Insurance can be perceived as challenging due to its complex terminology, varying policy structures, and the need to understand specific coverage details. For many, navigating the intricacies of premiums, deductibles, and exclusions feels overwhelming, especially when trying to determine the right level of protection for individual needs. Additionally, the process of filing claims and understanding policy limitations often adds to the difficulty. However, with proper research, guidance from professionals, and a clear understanding of personal or business requirements, insurance can become more manageable and less daunting.

| Characteristics | Values |

|---|---|

| Complexity of Concepts | Insurance involves intricate concepts like risk assessment, actuarial science, and policy terms, which can be challenging to grasp. |

| Regulatory Requirements | Strict regulations and compliance standards vary by region, adding complexity to operations and product design. |

| Customer Expectations | High expectations for transparency, fair pricing, and quick claims processing increase pressure on insurers. |

| Technological Advancements | Rapid adoption of AI, data analytics, and digital platforms requires continuous adaptation and investment. |

| Market Competition | Intense competition among insurers drives the need for innovation and cost efficiency. |

| Economic Sensitivity | Insurance is highly sensitive to economic fluctuations, affecting premiums, claims, and investment returns. |

| Claims Management | Handling claims efficiently and fairly is resource-intensive and critical to customer satisfaction. |

| Product Customization | Demand for personalized policies increases complexity in product development and underwriting. |

| Talent Acquisition | Skilled professionals in actuarial science, data analysis, and compliance are in high demand and hard to retain. |

| Customer Education | Educating customers about complex policies and terms remains a significant challenge. |

| Fraud Detection | Increasing instances of insurance fraud require advanced tools and strategies for detection and prevention. |

| Global Trends | Climate change, pandemics, and geopolitical risks introduce new uncertainties and risks. |

Explore related products

What You'll Learn

![]()

Understanding Insurance Basics

Insurance can seem daunting, but breaking it down into its core components simplifies the concept. At its heart, insurance is a contract between you and an insurer, where you pay a premium in exchange for financial protection against specified risks. Think of it as a safety net: you invest a small, manageable amount regularly to avoid a potentially catastrophic financial loss later. For instance, auto insurance doesn’t prevent accidents, but it ensures you’re not left with crippling repair or medical bills if one occurs. Understanding this basic principle—risk pooling and financial protection—is the first step to demystifying insurance.

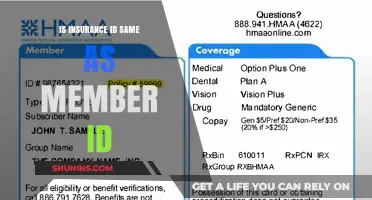

Next, familiarize yourself with key terms like *premium*, *deductible*, and *coverage limits*. The premium is your regular payment to maintain the policy, while the deductible is the amount you pay out-of-pocket before insurance kicks in. Coverage limits cap how much the insurer will pay for a claim. For example, a health insurance policy might have a $1,000 deductible and a $5,000 coverage limit for a specific procedure. If the procedure costs $6,000, you pay $1,000, and the insurer covers $5,000, leaving you responsible for the remaining $1,000. Knowing these terms empowers you to choose policies that align with your financial situation and risk tolerance.

A common misconception is that all insurance policies are one-size-fits-all. In reality, customization is key. Life insurance, for instance, varies widely: term life provides coverage for a set period (e.g., 20 years), while whole life offers lifelong coverage with an investment component. Similarly, homeowners’ insurance can be tailored to include flood or earthquake coverage, depending on your location. Assess your unique needs—age, health, assets, and dependents—to determine the right type and level of coverage. For example, a 30-year-old with a family might prioritize higher life insurance coverage, while a renter may focus on liability protection.

