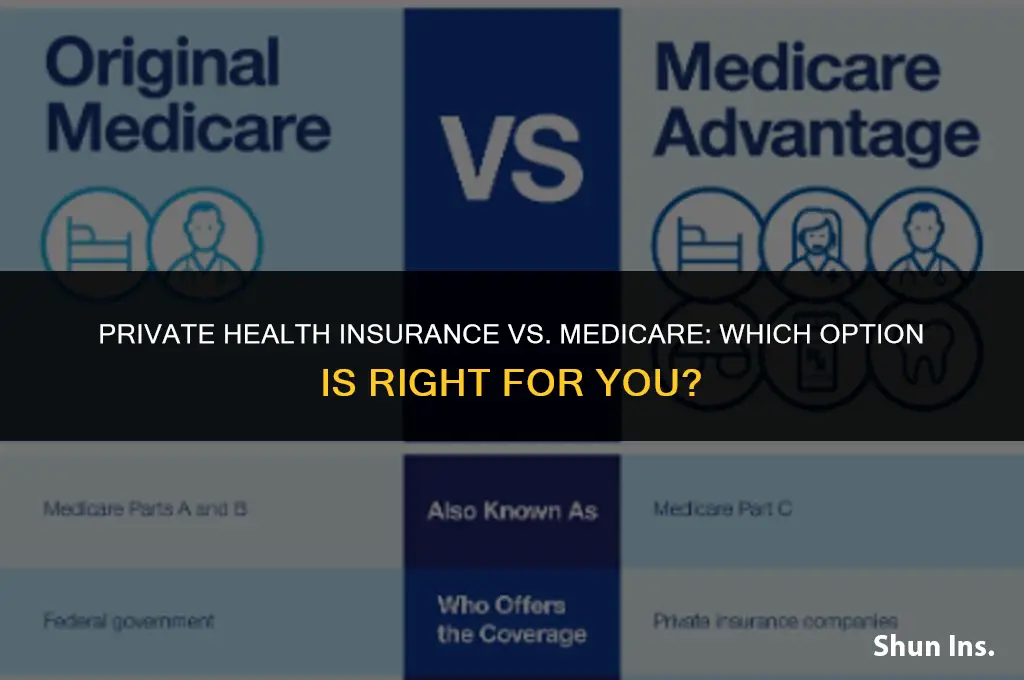

When considering the choice between private health insurance and Medicare, it's essential to weigh the benefits and drawbacks of each option. Private health insurance, often provided through employers or purchased individually, offers a range of plans with varying levels of coverage and costs. These plans may provide more flexibility in choosing healthcare providers and facilities, as well as potentially lower out-of-pocket expenses for certain services. However, private insurance can also come with higher premiums, deductibles, and co-payments, and may not cover all medical services or pre-existing conditions.

On the other hand, Medicare, a government-funded program primarily for individuals aged 65 and older, as well as some younger people with disabilities, offers standardized coverage with lower premiums and out-of-pocket costs compared to private insurance. Medicare provides comprehensive coverage for hospital stays, doctor visits, and prescription medications, and also covers certain preventive services. However, Medicare may have limitations in terms of provider choice and may not cover all medical services or procedures.

Ultimately, the decision between private health insurance and Medicare depends on individual circumstances, including age, health status, income, and personal preferences. It's important to carefully evaluate the options and consider factors such as coverage, cost, provider choice, and overall value when making a decision.

| Characteristics | Values |

|---|---|

| Coverage | Private health insurance: May offer more comprehensive coverage, including dental and vision care. Medicare: Covers essential medical services, but may have gaps in coverage. |

| Cost | Private health insurance: Premiums can be higher, but may offer more predictable costs. Medicare: Generally lower premiums, but may have higher out-of-pocket costs. |

| Flexibility | Private health insurance: Often allows for more choice in providers and plans. Medicare: Limited to approved providers and plans. |

| Enrollment | Private health insurance: Can enroll at any time. Medicare: Enrollment is typically limited to specific periods. |

| Pre-existing conditions | Private health insurance: May exclude or charge more for pre-existing conditions. Medicare: Covers pre-existing conditions without additional charges. |

| Prescription drug coverage | Private health insurance: May offer prescription drug coverage as an add-on. Medicare: Offers prescription drug coverage through Part D plans. |

| Long-term care | Private health insurance: May offer long-term care coverage as an add-on. Medicare: Limited long-term care coverage. |

| Eligibility | Private health insurance: Available to anyone who can afford it. Medicare: Available to those 65 and older, or with certain disabilities. |

