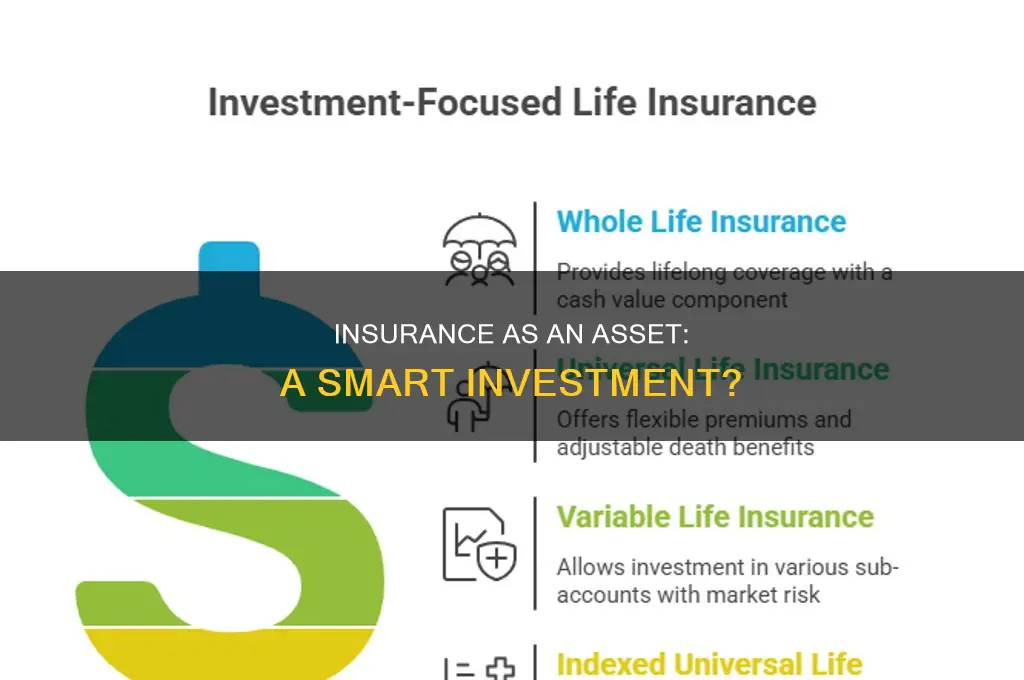

Insurance is a legal contract that provides financial protection against unexpected losses, accidents, injuries, or property damage. It helps individuals protect their assets, health, homes, and automobiles. Life insurance, in particular, can be considered an asset if it accumulates cash value or is converted into cash. Permanent life insurance policies, such as whole life and universal life insurance, offer the potential for cash value accumulation, making them more likely to be considered assets. On the other hand, term life insurance does not typically build cash value and is less likely to be viewed as an asset. It's important to note that the classification of insurance as an asset or liability can depend on various factors, including the type of policy, net worth, and individual financial goals.

| Characteristics | Values |

|---|---|

| Type of insurance policy | Term life insurance and permanent life insurance offer different options for coverage. |

| Accumulation of cash value | Permanent life insurance accumulates cash value, while term life insurance does not. |

| Tax advantages | Whole life insurance policies can be used as tax shelters, allowing individuals to avoid capital gains taxes. |

| Investment aspect | Whole life insurance policies have an investment component, allowing for the accumulation of cash value over time. |

| Loan collateral | Life insurance policies can be used as collateral for loans, providing a source of funding without selling assets. |

| Withdrawals | Some policies allow for withdrawals, providing access to funds without taking on debt. |

| Payout upon maturity | Insurance policies can provide a lump-sum payout upon maturity or in the event of a covered risk, such as critical illness or death. |

| Financial protection | Insurance protects against unexpected financial losses, covering medical bills, damage to property, and lawsuits. |

Explore related products

What You'll Learn

- Life insurance can be an asset if it accumulates cash value

- Permanent life insurance is an asset as it covers you for your whole life

- Whole life insurance is an asset for the ultra-wealthy

- Universal life insurance is an asset as it allows policyholders to grow an asset by accruing interest

- Insurance becomes an asset when a risk covered in the plan is activated or when the plan matures

![]()

Life insurance can be an asset if it accumulates cash value

Life insurance is a product that provides financial protection against unexpected losses resulting from accidents, injuries, or property damage. While it is not typically considered an asset, certain types of life insurance policies can be used as one.

