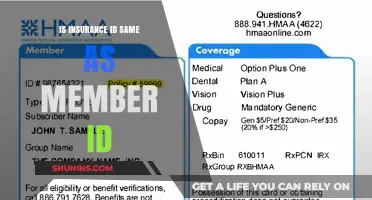

The question of whether an insurance ID serves as a unique key is a critical aspect of data management and identification within the insurance industry. An insurance ID, typically assigned to policyholders or beneficiaries, is designed to uniquely identify individuals or entities within an insurer's system. Its uniqueness ensures accurate record-keeping, prevents duplication, and facilitates efficient processing of claims and policy-related transactions. However, the extent to which an insurance ID functions as a unique key depends on the insurer's database structure, compliance with regulatory standards, and the absence of errors in data entry. Understanding its role as a unique identifier is essential for maintaining data integrity, enhancing operational efficiency, and ensuring seamless interactions between insurers, policyholders, and regulatory bodies.

| Characteristics | Values |

|---|---|

| Uniqueness | Insurance IDs are typically designed to be unique within a specific insurance provider or system. This ensures accurate identification of individual policies and policyholders. |

| Format | The format varies widely depending on the insurance company and type of insurance. It can be alphanumeric, numeric, or a combination, often including letters, numbers, and sometimes special characters. |

| Length | Length varies, typically ranging from 8 to 16 characters, but can be shorter or longer. |

| Purpose | Primarily used for identification and tracking of insurance policies, claims, and policyholder information. |

| Security | Often treated as sensitive information due to its association with personal and financial data. |

| Portability | Generally not portable across different insurance providers. A new ID is usually issued when switching providers. |

| Regulatory Requirements | May be subject to specific formatting or data standards mandated by insurance regulations in different regions. |

| Accessibility | Usually accessible to policyholders through insurance cards, online portals, or policy documents. |

Explore related products

![ESSENTIAL Car Auto Insurance Registration BLACK Document Wallet Holders 2 Pack - [BUNDLE, 2pcs] - Automobile, Motorcycle, Truck, Trailer Vinyl ID Holder & Visor Storage - Strong Closure On Each -](https://m.media-amazon.com/images/I/61px7jy3NmL._AC_UL320_.jpg)

What You'll Learn

- Uniqueness of Insurance ID Numbers: Are insurance IDs universally unique across all providers and policy types

- Purpose of Insurance ID as Key: Why is the insurance ID considered a primary identifier in databases

- Format and Structure: How do insurance IDs vary in length, characters, and encoding standards

- Security and Privacy: What measures ensure insurance IDs protect policyholder data from unauthorized access

- Interoperability Across Systems: Can insurance IDs be seamlessly shared and recognized between different platforms and insurers

![]()

Uniqueness of Insurance ID Numbers: Are insurance IDs universally unique across all providers and policy types?

Insurance ID numbers serve as critical identifiers for policyholders, linking individuals to their specific coverage details. However, the assumption that these IDs are universally unique across all providers and policy types is a misconception. Each insurance company typically generates its own unique ID format, often incorporating alphanumeric characters, hyphens, or other separators. For instance, a health insurance ID from Provider A might look like "HIX-123-4567," while Provider B could use "P789-ABC-23." This variance underscores the lack of a standardized system across the industry.

To understand the implications, consider the process of verifying coverage. When a healthcare provider or claims processor receives an insurance ID, they must first identify the issuer to interpret the number correctly. This step is crucial because an ID from one company might overlap with another’s format, leading to potential confusion. For example, "POL-98765" could belong to both a life insurance policy and an auto insurance policy from different providers. Without a universal key, cross-referencing becomes essential but time-consuming.

From a technical standpoint, the absence of a universally unique insurance ID system poses challenges for data integration and interoperability. In industries like banking, account numbers are often standardized through systems like IBAN (International Bank Account Number), ensuring global uniqueness. Insurance, however, lacks such a framework. Efforts to create a standardized ID system face hurdles, including resistance from providers who have invested in proprietary formats and concerns over data privacy. Until a unified system emerges, policyholders and stakeholders must navigate this fragmented landscape.

Practical tips for individuals include retaining all policy documents and verifying ID accuracy with providers. For businesses, investing in robust ID verification software can streamline processes and reduce errors. While the current system is far from perfect, understanding its limitations empowers users to mitigate risks and ensure accurate policy management. The quest for a universally unique insurance ID remains an ongoing challenge, but awareness and adaptability are key in the interim.

Is Kaiser Insurance Available in Utah? Coverage Options Explained

You may want to see also

Explore related products

![Spigen Car Registration and Insurance Card Holder for All Cars [Tesla Model Y Juniper (2025/26) & 3/Y/S/X/Cybertruck] Store Card Keys, ID License Holder, Essential Documents - Black](https://m.media-amazon.com/images/I/61yTRHM9RZL._AC_UL320_.jpg)

![]()

Purpose of Insurance ID as Key: Why is the insurance ID considered a primary identifier in databases?