Explore related products

What You'll Learn

- Cost Comparison: Evaluate the out-of-pocket expenses, premiums, and deductibles associated with private insurance versus Medicare

- Coverage Differences: Compare the range of services, prescription drug coverage, and specialist access between private plans and Medicare

- Flexibility and Choice: Assess the ability to choose healthcare providers and the flexibility of plans in private insurance compared to Medicare

- Supplemental Insurance Needs: Determine if supplemental insurance is necessary to cover gaps in Medicare or if private insurance provides more comprehensive coverage

- Long-Term Care Options: Examine how private insurance and Medicare handle long-term care, including nursing homes and in-home care services

![]()

Cost Comparison: Evaluate the out-of-pocket expenses, premiums, and deductibles associated with private insurance versus Medicare

Evaluating the cost differences between private health insurance and Medicare involves a detailed comparison of various financial aspects. One key area to examine is out-of-pocket expenses, which can significantly impact an individual's overall healthcare costs. Private insurance often requires higher out-of-pocket payments, including copays and coinsurance, compared to Medicare. However, Medicare beneficiaries may face higher costs for certain services or medications not fully covered by the program.

Another critical factor is premiums. Private health insurance premiums can vary widely based on factors such as age, health status, and coverage level. In contrast, Medicare premiums are generally more standardized, with most beneficiaries paying a fixed monthly amount for Part B coverage. However, those with higher incomes may pay more for Medicare premiums due to income-related adjustments.

Deductibles also play a significant role in the cost comparison. Private insurance plans typically have higher deductibles than Medicare, meaning individuals must pay more out of pocket before their coverage kicks in. Medicare's deductible for Part B is relatively low, but beneficiaries may need to pay a separate deductible for prescription drug coverage under Part D.

When comparing costs, it's essential to consider the overall financial burden on individuals. While private insurance may offer more comprehensive coverage for certain services, the higher premiums and out-of-pocket expenses can make it less affordable for some. Medicare, on the other hand, provides a more predictable cost structure, but may not cover all healthcare needs, potentially leading to additional expenses.

Ultimately, the decision between private health insurance and Medicare depends on individual circumstances, including health status, financial situation, and personal preferences. A thorough cost comparison can help individuals make an informed choice that best meets their healthcare needs and budget.

Non-Emergency Medical Transportation: Who Insures This Service?

You may want to see also

Explore related products

![]()

Coverage Differences: Compare the range of services, prescription drug coverage, and specialist access between private plans and Medicare

Private health insurance plans and Medicare differ significantly in their coverage of services, prescription drugs, and access to specialists. Understanding these differences is crucial for individuals deciding between the two options.

One key difference lies in the range of services covered. Private plans often offer a broader array of services, including dental and vision care, which are not typically covered under Medicare. Additionally, private plans may cover alternative therapies and wellness programs that Medicare does not. However, Medicare generally covers more essential health services, such as hospital stays, doctor visits, and preventive care, with lower out-of-pocket costs.

Prescription drug coverage is another area where private plans and Medicare diverge. Private plans usually have formularies that list the drugs they cover, and these formularies can vary widely between plans. Medicare Part D, which covers prescription drugs, also has formularies, but they tend to be more standardized across different plans. Furthermore, Medicare Part D often has a coverage gap, known as the "donut hole," where beneficiaries pay a higher percentage of their drug costs until they reach a certain spending threshold.

