to avoid delays in the claim process.

After the investigation is complete, the insurance company will determine the amount of the claim payment based on the policy terms and the evidence provided. If the claim is approved, the payment will be issued to the claimant, typically within a few weeks. However, if the claim is denied, the claimant will be notified in writing of the reason for the denial and may have the option to appeal the decision.

Throughout the claim process, it is important for policyholders to keep detailed records of all communications with the insurance company, including phone calls, emails, and letters. This documentation can be helpful in case of any disputes or issues that arise during the claim process. Additionally, policyholders should carefully review their policy terms and conditions to ensure they understand their rights and responsibilities when filing a claim.

In conclusion, the claim process for indemnity insurance involves several important steps, including notifying the insurance company, cooperating with the adjuster, and keeping detailed records of all communications. By following these steps and understanding their policy terms, policyholders can help ensure a smooth and successful claim process.

Medicaid Insurance Options in Oklahoma: What's Covered?

You may want to see also

Explore related products

$17.99

$8.99 $17.99

![]()

Provider Choice: Freedom to choose healthcare providers with indemnity plans

One of the key advantages of indemnity health insurance plans is the freedom they offer in choosing healthcare providers. Unlike managed care plans that often restrict you to a specific network of providers, indemnity plans typically allow you to visit any licensed healthcare professional or facility. This flexibility can be particularly beneficial for individuals who have established relationships with certain doctors or who require specialized care that may not be readily available within a managed care network.

However, this freedom comes with certain trade-offs. Indemnity plans often have higher premiums and out-of-pocket costs compared to managed care plans. Additionally, while you have the freedom to choose your providers, you may also bear more responsibility for ensuring that the care you receive is covered under your plan. This means that it's essential to carefully review your policy's terms and conditions to understand what services are covered and what your financial responsibilities may be.

When considering an indemnity plan, it's also important to think about the potential impact on your healthcare costs. While the ability to choose any provider may seem appealing, it could lead to higher overall expenses if you frequently visit out-of-network providers or require expensive treatments. On the other hand, if you are generally healthy and only require routine check-ups and preventive care, an indemnity plan could offer a cost-effective solution by allowing you to choose providers based on factors such as location and convenience rather than network participation.

Ultimately, the decision of whether an indemnity plan is right for you will depend on your individual healthcare needs, preferences, and budget. If provider choice is a top priority for you, an indemnity plan may be an excellent option. However, it's crucial to weigh this benefit against the potential drawbacks and to carefully compare indemnity plans with other types of health insurance to find the best fit for your unique situation.

Does Freedom Health Insurance Cover Cataract Surgery?

You may want to see also

![]()

Premium Factors: What affects the cost of indemnity health insurance premiums

Several factors can influence the cost of indemnity health insurance premiums. One significant factor is the policyholder's age. Younger individuals typically pay lower premiums due to their lower risk of health issues, while older individuals may face higher premiums as they are more likely to require medical attention. Another factor is the policyholder's health status. Those with pre-existing conditions or a history of health problems may be charged higher premiums, as they present a greater risk to the insurer.

The level of coverage chosen also affects premium costs. Policies with higher coverage limits or additional benefits, such as prescription drug coverage or dental care, will generally have higher premiums. The deductible amount selected can also impact premium costs, with lower deductibles typically resulting in higher premiums.

The policyholder's lifestyle choices can also play a role in determining premium costs. For example, smokers may face higher premiums due to the increased health risks associated with tobacco use. Additionally, individuals who engage in high-risk activities, such as extreme sports, may also see higher premiums.

It's important to note that premium costs can vary significantly between different insurance providers. Shopping around and comparing quotes from multiple insurers can help policyholders find the most affordable coverage that meets their needs.

Deer-Related Accidents: Will Your Insurance Rates Spike?

You may want to see also

Frequently asked questions

Indemnity health insurance is a type of insurance plan where the insurer pays the policyholder directly for each out-of-pocket medical expense, up to the policy's limits, rather than paying the healthcare provider.

Unlike managed care plans, such as HMO or PPO, which require you to use a network of approved providers and often involve copays and deductibles, indemnity plans offer more flexibility in choosing healthcare providers but typically require you to pay all medical bills upfront and then file a claim for reimbursement.

The main advantages of indemnity health insurance include the freedom to choose any healthcare provider, the ability to see specialists without a referral, and potentially lower premiums compared to managed care plans. Additionally, indemnity plans often cover a wider range of medical expenses.

The disadvantages of indemnity health insurance include the requirement to pay all medical bills upfront, which can be financially burdensome, and the need to file claims manually, which can be time-consuming. Additionally, indemnity plans may have higher out-of-pocket costs and less predictable coverage compared to managed care plans.

Whether indemnity health insurance is better depends on your individual needs and preferences. If you value flexibility in choosing healthcare providers and are willing to manage your own claims and out-of-pocket expenses, indemnity insurance might be a good fit. However, if you prefer lower upfront costs and more predictable coverage, managed care plans might be a better option.