The Massachusetts Health Marketplace, also known as MassHealth, is a state-run health insurance exchange that provides coverage options to residents of Massachusetts. Established under the Affordable Care Act, the marketplace offers a range of plans from various insurance providers, catering to different needs and budgets. Individuals and families can explore and enroll in plans that include comprehensive benefits such as medical, dental, and vision care. The marketplace also facilitates access to subsidies and financial assistance for eligible participants, making health insurance more affordable. Navigating the Massachusetts Health Marketplace can be a straightforward process with the right guidance, allowing residents to secure the health coverage they need.

| Characteristics | Values |

|---|---|

| Coverage Area | Massachusetts |

| Plan Types | Individual, Family |

| Insurance Type | Health Insurance Marketplace |

| Subsidy Options | Available based on income |

| Enrollment Period | Open Enrollment, Special Enrollment |

| Provider Network | In-network providers within Massachusetts |

| Premiums | Vary based on plan and coverage |

| Deductibles | Vary based on plan |

| Co-pays | Vary based on plan |

| Out-of-Pocket Costs | Vary based on plan |

| Prescription Drug Coverage | Included in some plans |

| Dental Coverage | Available as an add-on |

| Vision Coverage | Available as an add-on |

| Customer Support | Available through website and phone |

Explore related products

What You'll Learn

- Eligibility Criteria: Understand the requirements to qualify for MA Health Marketplace insurance plans

- Available Plans: Explore the different types of health insurance plans offered through the marketplace

- Enrollment Process: Learn the steps to enroll in a plan, including deadlines and necessary documentation

- Premium Costs: Discover how premiums are calculated and explore potential subsidies or financial assistance

- Coverage Details: Review what services and treatments are covered under MA Health Marketplace insurance plans

![]()

Eligibility Criteria: Understand the requirements to qualify for MA Health Marketplace insurance plans

To qualify for MA Health Marketplace insurance plans, individuals must meet specific eligibility criteria. One of the primary requirements is residency; applicants must be residents of Massachusetts. Additionally, they must be U.S. citizens or lawfully present in the United States. Income also plays a significant role in determining eligibility. Applicants must fall within certain income brackets, which vary depending on the size of their household. For example, a single individual may qualify if their income is below a certain threshold, while a family of four would have a different income limit.

Another crucial factor is the lack of employer-sponsored health insurance. Individuals who have access to employer-provided health coverage are generally not eligible for Marketplace plans, unless their employer's plan does not meet certain standards. Furthermore, applicants must not be enrolled in Medicare or Medicaid. Age is another consideration; applicants must be at least 18 years old, although there are exceptions for younger individuals in certain circumstances.

The application process for MA Health Marketplace insurance involves providing documentation to verify eligibility. This may include proof of residency, citizenship or lawful presence, income, and lack of employer-sponsored insurance. Applicants can submit their applications online, by phone, or in person through a certified application counselor. It's important to note that eligibility criteria may change over time, so it's essential for applicants to stay informed about any updates or changes to the requirements.

Understanding the eligibility criteria for MA Health Marketplace insurance plans is crucial for individuals seeking coverage. By meeting the specific requirements related to residency, citizenship, income, lack of employer-sponsored insurance, and age, applicants can increase their chances of qualifying for a Marketplace plan. Additionally, being aware of the documentation needed and the application process can help ensure a smooth and successful enrollment experience.

Short-Term Medical Insurance: UnitedHealthcare's Temporary Solution

You may want to see also

Explore related products

![]()

Available Plans: Explore the different types of health insurance plans offered through the marketplace

The Massachusetts Health Insurance Marketplace offers a variety of health insurance plans to meet the diverse needs of its residents. These plans are categorized into different metal levels, each representing the cost-sharing ratio between the insured and the insurer. For instance, Bronze plans typically cover about 60% of healthcare costs, leaving the insured to pay the remaining 40%. Silver plans cover around 70%, Gold plans about 80%, and Platinum plans approximately 90%. Understanding these metal levels is crucial for selecting a plan that aligns with one's budget and healthcare needs.