Access to specialists is also a critical factor to consider. Private plans may offer more flexibility in choosing specialists, as they often have larger networks of providers. However, Medicare has its own network of approved providers, and beneficiaries may face limitations in accessing certain specialists, especially in rural areas. Additionally, Medicare requires beneficiaries to use providers who accept Medicare assignment, which can further restrict access to certain specialists.

In conclusion, the choice between private health insurance and Medicare depends on individual needs and preferences. Those who require a broader range of services, including dental and vision care, may find private plans more suitable. However, individuals who prioritize essential health services with lower out-of-pocket costs, standardized prescription drug coverage, and are comfortable with Medicare's network of providers may find Medicare to be the better option.

Medicare and Supplemental Insurance: Understanding Primary Coverage

You may want to see also

Explore related products

![]()

Flexibility and Choice: Assess the ability to choose healthcare providers and the flexibility of plans in private insurance compared to Medicare

Private health insurance often boasts greater flexibility and choice in healthcare providers compared to Medicare. This is because private insurers typically offer a wider range of plans, each with its own network of providers. Policyholders can select a plan that includes their preferred doctors and hospitals, or they may opt for a plan that offers out-of-network coverage if they are willing to pay higher premiums. This level of customization allows individuals to tailor their healthcare coverage to their specific needs and preferences.

In contrast, Medicare is a government-run program that operates on a more standardized model. While Medicare does offer some level of provider choice, it is generally more limited than what is available through private insurance. Medicare Advantage plans, which are offered by private insurers but approved by Medicare, do provide some additional flexibility in terms of provider networks and coverage options. However, these plans are still subject to Medicare's rules and regulations, which can restrict the level of customization available to beneficiaries.

One of the key advantages of private health insurance is the ability to choose from a variety of plan types, each with its own level of coverage and cost-sharing requirements. This allows individuals to select a plan that best fits their healthcare needs and budget. For example, a young, healthy individual may opt for a high-deductible health plan (HDHP) with a lower premium, while an older individual with chronic health conditions may prefer a plan with more comprehensive coverage and lower out-of-pocket costs.

Medicare, on the other hand, offers a more limited selection of plan types. The two main options are Original Medicare, which includes Part A (hospital insurance) and Part B (medical insurance), and Medicare Advantage plans. While Original Medicare provides a basic level of coverage, it does not include prescription drug coverage or dental and vision care. Medicare Advantage plans can offer additional benefits, but they are still subject to Medicare's rules and regulations, which can limit the level of customization available to beneficiaries.

In conclusion, private health insurance generally offers greater flexibility and choice in healthcare providers and plans compared to Medicare. This is because private insurers are not bound by the same rules and regulations as Medicare, allowing them to offer a wider range of options to policyholders. However, it is important to note that private insurance can also be more expensive than Medicare, and individuals should carefully consider their healthcare needs and budget when making a decision about which type of coverage is best for them.

Does Health Insurance Cover Fertility Treatments? What You Need to Know

You may want to see also

Explore related products

![Medicare and Social Security: [5 in 1] Maximize Your Retirement Benefits, Secure Medical Coverage and Quality Healthcare | Proven Strategies to Protect Your Financial Future Avoiding Costly Mistakes](https://m.media-amazon.com/images/I/61ilSrOeMoL._AC_UL320_.jpg)

![]()

Supplemental Insurance Needs: Determine if supplemental insurance is necessary to cover gaps in Medicare or if private insurance provides more comprehensive coverage

Determining the need for supplemental insurance involves a careful assessment of the gaps in Medicare coverage and how they align with your personal health needs and financial situation. Supplemental insurance, such as Medigap policies, is designed to cover costs that Medicare does not, including deductibles, copayments, and coinsurance. These policies can be particularly beneficial for individuals who have high healthcare costs or who travel frequently, as Medicare typically does not cover medical expenses incurred abroad.

