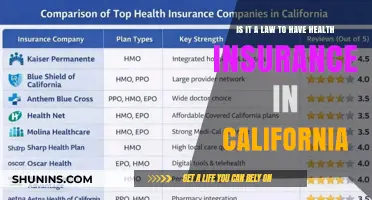

The question of whether it is still the law to have health insurance is a pertinent one, particularly in the context of recent changes to healthcare legislation. Historically, the Affordable Care Act (ACA), also known as Obamacare, mandated that most individuals have health insurance or pay a penalty. However, in 2017, the Tax Cuts and Jobs Act eliminated the individual mandate penalty, effectively repealing this requirement. Despite this change, some states have enacted their own individual mandates to ensure residents maintain health coverage. Additionally, the ACA's other provisions, such as protections for pre-existing conditions and the expansion of Medicaid, remain in place. Therefore, while the federal mandate to have health insurance no longer exists, the legal landscape surrounding health insurance is complex and varies by state.

Explore related products

What You'll Learn

- Legal Requirements: Overview of current laws mandating health insurance coverage

- Penalties for Non-Compliance: Consequences faced by individuals without health insurance

- Types of Acceptable Coverage: Explanation of what constitutes valid health insurance under the law

- Exemptions: Circumstances under which individuals may be exempt from health insurance requirements

- Recent Changes: Updates or amendments to health insurance laws and their implications

![]()

Legal Requirements: Overview of current laws mandating health insurance coverage

The Affordable Care Act (ACA), commonly known as Obamacare, is the primary federal law that mandates health insurance coverage for most U.S. citizens and residents. Enacted in 2010, the ACA requires individuals to maintain minimum essential health insurance coverage or pay a penalty, unless they qualify for an exemption. This mandate aims to ensure that all Americans have access to affordable health care and to reduce the number of uninsured individuals.

Under the ACA, health insurance plans must cover essential health benefits, including preventive care, prescription drugs, and mental health services. Insurers are also prohibited from denying coverage based on pre-existing conditions or charging higher premiums to individuals with health issues. The law provides subsidies to help low-income individuals afford health insurance and expands Medicaid eligibility to cover more people.

While the ACA is the most significant federal law regarding health insurance, some states have enacted their own laws to further regulate health insurance coverage. For example, some states require insurers to cover additional benefits, such as dental care or fertility treatments, or impose stricter regulations on insurance plan design.

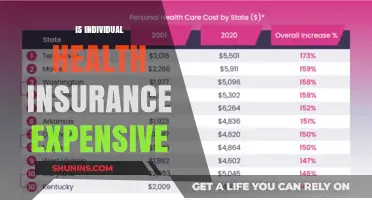

Despite the ACA's mandate, there are still some individuals who do not have health insurance coverage. According to recent data, approximately 28 million Americans are uninsured, representing about 8.5% of the population. The reasons for this vary, but common factors include high premium costs, lack of eligibility for subsidies, and confusion about the enrollment process.

The future of the ACA and health insurance mandates in the United States remains uncertain. The law has faced numerous legal challenges, including a recent Supreme Court case that upheld a key provision of the ACA. However, ongoing political debates and policy proposals suggest that health insurance reform will continue to be a contentious issue in the coming years.

Does Health Insurance Cover Wisdom Teeth Removal? What You Need to Know

You may want to see also

Explore related products

![]()

Penalties for Non-Compliance: Consequences faced by individuals without health insurance

Individuals who fail to maintain health insurance coverage may face a range of penalties, both financial and in terms of access to healthcare services. One of the primary consequences is the imposition of a penalty fee, which can vary depending on the jurisdiction and the duration of non-compliance. For example, in the United States under the Affordable Care Act, the penalty for not having health insurance was calculated as a percentage of one's taxable income or a flat fee, whichever was higher. This financial penalty was designed to encourage individuals to obtain coverage and help offset the costs of uncompensated care.

Beyond financial penalties, individuals without health insurance may also encounter significant barriers to accessing healthcare services. Without insurance, they may be responsible for paying the full cost of medical treatments, which can be prohibitively expensive, leading to delayed or forgone care. This can result in poorer health outcomes, as conditions that could have been managed or treated early on may worsen, requiring more intensive and costly interventions later. Furthermore, uninsured individuals may be less likely to receive preventive care, such as vaccinations and screenings, which are crucial for maintaining overall health and detecting potential issues early.

In some cases, non-compliance with health insurance mandates may also have legal repercussions. For instance, in certain jurisdictions, individuals who fail to obtain health insurance may be subject to fines or even criminal charges. These legal penalties are typically reserved for cases of willful non-compliance or fraud. Additionally, uninsured individuals may face difficulties when seeking employment or applying for certain government benefits, as proof of health insurance coverage may be required as part of the application process.

The penalties for non-compliance with health insurance mandates are designed to promote widespread coverage and ensure that individuals have access to necessary healthcare services. By understanding these consequences, individuals can make informed decisions about their health insurance options and take steps to avoid potential penalties. It is important to note that the specific penalties and requirements can vary significantly depending on the country, state, or region, so it is crucial to be aware of the local laws and regulations regarding health insurance coverage.

Understanding Federal Health Insurance: Coverage, Benefits, and How It Works

You may want to see also

Explore related products

![]()

Types of Acceptable Coverage: Explanation of what constitutes valid health insurance under the law

Under the Affordable Care Act (ACA), also known as Obamacare, health insurance coverage must meet certain standards to be considered acceptable. This means that not all health insurance plans are created equal, and some may not provide the necessary coverage required by law. Acceptable coverage must include essential health benefits, such as preventive care, prescription drugs, and mental health services. It must also cover at least 60% of healthcare costs, leaving no more than 40% to be paid out-of-pocket by the insured individual.