Insurance IDs serve as a cornerstone in database management, primarily because they provide a standardized, unique identifier for each policyholder. Unlike names or addresses, which can change or be duplicated, an insurance ID is a static, alphanumeric code assigned to an individual or entity. This uniqueness ensures that each record in a database corresponds to a distinct policyholder, eliminating ambiguity and reducing errors in data retrieval and processing. For instance, in a healthcare database, a patient’s insurance ID links their medical history, claims, and billing information seamlessly, even if their personal details evolve over time.

From a practical standpoint, the insurance ID acts as a relational key, enabling efficient data integration across multiple systems. Insurance companies, healthcare providers, and government agencies often share or cross-reference data. Without a standardized identifier, reconciling records from different sources would be cumbersome and error-prone. For example, when a hospital submits a claim to an insurer, the insurance ID ensures the claim is matched to the correct policyholder’s account, regardless of variations in name spelling or address formatting. This interoperability is critical for streamlining operations and maintaining data accuracy.

The analytical value of insurance IDs extends beyond transactional efficiency. They facilitate data analytics and reporting by providing a consistent basis for aggregating and segmenting information. Insurers can track claims trends, assess risk, and optimize policies by analyzing data tied to unique IDs. For instance, identifying high-frequency claimants or detecting fraudulent activity becomes more straightforward when each policyholder is uniquely tagged. This granularity enhances decision-making and supports compliance with regulatory requirements, such as those related to patient privacy or financial reporting.

However, the effectiveness of insurance IDs as a primary key hinges on their proper implementation. Organizations must ensure that IDs are generated systematically, avoiding duplicates or gaps in the sequence. Additionally, data governance policies should address ID expiration, transferability, and security to prevent misuse. For example, if a policyholder switches insurers, the new provider must either adopt the existing ID or map it to a new one while maintaining historical data integrity. Such precautions safeguard the reliability of the ID as a unique identifier.

In conclusion, the insurance ID’s role as a primary key in databases is rooted in its uniqueness, standardization, and versatility. It simplifies data management, enhances interoperability, and enables advanced analytics, making it indispensable in industries like healthcare and finance. By adhering to best practices in ID generation and governance, organizations can maximize its utility while minimizing risks. As data ecosystems grow more complex, the insurance ID will remain a vital tool for ensuring accuracy, efficiency, and compliance.

Insurance Appraisal Presence: Must You Attend or Can You Skip?

You may want to see also

Explore related products

![Spigen Car Registration and Insurance Card Holder for All Cars [Tesla Model Y Juniper (2025/26) & 3/Y/S/X/Cybertruck] Store Card Keys, ID License Holder, Essential Documents - Dune Beige](https://m.media-amazon.com/images/I/61iYUNw5j2L._AC_UL320_.jpg)

![]()

Format and Structure: How do insurance IDs vary in length, characters, and encoding standards?

Insurance IDs are not one-size-fits-all. Their format and structure vary significantly across providers, regions, and policy types. Length is a primary differentiator, ranging from 8 to 16 characters in most cases, though some IDs can be as short as 6 or as long as 20. For instance, a U.S. health insurance ID might be 10 characters, while a European car insurance ID could be 12. These variations are not arbitrary; they often reflect the complexity of the data encoded and the provider’s internal systems.

Character composition adds another layer of complexity. Insurance IDs typically include alphanumeric characters, but the mix differs. Some IDs use only numbers, while others incorporate letters, hyphens, or special symbols. For example, a life insurance ID might be purely numeric for simplicity, whereas a property insurance ID could include letters to denote policy type or region. Encoding standards further complicate this landscape. While some providers use proprietary formats, others adhere to industry standards like the ANSI X12 EDI for health insurance or the ISO 7812 standard for identifying issuers.

Understanding these variations is crucial for interoperability. Systems that process insurance IDs—whether for claims, verification, or data analysis—must account for these differences to avoid errors. For instance, a system expecting a 10-character numeric ID will fail if it encounters a 12-character alphanumeric one. Developers and analysts should consult provider documentation or industry guidelines to ensure compatibility.

Practical tips for handling insurance IDs include validating their format before processing, using regular expressions to check character types and lengths, and maintaining a lookup table for known encoding standards. For example, a regex pattern like `^[A-Z0-9]{8,16}$` can ensure an ID meets basic alphanumeric and length criteria. Additionally, leveraging APIs provided by insurance companies can streamline validation and reduce manual errors.

In conclusion, the format and structure of insurance IDs are far from standardized, reflecting a patchwork of provider practices and regional norms. By understanding these variations and adopting systematic approaches to handling them, stakeholders can ensure accuracy and efficiency in insurance-related processes.

Life Insurance: Recession-Proof or Risky Move?

You may want to see also

Explore related products

![]()

Security and Privacy: What measures ensure insurance IDs protect policyholder data from unauthorized access?