In addition to the metal levels, the marketplace also offers catastrophic plans for individuals under the age of 30 or those who qualify for a hardship exemption. These plans have lower premiums but higher deductibles, making them suitable for those who do not expect to use healthcare services frequently. Furthermore, there are specialized plans for individuals with specific healthcare needs, such as those requiring long-term care or those with chronic conditions.

When exploring the available plans, it's important to consider factors beyond just the premium cost. The out-of-pocket maximum, deductible, copayments, and coinsurance are all critical components that can significantly impact the overall cost of healthcare. Additionally, the network of providers associated with each plan should be carefully reviewed to ensure that preferred doctors and hospitals are included.

To assist in the decision-making process, the Massachusetts Health Insurance Marketplace provides tools and resources on its website. These include a plan comparison tool, which allows users to side-by-side compare different plans based on various criteria, and a subsidy calculator, which helps determine eligibility for financial assistance. By utilizing these resources and carefully evaluating the available plans, individuals can make informed decisions about their healthcare coverage.

Best Medical Insurance Plans for COVID-19 Coverage

You may want to see also

Explore related products

![]()

Enrollment Process: Learn the steps to enroll in a plan, including deadlines and necessary documentation

To enroll in a plan through the Massachusetts Health Marketplace, you must follow a series of steps that include creating an account, filling out an application, and selecting a plan. The enrollment process typically begins in the fall and ends in the winter, with specific deadlines for different types of coverage. For example, if you want your coverage to start on January 1st, you must apply by December 15th. If you miss this deadline, you may still be able to enroll during the open enrollment period, which usually runs until January 31st. However, your coverage may not start until February 1st or later.

The first step in the enrollment process is to create an account on the Massachusetts Health Marketplace website. You will need to provide some basic information, such as your name, email address, and password. Once you have created an account, you can log in and start filling out the application. The application will ask for more detailed information, including your income, household size, and health insurance history. You will also need to provide documentation to verify your identity and income, such as a driver's license, passport, or pay stubs.

After you have submitted your application, you will be able to browse and compare different health plans. You can filter plans based on factors such as cost, coverage, and provider network. Once you have selected a plan, you will need to complete the enrollment process by paying the first month's premium. You can pay online, by mail, or by phone. If you have any questions or need assistance with the enrollment process, you can contact the Massachusetts Health Marketplace customer service center.

It is important to note that the enrollment process can be complex and time-consuming. It is recommended that you start the process early and allow yourself plenty of time to complete each step. If you make a mistake or miss a deadline, you may have to wait until the next open enrollment period to apply again. Therefore, it is crucial to be organized and diligent when enrolling in a plan through the Massachusetts Health Marketplace.

Understanding the Legal Implications of Not Having Health Insurance

You may want to see also

Explore related products

$12.99 $12.99

![]()

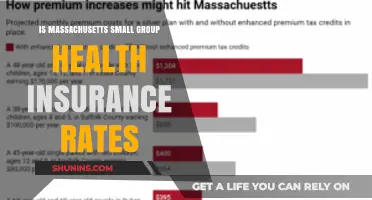

Premium Costs: Discover how premiums are calculated and explore potential subsidies or financial assistance

Understanding premium costs is crucial when navigating the Massachusetts Health Marketplace Insurance. Premiums are the monthly payments you make to maintain your health insurance coverage. They are calculated based on several factors, including your age, income, and the level of coverage you choose. Insurance companies also consider the cost of healthcare services in your area and your health status. To get an accurate estimate of your premium costs, you can use the marketplace's online tool, which allows you to input your specific information and compare plans.

One of the key aspects of the Affordable Care Act (ACA) is the provision of subsidies to help make health insurance more affordable. Depending on your income level, you may be eligible for premium tax credits, which can significantly reduce your monthly payments. These subsidies are designed to ensure that health insurance is accessible to a wide range of individuals, regardless of their financial situation. To determine if you qualify for subsidies, you will need to provide information about your income and household size when applying for coverage.

