Mandatory health insurance, also known as compulsory health insurance, is a system where individuals are required by law to have health insurance coverage. This system aims to ensure that everyone has access to healthcare services and to distribute the cost of healthcare across the population. As of my last update in June 2024, many countries around the world have some form of mandatory health insurance in place. However, the specifics of these systems, including the extent of coverage, the cost to individuals, and the penalties for non-compliance, vary significantly from one country to another. In some countries, mandatory health insurance is provided by the government, while in others, it is offered by private insurance companies. The effectiveness and impact of mandatory health insurance systems are subjects of ongoing debate, with proponents arguing that they improve access to healthcare and reduce financial burdens on individuals, and critics contending that they can be costly and limit individual choice.

| Characteristics | Values |

|---|---|

| Topic | Health Insurance |

| Type | Mandatory |

| Status | In Effect |

| Language | English |

| Format | Table |

| Date | June 2024 |

Explore related products

What You'll Learn

- Current status of the Affordable Care Act (ACA) and its impact on health insurance mandates

- Recent changes in federal and state health insurance laws affecting mandatory coverage

- Enforcement of individual mandate penalties and their implications for uninsured individuals

- Employer-sponsored health insurance requirements under the ACA and related compliance issues

- Medicaid expansion and its influence on mandatory health insurance coverage across states

![]()

Current status of the Affordable Care Act (ACA) and its impact on health insurance mandates

The Affordable Care Act (ACA), commonly known as Obamacare, has undergone significant changes since its inception in 2010. One of the most notable aspects of the ACA was the individual mandate, which required most Americans to have health insurance or pay a penalty. However, in 2017, the Tax Cuts and Jobs Act (TCJA) repealed the individual mandate, effectively eliminating the penalty for not having health insurance. Despite this change, the ACA remains in effect, and many of its provisions continue to shape the healthcare landscape in the United States.

The repeal of the individual mandate has had a mixed impact on health insurance coverage. On one hand, it has led to a slight decrease in the number of insured individuals, as some people have chosen to forgo coverage without the threat of a penalty. On the other hand, the ACA's other provisions, such as the expansion of Medicaid and the establishment of health insurance exchanges, have helped to maintain and even increase coverage for many Americans. Additionally, the ACA's protections for people with pre-existing conditions and its requirement that insurers cover essential health benefits remain in place, ensuring that those who do have insurance have access to comprehensive care.

The current status of the ACA is the subject of ongoing debate and litigation. In 2020, the Supreme Court heard a case challenging the constitutionality of the ACA, but ultimately upheld the law. However, the legal challenges to the ACA are not over, and the law's future remains uncertain. In the meantime, states have taken different approaches to implementing the ACA, with some expanding Medicaid and others opting not to. This has created a patchwork of coverage across the country, with some states experiencing higher rates of uninsured individuals than others.

The impact of the ACA on health insurance mandates has been significant, but it is important to note that the law has also had a broader impact on the healthcare system as a whole. The ACA has helped to slow the growth of healthcare costs, improve the quality of care, and increase access to preventive services. While the individual mandate may no longer be in effect, the ACA's other provisions continue to play a crucial role in shaping the healthcare landscape in the United States.

In conclusion, the current status of the Affordable Care Act and its impact on health insurance mandates is complex and multifaceted. While the individual mandate has been repealed, the ACA remains in effect, and its other provisions continue to influence the healthcare system. The law's future is uncertain, but its impact on healthcare coverage and costs is undeniable. As the debate over the ACA continues, it is important to consider the full range of its effects and the potential consequences of further changes to the law.

Understanding Copayments: A Key Component of Health Insurance Explained

You may want to see also

Explore related products

$31.08 $54.99

$14.99 $14.99

$61.7 $64.95

![]()

Recent changes in federal and state health insurance laws affecting mandatory coverage

Recent changes in federal and state health insurance laws have significantly impacted mandatory coverage requirements. One of the most notable changes is the repeal of the federal individual mandate penalty under the Affordable Care Act (ACA). This penalty, which was designed to encourage individuals to maintain health insurance coverage, was eliminated as part of the Tax Cuts and Jobs Act of 2017. As a result, individuals are no longer subject to a federal penalty for failing to have health insurance, although some states have implemented their own individual mandates to fill this gap.

At the state level, there has been a flurry of activity regarding mandatory health insurance coverage. Some states, such as California and New Jersey, have enacted their own individual mandates, requiring residents to maintain health insurance coverage or face a state penalty. Other states have taken a different approach, opting to expand Medicaid under the ACA to provide more comprehensive coverage to low-income individuals. This expansion has been particularly significant in states with high uninsured rates, as it has helped to reduce the number of individuals without health insurance.