Finally, don’t overlook the importance of reviewing and updating your policies regularly. Life changes—marriage, homeownership, or a new job—can alter your insurance needs. For instance, if you’ve paid off your car loan, you might reduce collision coverage to save on premiums. Similarly, a salary increase could mean you need more disability insurance to protect your higher income. Set a yearly reminder to evaluate your policies, ensuring they still fit your circumstances. This proactive approach prevents gaps in coverage and avoids overpaying for unnecessary protection.

In essence, understanding insurance basics isn’t about mastering complexity but grasping its purpose and mechanics. By focusing on key terms, customizing policies to your needs, and staying proactive, you can navigate insurance with confidence. It’s not about eliminating risk but managing it effectively, ensuring peace of mind without breaking the bank.

Term Life Insurance: Loan Collateral Options Explored

You may want to see also

Explore related products

![Life and Health Insurance Study Cards: Life Health Insurance License Exam Prep with Practice Test Questions [Full Color]](https://m.media-amazon.com/images/I/51Pox87Z5lL._AC_UY218_.jpg)

![Property and Casualty Insurance License Exam Study Guide: Property Casualty Insurance Book and Practice Test Questions [3rd Edition]](https://m.media-amazon.com/images/I/71MhA+5nDML._AC_UY218_.jpg)

![]()

Complexity of Policy Terms

Insurance policies are notorious for their dense, jargon-filled language, leaving many policyholders scratching their heads. The complexity of policy terms is a significant barrier to understanding, often requiring a legal dictionary and a finance degree to decipher. For instance, terms like "indemnity," "subrogation," and "coinsurance" are commonplace but rarely explained in plain English. This opacity can lead to misunderstandings, where customers believe they are covered for certain risks, only to discover loopholes or exclusions when filing a claim. The industry's reliance on such intricate language raises questions about transparency and whether insurers intentionally obscure details to avoid scrutiny.

Consider the process of comparing health insurance plans. A typical policy might outline coverage limits, deductibles, and copayments, but these terms are often embedded in paragraphs of legalese. For example, a policy may state, "Coverage is subject to a $2,000 deductible per policy period, with a 20% coinsurance for out-of-network services." Without a clear explanation, a 40-year-old individual might overlook that "coinsurance" means they pay 20% of the cost after the deductible, potentially leading to unexpected out-of-pocket expenses. Simplifying these terms—such as replacing "coinsurance" with "shared cost"—could empower consumers to make informed decisions.

From a persuasive standpoint, insurers argue that complex terms are necessary to precisely define coverage and protect against fraudulent claims. However, this rationale falls short when weighed against the consumer’s right to clarity. A comparative analysis of European insurance policies reveals that many countries mandate plain-language summaries, ensuring policyholders understand their coverage without needing a law degree. For instance, the UK’s Financial Conduct Authority requires insurers to provide a "key facts document" in straightforward terms. Such regulations demonstrate that complexity is not inevitable but a choice—one that prioritizes legal protection over customer comprehension.

To navigate this complexity, policyholders can take proactive steps. First, request a glossary of terms from the insurer, which many companies provide upon request. Second, use online tools like policy decoders or consult a trusted broker who can translate the fine print. For example, a 55-year-old purchasing life insurance might focus on understanding terms like "contestability period" (typically 2 years, during which the insurer can deny claims for misrepresented information) and "cash value" (the savings component in whole life policies). By breaking down these terms, consumers can avoid pitfalls and ensure their coverage aligns with their needs.

In conclusion, the complexity of policy terms is a solvable problem, not an inherent trait of insurance. While insurers may defend their use of technical language, the onus should be on them to communicate clearly. Until regulatory changes force transparency, consumers must arm themselves with knowledge and tools to decode their policies. After all, insurance is meant to provide peace of mind, not confusion—and understanding the terms is the first step toward achieving that goal.

Mastering the Art of Selling Insurance: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Navigating Claims Process

The claims process is often where policyholders discover whether their insurance investment was worthwhile. It’s a moment of truth, yet many find it labyrinthine and frustrating. From deciphering policy jargon to gathering evidence, each step requires precision and patience. For instance, a homeowner filing a claim after a storm must document damage with photos, obtain repair estimates, and submit these within the insurer’s timeline—often while dealing with the stress of displacement. Missteps here can delay payouts or result in denials, turning a safety net into a source of added anxiety.