Life insurance policies that accumulate cash value are considered assets because the policyholder can access this cash value while they are alive. This cash value grows over time at a minimum guaranteed rate indicated by the policy. Whole life insurance and universal life insurance are two examples of permanent life insurance policies that allow policyholders to build cash value. A portion of the premium paid every month is put into a cash value account, allowing the policyholder to grow an asset by accruing interest over time.

The cash value of a life insurance policy can be used to borrow against, used as collateral for a loan, or withdrawn. It can also help protect wealth and transfer it to heirs. However, accessing the cash value of a life insurance policy may reduce the death benefit and available cash surrender value, and there may be surrender charges and taxes involved.

It is important to note that term life insurance policies, which are generally less expensive and valid for a set number of years, do not offer the ability to accumulate cash value and, therefore, do not serve as assets.

In summary, life insurance can be an asset if it accumulates cash value that the policyholder can access. This cash value can provide financial benefits during the lifetime of the policyholder, in addition to the death benefit provided by the life insurance policy.

Borrowing Against Meritus Life Insurance: Is It Possible?

You may want to see also

Explore related products

$3.7 $14.95

$62.67 $85.99

$75.35 $85.99

![]()

Permanent life insurance is an asset as it covers you for your whole life

Insurance is a means of protection against unexpected financial losses. It is a contract in which an insurance company indemnifies the insured against covered losses from specific risks. The most common types of insurance include life, health, homeowners, and auto insurance.

Life insurance is a financial asset that can be used to protect your wealth and transfer it to your heirs. It can provide a death benefit to your family and loved ones, which can be used to reduce their risk of financial hardship. Term life insurance policies are temporary and do not have an accessible cash value during the policyholder's lifetime. On the other hand, permanent life insurance provides lifelong coverage and can be an asset as it accumulates cash value over time.

Permanent life insurance policies, such as whole life and universal life insurance, have a savings component that allows the policyholder to build cash value. This cash value can be accessed during the policyholder's lifetime, providing funds for retirement or other financial goals. The cash value grows over time, either at a guaranteed minimum rate or by accruing interest or investment returns. It is important to note that accessing the cash value may reduce the death benefit and available cash surrender value and may incur fees or taxes.

Permanent life insurance is an asset because it covers you for your whole life and provides additional benefits beyond traditional term life insurance. The cash value component can be used to borrow against, supplement retirement savings, or meet other financial goals. It offers the advantage of lifelong coverage, ensuring financial protection for your loved ones regardless of how long you live. The ability to accumulate and access cash value within a permanent life insurance policy makes it a valuable asset that can improve your financial health and security.

Ending Life: Insurance Money Payouts Explained

You may want to see also

Explore related products

![]()

Whole life insurance is an asset for the ultra-wealthy

Insurance is a way to manage your financial risks. When you buy insurance, you purchase protection against unexpected financial losses. The insurance company indemnifies you or someone you choose against covered losses from specific contingencies. Most people have insurance, whether that's for their vehicle, home, or life.

Whole life insurance is a type of permanent life insurance that offers the policyholder the ability to accumulate cash value. This works because a portion of the premium you pay every month goes into a cash value account. This cash value account accumulates over time at a minimum guaranteed rate indicated by your policy. The premiums on these policies typically won't increase over the life of the policy. Whole life insurance is an asset for the ultra-wealthy because it can be used as a tool to skirt around normal rules with insurance and investment products. It is a means to protect your assets and your financial health. It can also be used as an investment tool with tax benefits when you're still alive.

Whole life insurance is an asset because it can be used as collateral for a loan, and you can withdraw funds or receive "accelerated benefits" or cash out the policy. The cash value of whole life insurance can be used to help protect wealth and transfer it to heirs. The cash value provides funds that can be used during retirement, when life insurance needs may decrease.