To evaluate whether supplemental insurance is necessary, start by reviewing your Medicare coverage and identifying any areas where you may be exposed to significant out-of-pocket expenses. Consider factors such as your age, health status, and the likelihood of needing extended care or prescription drug coverage. If you find that there are substantial gaps in your coverage, supplemental insurance may be a prudent investment to protect your financial well-being.

Private insurance, on the other hand, may offer more comprehensive coverage than Medicare, including vision, dental, and wellness programs. However, private insurance can also be more expensive, and the extent of coverage can vary widely depending on the policy. When comparing private insurance to Medicare, it is essential to consider the total cost of premiums, deductibles, and out-of-pocket expenses, as well as the breadth of coverage provided.

In some cases, individuals may opt for a combination of Medicare and private insurance, using Medicare as the primary payer and private insurance to cover gaps in coverage. This approach can provide a more comprehensive safety net, but it also requires careful coordination to ensure that both plans work together effectively.

Ultimately, the decision to purchase supplemental insurance or private insurance depends on your unique circumstances and priorities. It is advisable to consult with a healthcare professional or insurance advisor to discuss your options and make an informed choice that best meets your needs.

Does Optima Health Bronze Insurance Cover Chantix? A Comprehensive Guide

You may want to see also

Explore related products

![The Medicare Bible for Beginners: [3 in 1] Unlock Medical Benefits and Quality Healthcare | Super Easy Insider Strategies to Navigate Medicare While Avoiding Costly Mistakes](https://m.media-amazon.com/images/I/61wrmwXah3L._AC_UL320_.jpg)

![]()

Long-Term Care Options: Examine how private insurance and Medicare handle long-term care, including nursing homes and in-home care services

Long-term care is a critical aspect of health insurance that often gets overlooked until it's too late. Private insurance and Medicare have distinct approaches to covering long-term care services, which can significantly impact the quality of care and the financial burden on individuals and families.

Private insurance typically offers more comprehensive coverage for long-term care, including nursing homes and in-home care services. Many private insurers provide policies specifically designed for long-term care, which can cover a wide range of services from skilled nursing to personal care and even respite care for caregivers. However, these policies can be expensive, and the cost can vary widely depending on the level of coverage and the individual's health status.

Medicare, on the other hand, has limited coverage for long-term care. While it does cover some short-term rehabilitation services in skilled nursing facilities, it does not provide ongoing coverage for long-term care needs. This can leave individuals and families facing significant out-of-pocket expenses if they require extended care. However, Medicare Advantage plans, which are offered by private insurers, may provide additional coverage for long-term care services.

One of the key differences between private insurance and Medicare is the eligibility requirements for long-term care coverage. Private insurance policies typically require individuals to meet certain health criteria and may have waiting periods before coverage begins. Medicare, on the other hand, does not have these requirements, but it does have strict guidelines for what services are covered and for how long.

When considering long-term care options, it's essential to weigh the costs and benefits of private insurance versus Medicare. Private insurance may provide more comprehensive coverage, but it can also be more expensive. Medicare may be more affordable, but it offers limited coverage for long-term care needs. Ultimately, the best option will depend on an individual's specific needs and financial situation.

Medical Malpractice Insurance Costs in New Jersey: What's the Price?

You may want to see also

Frequently asked questions

The choice between private health insurance and Medicare depends on your individual needs, age, health status, and financial situation. Medicare is a government-funded program primarily for people aged 65 and older, as well as some younger individuals with disabilities. Private health insurance is provided by non-governmental companies and can be tailored to cover specific needs.

Medicare often has lower premiums and out-of-pocket costs compared to private health insurance. It also provides guaranteed coverage for essential health services and prescription drugs, and you can choose from a variety of Medicare plans to suit your needs. Additionally, Medicare is widely accepted by healthcare providers across the United States.

Medicare may have limitations in terms of coverage for certain services, such as dental, vision, and hearing care. It also typically requires you to pay a deductible and coinsurance for covered services. Private health insurance, on the other hand, can offer more comprehensive coverage and may include additional benefits like wellness programs and telemedicine services. However, private insurance can be more expensive and may have higher out-of-pocket costs.