Insurance IDs serve as a critical link between policyholders and their coverage, but their uniqueness alone doesn’t guarantee security. To protect sensitive policyholder data, insurers employ a layered approach that combines technical, procedural, and legal measures. Encryption, for instance, is a cornerstone of this strategy. Advanced encryption protocols like AES-256 convert policyholder data into unreadable formats during transmission and storage, ensuring that even if unauthorized access occurs, the information remains indecipherable. This measure is particularly vital for digital platforms, where data is more vulnerable to interception.

Beyond encryption, access controls play a pivotal role in safeguarding insurance IDs. Role-based access ensures that only authorized personnel can view or modify policyholder data. For example, a claims adjuster might access claim details but not payment information, while a billing specialist could view payment history but not medical records. Multi-factor authentication (MFA) adds another layer of security by requiring users to provide two or more verification factors—such as a password and a one-time code sent to their phone—before accessing sensitive systems. This significantly reduces the risk of unauthorized access, even if login credentials are compromised.

Regular audits and compliance checks are equally essential to maintaining data security. Insurers must adhere to regulations like GDPR in Europe or HIPAA in the U.S., which mandate strict data protection standards. Audits not only ensure compliance but also identify vulnerabilities in the system. For instance, a routine audit might reveal outdated software or weak password policies, prompting immediate corrective action. Policyholders can enhance their own security by regularly reviewing their insurance accounts for suspicious activity and updating their contact information to ensure they receive timely alerts.

Finally, insurers invest in cybersecurity training for employees to mitigate human error, a leading cause of data breaches. Phishing simulations and workshops educate staff on recognizing and responding to threats. For policyholders, insurers often provide guidelines on protecting their insurance IDs, such as avoiding sharing them over unsecured channels or storing them in easily accessible locations. By combining these measures, insurers create a robust framework that not only protects policyholder data but also fosters trust in their services.

Michigan's No-Fault Insurance: What Changed and Why?

You may want to see also

Explore related products

![]()

Interoperability Across Systems: Can insurance IDs be seamlessly shared and recognized between different platforms and insurers?

Insurance IDs, often serving as unique identifiers for policyholders, are critical for streamlining claims processing, verifying coverage, and preventing fraud. However, their effectiveness hinges on interoperability—the ability to seamlessly share and recognize these IDs across different platforms and insurers. Without standardized formats or universal acceptance, these IDs risk becoming siloed, limiting their utility in a fragmented insurance ecosystem. For instance, a policyholder’s ID from one insurer may not be recognized by another, leading to delays, errors, or redundant data entry. This fragmentation underscores the need for a unified approach to ensure IDs function as true unique keys across systems.

Achieving interoperability requires addressing technical and regulatory challenges. On the technical side, insurers must adopt common data standards, such as HL7 FHIR for health insurance or ACORD standards for property and casualty. These frameworks enable consistent formatting and interpretation of IDs, ensuring they are universally readable. For example, a health insurance ID could include a standardized alphanumeric sequence, with specific segments denoting the insurer, policy type, and policyholder details. Pairing this with APIs (Application Programming Interfaces) allows systems to exchange data in real time, reducing manual intervention and errors.

Regulatory alignment is equally critical. Governments and industry bodies must establish guidelines that mandate the use of standardized IDs and penalize non-compliance. In the European Union, the General Data Protection Regulation (GDPR) already influences how personal data, including insurance IDs, is handled. Extending such regulations to enforce interoperability could create a level playing field. For instance, requiring all insurers to adopt a common ID format by a specific deadline would incentivize collaboration and reduce market friction.

Despite these steps, challenges remain. Legacy systems, often incompatible with modern standards, pose a significant barrier. Insurers must invest in upgrading their infrastructure, which can be costly and time-consuming. Additionally, privacy concerns arise when sharing IDs across platforms. Implementing robust encryption and access controls is essential to protect sensitive information. For example, using tokenization—replacing sensitive ID data with non-sensitive tokens—can minimize exposure while enabling seamless data exchange.

Ultimately, the goal is to transform insurance IDs into universal keys that unlock efficiency and convenience. A policyholder should be able to use their ID across insurers, platforms, and even industries, such as healthcare or automotive, without friction. This vision requires collective effort from insurers, regulators, and technology providers. By prioritizing interoperability, the industry can enhance customer experience, reduce operational costs, and pave the way for innovative services. For instance, a single ID could enable automated claims processing across multiple policies, saving time and reducing administrative burdens. The question is not whether insurance IDs can be seamlessly shared, but how quickly the industry can align to make it a reality.

Uncovering Your Father's Legacy: Life Insurance Discovery

You may want to see also

Frequently asked questions

Yes, an insurance ID is typically a unique identifier assigned to an individual or policyholder to distinguish them from others within an insurance system.

No, insurance IDs are designed to be unique to prevent confusion and ensure accurate identification of policyholders or their coverage details.

Using someone else’s insurance ID is fraudulent and can result in legal consequences, denial of claims, and termination of insurance coverage.