Whole life insurance is also an asset because it can be used to maximize the after-tax estate and have more money to pass on to heirs. Life insurance death benefits are income-tax-free to your beneficiary, which could be appealing to an individual with a higher net worth who wants to provide an inheritance that doesn't create an extra tax burden. Life insurance can be a useful financial tool for high-net-worth individuals.

Understanding Insurance Responsibility for Adult Children

You may want to see also

Explore related products

![]()

Universal life insurance is an asset as it allows policyholders to grow an asset by accruing interest

Life insurance is a means of protecting your assets, your financial health, and your family's financial health. It is not an asset in and of itself. However, some forms of life insurance, such as permanent life insurance, can be considered an asset because they allow policyholders to build cash value over time. This cash value can be accessed during the policyholder's lifetime, and it can grow through interest accrual.

Universal life insurance is a type of permanent life insurance that functions similarly to whole life insurance. It allows policyholders to grow an asset by accruing interest over time. This interest is credited to the policyholder's account, and the cash value of the policy grows in tandem with it. Policyholders can also borrow against or cash in their savings portion, which grows tax-deferred over their lifetime.

The flexibility of universal life insurance policies makes them a powerful financial tool. Policyholders can adjust their premiums and death benefits to suit their needs and financial strategies. Additionally, universal life insurance policies offer the potential for higher returns through variable universal life policies, where earnings can be invested in accounts of the policyholder's choosing, such as mutual funds or the stock market.

However, it is important to note that universal life insurance policies come with certain risks. The interest rates are not guaranteed and can change frequently. If the investments underperform or the policy is underfunded, the cash value may not grow as expected, and the policy could lapse. Therefore, policyholders must carefully consider their options and seek guidance from insurance or financial professionals before choosing a universal life insurance policy.

In conclusion, universal life insurance can be considered an asset as it enables policyholders to grow their wealth by accruing interest and provides access to that accrued wealth during their lifetime. However, it is essential to understand the associated risks and structure the policy appropriately to maximize its benefits.

Life Insurance Rates: AARP's Affordable Plans for Seniors

You may want to see also

Explore related products

![]()

Insurance becomes an asset when a risk covered in the plan is activated or when the plan matures

Insurance is a means of protection against unexpected financial losses, and it can be considered a contract between the insurer and the insured. While insurance is not typically considered an asset, it can become one in certain situations.

Firstly, insurance becomes an asset when a risk covered in the plan is activated. For example, if an unforeseen illness results in a critical illness, disability, or death, the insurance policy becomes an asset as it provides financial protection and allows the policyholder to make a claim and receive a payout. This payout can help cover expenses, maintain the standard of living for surviving family members, and repay any debts incurred.

Secondly, insurance can become an asset when the plan matures. Permanent life insurance policies, such as whole life and universal life insurance, can accumulate cash value over time, allowing policyholders to borrow or withdraw funds, receive accelerated benefits, or cash out the policy. These policies enable individuals to invest in conservative investments like mutual funds or exchange-traded funds (ETFs) and provide financial benefits during their lifetime, similar to an IRA or mutual fund.

It is important to note that not all insurance policies are created equal. Term life insurance policies, for instance, do not have an accessible cash value during the policyholder's lifetime and are generally less expensive and valid for a set number of years. Therefore, when considering insurance as an asset, individuals should opt for policies that have a cash value, such as permanent life insurance policies.

In summary, insurance becomes an asset when a covered risk is activated, allowing policyholders to receive a payout, or when the plan matures, enabling individuals to access the accumulated cash value. By understanding these aspects, individuals can leverage insurance as a valuable tool for financial protection and wealth management.

Who Gets the Payout? Contesting Life Insurance Beneficiary Designation

You may want to see also

Frequently asked questions

It depends on the type of insurance policy. Term life insurance does not build cash value, whereas permanent life insurance does, which can be considered an asset. Whole life insurance and universal life insurance are two types of permanent life insurance that can be used as assets.

Permanent life insurance policies allow policyholders to accumulate cash value by depositing part of their premiums into a tax-deferred savings account. This money can be withdrawn or used as collateral for a loan. It is important to note that withdrawing money from the policy will reduce the death benefit for beneficiaries.

Permanent life insurance policies often have high fees and poor performance compared to other investment options. Therefore, it may not be a good investment choice for those who are not ultra-wealthy.