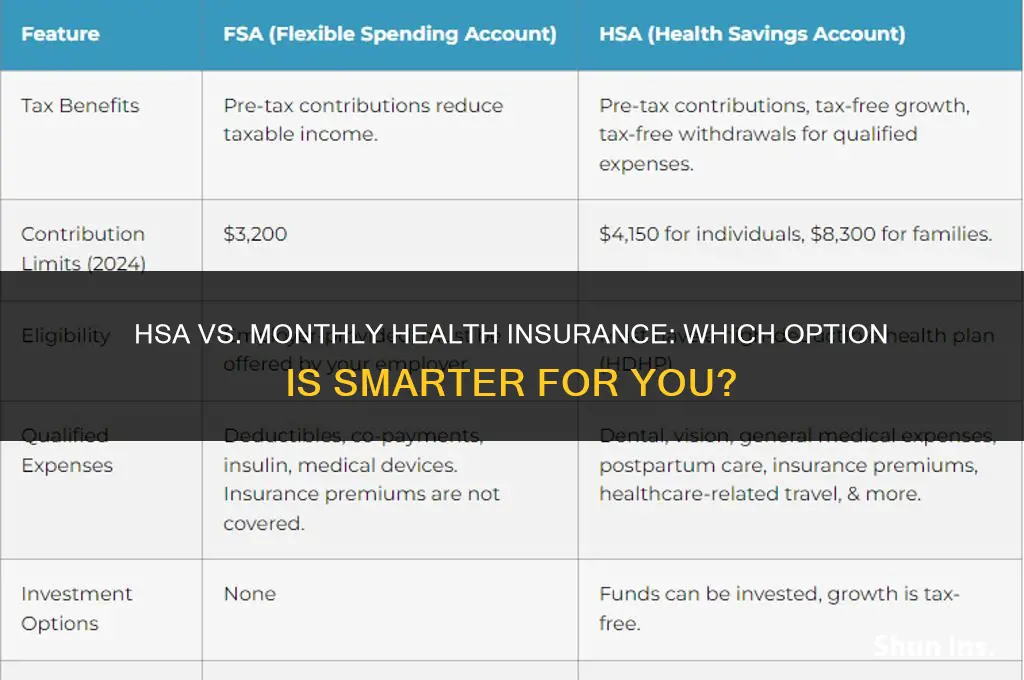

When considering the financial implications of health insurance, many individuals wonder whether opting for a Health Savings Account (HSA) is a smarter choice than traditional monthly health insurance premiums. An HSA allows you to save money on a tax-advantaged basis to cover qualified medical expenses, potentially offering more control over your healthcare spending. However, navigating the complexities of HSAs versus traditional insurance plans requires careful analysis of factors such as contribution limits, withdrawal rules, and the potential long-term benefits of each option.

| Characteristics | Values |

|---|---|

| Cost Comparison | HSA may have lower premiums than traditional monthly health insurance |

| Tax Benefits | HSA contributions are tax-deductible, and withdrawals for qualified medical expenses are tax-free |

| Flexibility | HSA allows for more control over healthcare spending and savings |

| Portability | HSA accounts are portable and can be used with different employers or insurance plans |

| Long-term Savings | HSA can be used as a retirement savings vehicle for healthcare expenses |

| Eligibility | HSA is available to those with a high-deductible health plan (HDHP) and not enrolled in Medicare |

| Administrative Effort | HSA requires more effort to manage and track expenses compared to traditional insurance |

| Risk | HSA carries more financial risk if unexpected medical expenses occur |

Explore related products

What You'll Learn

- Cost Comparison: Evaluate the total annual cost of HSA versus monthly health insurance premiums

- Tax Benefits: Explore the tax advantages of contributing to an HSA compared to paying for health insurance

- Coverage Flexibility: Compare the flexibility in choosing health services and providers between HSA and traditional insurance

- Long-term Savings: Assess the potential for long-term savings with an HSA, considering investment options and growth

- Health Plan Eligibility: Determine eligibility criteria for HSAs and how they differ from those for monthly health insurance plans

![]()

Cost Comparison: Evaluate the total annual cost of HSA versus monthly health insurance premiums

To evaluate the total annual cost of an HSA (Health Savings Account) versus monthly health insurance premiums, it's essential to consider several factors. First, let's break down the components of each option. An HSA is a tax-advantaged account that allows you to save money for qualified medical expenses. It is typically paired with a high-deductible health plan (HDHP), which has lower monthly premiums but higher out-of-pocket costs. On the other hand, traditional health insurance plans with lower deductibles have higher monthly premiums but cover more of your healthcare costs upfront.

When comparing the costs, start by calculating the annual premium for both options. For the HSA-compatible HDHP, multiply the monthly premium by 12. For the traditional health insurance plan, do the same. Next, consider the annual contribution limit to the HSA, which is $3,600 for individuals and $7,200 for families as of 2023. This contribution can be made pre-tax, reducing your taxable income.