One type of acceptable coverage is a qualified health plan (QHP), which is a plan that meets the ACA's standards and is sold through a health insurance marketplace. QHPs are categorized into four metal levels: bronze, silver, gold, and platinum. Each level represents the cost-sharing ratio between the insured individual and the insurance company. For example, a bronze plan typically covers 60% of healthcare costs, while a platinum plan covers up to 90%.

Another type of acceptable coverage is a grandfathered health plan, which is a plan that was in existence before the ACA was enacted and has not been significantly changed since then. These plans are exempt from some of the ACA's requirements, but they must still provide essential health benefits and meet certain standards.

Employer-sponsored health insurance plans can also be considered acceptable coverage, as long as they meet the ACA's standards. This means that employers who offer health insurance to their employees must ensure that the plans they offer provide essential health benefits and cover at least 60% of healthcare costs.

It's important to note that acceptable coverage does not include short-term health insurance plans, which are designed to provide temporary coverage for a limited period of time. These plans often do not meet the ACA's standards and may not provide the necessary coverage required by law.

In conclusion, acceptable health insurance coverage under the ACA must meet certain standards, including providing essential health benefits and covering at least 60% of healthcare costs. Qualified health plans, grandfathered health plans, and employer-sponsored health insurance plans can all be considered acceptable coverage, as long as they meet these standards.

How to Call and Verify Optum Behavioral Health Insurance Coverage

You may want to see also

Explore related products

![]()

Exemptions: Circumstances under which individuals may be exempt from health insurance requirements

Under the Affordable Care Act (ACA), most U.S. citizens and legal residents are required to have health insurance or pay a penalty. However, there are several exemptions to this mandate. For instance, individuals who are incarcerated are exempt from the requirement to maintain health insurance. This exemption is automatic and does not need to be applied for. Similarly, members of federally recognized tribes are also exempt, as are individuals who are not lawfully present in the United States.

Another exemption applies to individuals who experience a hardship that prevents them from obtaining health insurance. This could include situations such as homelessness, bankruptcy, or domestic violence. To qualify for this exemption, individuals must apply through the health insurance marketplace and provide documentation supporting their hardship claim. If approved, they will be exempt from the penalty for not having health insurance.

Individuals who are part of a health care sharing ministry are also exempt from the ACA's individual mandate. These ministries are religious organizations that provide health care services to their members, often at a lower cost than traditional health insurance. To qualify for this exemption, individuals must be members of a recognized health care sharing ministry and must not have any other health insurance coverage.

Additionally, there is an exemption for individuals who have a short-term gap in health insurance coverage. This exemption applies to those who have lost their health insurance due to job loss or other circumstances and are in the process of obtaining new coverage. The exemption is limited to three months and must be applied for through the health insurance marketplace.

It is important to note that these exemptions are specific and limited. Individuals who do not qualify for an exemption and fail to maintain health insurance coverage may be subject to a penalty. Therefore, it is crucial to understand the exemptions and how they apply in order to avoid potential penalties.

Mastering Health Insurance Payments: A Step-by-Step Spreadsheet Guide

You may want to see also

Explore related products

![]()

Recent Changes: Updates or amendments to health insurance laws and their implications

Recent changes to health insurance laws have introduced new requirements and benefits for policyholders. One significant update is the expansion of coverage for pre-existing conditions, ensuring that individuals with chronic illnesses or previous health issues can access affordable insurance. Additionally, there have been amendments to the age limit for dependents, allowing young adults to remain on their parents' policies until a later age. These changes aim to increase accessibility and affordability of health insurance for a broader range of people.

Another notable change is the introduction of new preventive care benefits, which include free screenings and vaccinations for certain conditions. This update emphasizes the importance of preventive healthcare and aims to reduce long-term healthcare costs by catching and treating conditions early. Furthermore, there have been adjustments to the prescription drug coverage, with some medications now being covered at a lower cost or with reduced copays.

The implications of these changes are far-reaching. For individuals, it means more comprehensive coverage and potentially lower out-of-pocket expenses. For healthcare providers, it may lead to an increase in the number of patients seeking preventive care and early treatment. For insurance companies, these changes could result in a shift in the types of policies offered and the way premiums are calculated.

To navigate these changes effectively, it is essential for policyholders to review their current coverage and understand how the new laws apply to them. This may involve contacting their insurance provider or consulting with a healthcare professional to ensure they are taking advantage of all available benefits. Additionally, staying informed about future changes and updates to health insurance laws can help individuals make informed decisions about their healthcare coverage.

Is Health Insurance Haram? Exploring Islamic Perspectives on Coverage

You may want to see also

Frequently asked questions

As of my last update in June 2024, the requirement to have health insurance, often referred to as the individual mandate, has been repealed in the United States. The Tax Cuts and Jobs Act of 2017 eliminated the federal penalty for not having health insurance, starting in 2019.

Yes, some states have their own individual mandates. For example, Massachusetts and California require residents to have health insurance or face a state-level penalty. It's important to check your state's specific laws regarding health insurance requirements.

While there is no longer a federal penalty for not having health insurance, there are still potential consequences. Without insurance, you may be responsible for paying the full cost of medical services out-of-pocket, which can be very expensive. Additionally, you may not have access to preventive care and screenings that can help detect health issues early.

To find out if you're eligible for health insurance subsidies or Medicaid, you can visit your state's health insurance marketplace website or apply through the federal marketplace at HealthCare.gov. These resources will help you determine your eligibility based on your income and other factors.