Consider the role of adjusters, who assess claims on behalf of insurers. Their evaluations are pivotal, yet their priorities may not align with yours. While they aim to verify legitimacy and minimize payouts, you seek fair compensation. This dynamic underscores the importance of thorough documentation and clear communication. For example, if a medical claim is denied due to a "pre-existing condition," understanding the policy’s exact definition of this term can be the difference between acceptance and rejection. Knowing how to appeal—often a multi-step process involving additional evidence and formal letters—is equally critical.

Navigating claims also involves understanding timelines and thresholds. Auto insurance claims, for instance, often have strict reporting windows; failing to notify your insurer within 24–48 hours of an accident can complicate matters. Similarly, health insurance claims may require pre-authorization for certain procedures, a step overlooked by many. Practical tips include keeping a claims diary, recording all communications, and asking for written confirmations. For complex cases, consulting a public adjuster or attorney can provide expertise, though their fees (typically 5–15% of the settlement) must be weighed against potential benefits.

Comparatively, the claims process varies significantly across insurance types. Life insurance claims, for example, often require a death certificate and policy documents but are generally less contentious. In contrast, property or liability claims involve third-party assessments and negotiations. A business owner filing an interruption claim might need to prove revenue loss through financial statements, a task simplified by maintaining meticulous records. Across all types, the common thread is preparation: knowing your policy inside out, staying organized, and advocating persistently.

Ultimately, the perception that insurance is hard stems partly from the claims process’s complexity. However, with strategic navigation, it becomes manageable. Start by reviewing your policy annually to understand coverage limits and exclusions. During a claim, act promptly but methodically, treating it as a formal process rather than a casual request. Leverage technology—apps that track claims or tools that digitize receipts—to streamline documentation. While insurers have a reputation for red tape, being informed and proactive can transform a daunting task into a structured, even empowering, experience.

Navigating Out-of-Network Transitions: Communicating Insurance Changes to Patients Effectively

You may want to see also

Explore related products

![Texas Property and Casualty Insurance License Exam Prep - Full-Length Practice Tests, Secrets Study Guide and Review: [Detailed Answer Explanations]](https://m.media-amazon.com/images/I/71J3Oq50CJL._AC_UY218_.jpg)

![]()

Comparing Coverage Options

Insurance can feel overwhelming, especially when comparing coverage options. The sheer volume of policies, providers, and jargon can leave you paralyzed by choice. But fear not! Breaking down the comparison process into manageable steps can transform confusion into clarity.

Start by identifying your core needs. Are you seeking health insurance for a young family, auto coverage for a new driver, or life insurance to secure your loved ones' future? Each scenario demands a tailored approach. For instance, a family with young children might prioritize comprehensive health plans with low deductibles and robust pediatric coverage, while a single adult may opt for a high-deductible plan with lower premiums.

Next, scrutinize the fine print. Don't be swayed by catchy slogans or seemingly low rates. Understand what's included and, crucially, what's excluded. A policy with a lower premium might have higher out-of-pocket costs or limited coverage for specific conditions or scenarios. For example, some auto insurance policies exclude coverage for rental cars or ridesharing activities, which could leave you vulnerable in certain situations.

Consider your risk tolerance and financial situation. If you're risk-averse and can afford higher premiums, comprehensive coverage with lower deductibles might be ideal. Conversely, if you're comfortable with higher out-of-pocket costs and have an emergency fund in place, a high-deductible plan could save you money in the long run. For instance, a 25-year-old with no dependents and a stable income might opt for a high-deductible health plan, while a 50-year-old with a family and chronic health conditions would likely benefit from a more comprehensive policy.