In addition to premium tax credits, there are other forms of financial assistance available. For example, some plans offer cost-sharing reductions, which can help lower your out-of-pocket expenses for deductibles, copayments, and coinsurance. These reductions are particularly beneficial for individuals who anticipate high healthcare costs. Furthermore, the marketplace may offer additional resources and support to help you understand your options and make informed decisions about your health insurance coverage.

When exploring premium costs and financial assistance, it is important to consider the trade-offs between different plans. While a plan with a lower premium may seem more attractive, it may also have higher out-of-pocket costs or less comprehensive coverage. Conversely, a plan with a higher premium may offer more robust coverage and lower out-of-pocket expenses. To make the best decision, you should carefully evaluate your healthcare needs and budget.

In conclusion, understanding premium costs and exploring potential subsidies or financial assistance are essential steps in selecting the right health insurance plan through the Massachusetts Health Marketplace Insurance. By taking the time to research and compare your options, you can find a plan that provides the coverage you need at a price you can afford.

Maximizing Revenue: Understanding Insurance Collection Rates

You may want to see also

Explore related products

![]()

Coverage Details: Review what services and treatments are covered under MA Health Marketplace insurance plans

Massachusetts Health Marketplace insurance plans offer a comprehensive range of services and treatments to ensure that residents have access to quality healthcare. These plans are designed to cover essential health benefits, which include preventive care, emergency services, prescription drugs, and mental health services. Preventive care services, such as annual check-ups, vaccinations, and screenings, are fully covered to promote early detection and prevention of health issues. Emergency services, including ambulance rides and emergency room visits, are also covered to provide timely and critical care when needed. Prescription drug coverage is another vital component, helping to make medications more affordable for those with chronic conditions or acute illnesses. Mental health services, including counseling and therapy sessions, are covered to support individuals struggling with mental health challenges.

In addition to these essential health benefits, MA Health Marketplace plans may also cover additional services such as dental and vision care, although these may come with separate premiums or copays. It's important for individuals to review the specific coverage details of each plan to understand what services are included and any associated costs. This can help them choose a plan that best meets their healthcare needs and budget.

When selecting a plan, it's also crucial to consider the network of providers. MA Health Marketplace plans typically have a network of healthcare providers, including doctors, hospitals, and specialists, that have agreed to provide services at a negotiated rate. Staying within this network can help individuals save money on healthcare costs. However, some plans may offer out-of-network coverage, albeit at a higher cost, for those who prefer to see providers outside of the network.

Understanding the coverage details of MA Health Marketplace insurance plans can help individuals make informed decisions about their healthcare. By reviewing the services and treatments covered, as well as any associated costs and provider networks, residents can choose a plan that provides the best possible coverage for their unique needs. This can lead to better health outcomes and greater peace of mind, knowing that they have access to quality healthcare when they need it.

Exploring Health Insurance Choices in Tennessee: A Comprehensive Guide

You may want to see also

Frequently asked questions

MA Health Marketplace Insurance refers to health insurance plans that are available through the Massachusetts Health Connector, which is the state's official health insurance marketplace. It offers a variety of plans from different insurance providers, allowing residents to compare and choose the best option for their needs.

Eligibility for MA Health Marketplace Insurance depends on several factors, including income, age, and residency status. Generally, individuals and families with incomes up to 400% of the Federal Poverty Level (FPL) may qualify for subsidized plans. Additionally, individuals who are not eligible for employer-sponsored insurance or other government programs like Medicaid or Medicare may also be eligible.

Enrollment in MA Health Marketplace Insurance can be done through the Massachusetts Health Connector website or by contacting their customer service. The enrollment process typically involves creating an account, filling out an application, and selecting a plan. It's important to note that there are specific enrollment periods, and individuals may need to provide documentation to verify their eligibility.