Now, let's factor in the out-of-pocket costs. With an HSA, you'll need to cover the deductible and any other qualified medical expenses not covered by the insurance. Traditional health insurance plans may have co-pays and coinsurance, but these are typically lower than the out-of-pocket costs associated with an HSA.

To make a more accurate comparison, create a scenario based on your expected healthcare needs. Estimate the number of doctor visits, prescriptions, and other medical expenses you might incur in a year. Then, calculate the total cost for each option, including premiums, deductibles, and out-of-pocket expenses.

Finally, consider the long-term benefits of an HSA. The funds in your HSA can grow tax-free over time, and you can use them for qualified medical expenses in future years. This can be a significant advantage if you anticipate ongoing healthcare needs or want to save for retirement healthcare costs.

In conclusion, while an HSA can offer tax advantages and potentially lower overall costs for those with high-deductible plans, it requires careful planning and an understanding of your healthcare needs. Traditional health insurance plans with lower deductibles may have higher monthly premiums but can provide more immediate cost savings on healthcare expenses. The smartest choice depends on your individual circumstances, healthcare needs, and financial goals.

Does Menards Offer Health Insurance? Benefits and Coverage Explained

You may want to see also

Explore related products

![]()

Tax Benefits: Explore the tax advantages of contributing to an HSA compared to paying for health insurance

Contributing to a Health Savings Account (HSA) offers several tax benefits that can make it a more attractive option than paying for traditional monthly health insurance. One of the primary advantages is that HSA contributions are tax-deductible, reducing your taxable income for the year. This deduction can be particularly beneficial if you're in a higher tax bracket, as it allows you to save more on taxes. Additionally, the funds in your HSA grow tax-free, meaning you don't pay capital gains taxes on the investment earnings within the account. This tax-free growth can significantly increase the value of your HSA over time, especially if you invest the funds wisely.

Another key tax benefit of HSAs is that withdrawals for qualified medical expenses are tax-free. This means that you can use the funds in your HSA to pay for deductibles, copays, and other out-of-pocket healthcare costs without incurring any additional taxes. In contrast, if you pay for these expenses with after-tax dollars, you're essentially paying more due to the loss of tax efficiency. Furthermore, HSAs offer a unique advantage over other types of health insurance in that they allow you to save for future medical expenses on a tax-advantaged basis. This can be particularly useful if you anticipate having significant healthcare costs in the future, such as during retirement.

When comparing HSAs to traditional health insurance, it's important to consider the overall tax implications. While health insurance premiums may be tax-deductible as well, the deduction is typically limited to the amount of your medical expenses that exceed a certain percentage of your adjusted gross income. In contrast, HSA contributions are fully deductible up to the annual limit, regardless of your medical expenses. This means that HSAs can provide a more consistent and predictable tax benefit over time. Additionally, HSAs offer more flexibility in terms of how you can use the funds, as you can choose to save them for future use or spend them on current medical expenses.

In conclusion, the tax benefits of contributing to an HSA can make it a more financially advantageous option than paying for traditional monthly health insurance. By reducing your taxable income, allowing for tax-free growth and withdrawals, and providing a consistent tax benefit, HSAs can help you save more on healthcare costs over the long term. However, it's important to carefully consider your individual financial situation and healthcare needs when deciding whether an HSA is the right choice for you.

Should You Disclose Existing Health Insurance to WAHealthPlanFinder?

You may want to see also

Explore related products

![]()

Coverage Flexibility: Compare the flexibility in choosing health services and providers between HSA and traditional insurance

Health Savings Accounts (HSAs) offer a unique advantage in terms of coverage flexibility compared to traditional health insurance plans. Unlike traditional insurance, which often comes with a predefined network of providers and a set of covered services, HSAs allow individuals to choose any qualified medical provider or service. This means that HSA holders are not limited to in-network doctors or hospitals and can seek care from any provider that accepts HSA funds.

One of the key benefits of this flexibility is the ability to tailor healthcare choices to individual needs and preferences. For example, an HSA holder may choose to visit a specialist outside of their traditional insurance network or opt for alternative treatments that may not be covered by standard insurance plans. This level of choice can be particularly valuable for individuals with specific health conditions or those who prioritize certain types of care.

Additionally, HSAs can be used to cover a wide range of medical expenses, including deductibles, copays, and even some over-the-counter medications. This broad coverage can help individuals manage their healthcare costs more effectively, as they can use HSA funds to pay for expenses that might otherwise be out-of-pocket under traditional insurance plans.

However, it's important to note that while HSAs offer greater flexibility, they also require more active management from the account holder. Individuals must be diligent in tracking their medical expenses and ensuring that they are using HSA funds appropriately. This can involve more paperwork and administrative tasks compared to traditional insurance, where the insurance company handles much of the claims process.