Utilize online tools and resources to simplify the comparison process. Many insurance comparison websites allow you to input your specific needs and receive tailored quotes from multiple providers. These platforms often include customer reviews, ratings, and expert analyses, providing valuable insights into each company's reputation, customer service, and claims handling. However, be cautious of biased reviews and always verify information from multiple sources.

Lastly, don't hesitate to seek professional advice. Insurance brokers or financial advisors can offer personalized guidance based on your unique circumstances. They can help you navigate complex policies, identify potential gaps in coverage, and ensure you're getting the best value for your money. While their services may come at a cost, the peace of mind and potential savings can outweigh the expense. By following these steps and adopting a systematic approach, comparing coverage options becomes a manageable task, allowing you to make informed decisions and secure the protection you need.

Whole Life Insurance: Guaranteed Issue, Explained

You may want to see also

Explore related products

![]()

Learning Industry Jargon

Insurance, as a field, is notorious for its dense and often confusing terminology. Learning industry jargon is a critical step in demystifying the complexity of insurance, whether you're a consumer trying to understand a policy or a professional aiming to excel in the field. The first challenge lies in recognizing that insurance jargon isn’t just a barrier—it’s a language designed to convey precise legal and financial concepts. For instance, terms like "deductible," "premium," and "rider" are not interchangeable but carry distinct meanings that impact coverage and cost. Without mastering these terms, even the most well-intentioned decisions can lead to costly misunderstandings.

To tackle this, start by breaking down jargon into manageable chunks. Focus on high-frequency terms first, such as "liability," "underwriting," and "exclusion." Use resources like glossaries provided by insurance companies or regulatory bodies, which often explain terms in plain language. For example, the Insurance Information Institute offers a comprehensive glossary that defines "indemnity" as compensation for a loss, a term often misunderstood by policyholders. Pair this with real-world examples: a deductible is the amount you pay out of pocket before insurance kicks in, much like a copay in health insurance. This contextual learning bridges the gap between abstract definitions and practical application.

However, learning jargon isn’t just about memorization—it’s about understanding the relationships between terms. For instance, "coverage limits" and "policy limits" are related but not identical. The former refers to the maximum amount an insurer will pay for a specific claim, while the latter caps total payouts across all claims. Misinterpreting these can lead to underinsurance or overpaying for unnecessary coverage. A useful strategy is to create visual aids, like flowcharts or tables, to map how terms interact. For example, a table comparing "actual cash value" (ACV) vs. "replacement cost" can clarify how depreciation affects claim payouts, helping you choose the right coverage for your needs.

One common pitfall is assuming that jargon is universally defined. Terms like "flood insurance" can vary significantly between providers and regions. For instance, the National Flood Insurance Program (NFIP) defines flood coverage differently than private insurers, often excluding certain types of water damage. To avoid this trap, cross-reference definitions across multiple sources and consult experts when in doubt. Insurance agents or brokers can provide clarity, but always verify their explanations against written materials to ensure accuracy.

Finally, practice is key. Engage with insurance documents actively rather than skimming them. Highlight unfamiliar terms and research them immediately. Simulate scenarios where understanding jargon matters, such as filing a claim or comparing policies. For example, knowing the difference between "occurrence-based" and "claims-made" policies can determine whether a claim is covered based on when the incident happened or when it was reported. Over time, this hands-on approach transforms jargon from a hurdle into a tool, empowering you to navigate insurance with confidence and precision.

Surrendering Life Insurance: Tax Implications and You

You may want to see also

Frequently asked questions

Insurance can seem complex due to industry jargon and policy details, but with research and guidance from professionals, it becomes easier to grasp.

Selling insurance can be challenging due to competition and the need to build trust, but with persistence, strong communication skills, and product knowledge, it can be a rewarding career.

Approval depends on factors like your health, driving record, or credit score. Some individuals may face challenges, but many policies are accessible with the right preparation.

Managing business insurance can be complex due to varying risks and compliance requirements, but working with a knowledgeable broker or using management tools can simplify the process.