In conclusion, the flexibility offered by HSAs in choosing health services and providers can be a significant advantage for many individuals. This flexibility allows for more personalized healthcare choices and can help manage costs more effectively. However, it also requires more active management and oversight from the account holder. When considering whether an HSA is the smarter choice compared to traditional monthly health insurance, it's essential to weigh these factors against individual healthcare needs and preferences.

Understanding Medical Insurance Expiry and Validity Periods

You may want to see also

Explore related products

![]()

Long-term Savings: Assess the potential for long-term savings with an HSA, considering investment options and growth

Assessing the potential for long-term savings with a Health Savings Account (HSA) involves understanding the investment options available and projecting the growth of these investments over time. HSAs offer a unique advantage in that they allow for tax-free growth, which can significantly compound savings over the long term.

To maximize long-term savings, it's crucial to consider the investment options offered by the HSA provider. Many HSAs provide a range of investment choices, from conservative options like savings accounts and certificates of deposit (CDs) to more aggressive options like stocks and mutual funds. The choice of investment will depend on the individual's risk tolerance, time horizon, and financial goals.

For those with a longer time horizon, investing in stocks or mutual funds can offer higher potential returns, although they come with greater risk. It's important to diversify investments to minimize risk and maximize returns. Regularly reviewing and rebalancing the investment portfolio can help ensure that it remains aligned with the individual's financial objectives.

Another factor to consider is the fees associated with the HSA. Some accounts may have administrative fees, investment fees, or withdrawal fees, which can eat into the savings over time. It's important to choose an HSA provider with low fees and to be mindful of any potential penalties for early withdrawals.

In addition to investment options and fees, it's also important to consider the contribution limits for HSAs. As of 2023, the annual contribution limit for individuals is $3,600, and for families, it's $7,200. Maximizing contributions within these limits can help accelerate the growth of the HSA balance.

Overall, the potential for long-term savings with an HSA is significant, especially when combined with strategic investment choices and consistent contributions. By carefully considering the investment options, fees, and contribution limits, individuals can make the most of this valuable savings tool.

Your Guide to Enrolling in First Health Insurance Easily

You may want to see also

![]()

Health Plan Eligibility: Determine eligibility criteria for HSAs and how they differ from those for monthly health insurance plans

To determine eligibility for Health Savings Accounts (HSAs), one must first understand the criteria set forth by the Internal Revenue Service (IRS). An individual is eligible to contribute to an HSA if they are covered by a high-deductible health plan (HDHP) and are not enrolled in Medicare. Additionally, they must not be claimed as a dependent on someone else's tax return. The HDHP must meet specific deductible and out-of-pocket maximum limits, which are adjusted annually for inflation. For example, in 2023, the minimum deductible for an individual is $1,400, and the maximum out-of-pocket expense is $7,150.

In contrast, eligibility for monthly health insurance plans, such as those offered through an employer or a health insurance marketplace, typically depends on factors such as employment status, income level, and residency. Employer-sponsored plans often require that an individual be a full-time employee, while marketplace plans may have income limits to qualify for subsidies. Residency requirements vary by state, and some plans may only be available to individuals living in certain areas.

When comparing HSA eligibility to that of monthly health insurance plans, it's important to note that HSAs are designed to be used in conjunction with HDHPs, which may have higher upfront costs but lower premiums. This can make HSAs more attractive to individuals who are generally healthy and do not anticipate frequent medical expenses. On the other hand, monthly health insurance plans may provide more comprehensive coverage and be more suitable for those with higher healthcare needs or who prefer the predictability of fixed monthly premiums.

In summary, while both HSAs and monthly health insurance plans have specific eligibility requirements, HSAs are more closely tied to the structure of an individual's health plan and tax status. Monthly health insurance plans, meanwhile, are influenced by a broader range of factors, including employment and income. Understanding these differences is crucial when deciding which option is more financially advantageous and aligns with an individual's healthcare needs.

Why Insurance Companies Can't Transform Golfers: Unraveling the Limitations

You may want to see also

Frequently asked questions

It depends on your specific financial situation and health needs. An HSA (Health Savings Account) can be a smart choice if you're healthy and don't expect many medical expenses, as it allows you to save money tax-free for future health costs. However, if you have frequent medical needs or high prescription costs, monthly health insurance might provide better coverage and predictability.

An HSA offers several tax advantages. Contributions to an HSA are tax-deductible, reducing your taxable income. The money grows tax-free within the account, and withdrawals for qualified medical expenses are also tax-free. Additionally, if you're 55 or older, you can make catch-up contributions to your HSA, further increasing your tax benefits.

Generally, HSA funds are intended for qualified medical expenses. Using HSA funds for non-medical expenses may result in penalties and taxes. However, some HSA plans allow for limited use of funds for non-medical expenses, such as over-the-counter medications or certain wellness products. It's essential to check your specific HSA plan's guidelines and consult with a tax professional before using HSA funds for non-medical purposes.