In addition to changes in individual mandate laws, there have also been recent developments in employer-sponsored health insurance. The ACA originally required employers with 50 or more full-time employees to offer health insurance coverage to their workers or face penalties. However, this requirement has been subject to numerous legal challenges and regulatory changes. Most recently, the Trump administration issued a final rule allowing employers to offer health reimbursement arrangements (HRAs) as an alternative to traditional health insurance coverage. This change could potentially impact the number of individuals with employer-sponsored health insurance, as HRAs may not provide the same level of coverage as traditional health plans.

Another area of change in health insurance laws is the increasing focus on transparency and cost containment. Many states have implemented laws requiring health insurers to disclose their pricing information and justify rate increases. This increased transparency is intended to help consumers make more informed decisions about their health insurance coverage and to put pressure on insurers to keep costs down. Additionally, some states have implemented laws aimed at reducing prescription drug costs, such as price caps and importation programs. These measures could potentially impact the overall cost of health insurance coverage and make it more affordable for consumers.

Overall, the recent changes in federal and state health insurance laws have created a complex and evolving landscape for mandatory coverage requirements. While the federal individual mandate penalty has been repealed, many states have implemented their own mandates or expanded Medicaid to ensure that residents have access to health insurance coverage. Employers are also facing changes in their obligations to provide health insurance coverage, with the rise of HRAs as an alternative to traditional health plans. Finally, there is an increasing focus on transparency and cost containment in health insurance markets, with states implementing laws aimed at reducing costs and increasing consumer choice.

Art Medication Costs: Out-of-Pocket Expenses and Affordability

You may want to see also

Explore related products

![]()

Enforcement of individual mandate penalties and their implications for uninsured individuals

The enforcement of individual mandate penalties has been a critical aspect of the Affordable Care Act (ACA), aiming to encourage uninsured individuals to obtain health coverage. Despite the ACA's implementation, the individual mandate penalty has faced numerous challenges and changes over the years. As of now, the penalty for not having health insurance is no longer in effect at the federal level, thanks to the Tax Cuts and Jobs Act of 2017, which reduced the penalty to $0 starting in 2019. However, some states have chosen to implement their own individual mandates and penalties to promote health coverage among their residents.

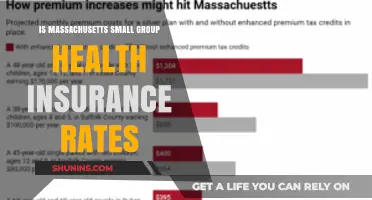

For uninsured individuals, the implications of these penalties can be significant. In states with active individual mandates, failing to obtain health insurance can result in fines or other penalties. For example, in Massachusetts, residents who do not have health insurance may face a penalty of up to $2,000 per year. In addition to financial penalties, uninsured individuals may also face challenges accessing healthcare services, as they may be responsible for paying full price for medical treatments and procedures.

The enforcement of individual mandate penalties has also had broader implications for the healthcare system as a whole. By encouraging more people to obtain health insurance, these penalties have helped to reduce the number of uninsured individuals and improve overall health outcomes. However, the penalties have also been controversial, with some arguing that they are an overreach of government authority and an undue burden on individuals.

In conclusion, while the federal individual mandate penalty is no longer in effect, some states have chosen to implement their own penalties to promote health coverage. For uninsured individuals, these penalties can have significant financial and healthcare implications. The enforcement of individual mandate penalties has been a complex and contentious issue, with both supporters and opponents weighing in on its effectiveness and fairness.

Understanding Medical Expenses: Navigating Insurance Claims and Paperwork

You may want to see also

Explore related products

![]()

Employer-sponsored health insurance requirements under the ACA and related compliance issues

Under the Affordable Care Act (ACA), employer-sponsored health insurance requirements mandate that large employers—those with 50 or more full-time employees—must offer health insurance to their full-time workers or face penalties. This provision aims to increase health coverage among Americans and reduce the number of uninsured individuals. Employers must provide plans that meet certain standards, including covering essential health benefits and adhering to cost-sharing limits.

Compliance with these requirements involves several key aspects. Employers must accurately determine their employee count, distinguishing between full-time and part-time workers. They must also ensure that their health plans meet the ACA's standards for essential health benefits, which include coverage for preventive care, prescription drugs, and mental health services, among others. Additionally, employers need to be aware of the cost-sharing provisions, which limit the amount employees can be required to pay out-of-pocket for covered services.

One significant compliance issue employers face is the potential for penalties if they fail to offer adequate coverage. The ACA imposes two types of penalties: one for not offering coverage to a sufficient percentage of employees and another for offering plans that do not meet the essential health benefits or cost-sharing requirements. Employers must carefully monitor their compliance to avoid these penalties, which can be substantial.

Another challenge is the need to communicate effectively with employees about their health insurance options. Employers are required to provide clear and accurate information about the available plans, including details on coverage, costs, and enrollment procedures. This can be a complex task, especially for employers with diverse workforces or those who offer multiple plan options.

To navigate these requirements and compliance issues, many employers turn to professional advisors or consultants who specialize in health insurance and ACA regulations. These experts can help employers understand their obligations, develop strategies for compliance, and manage the complexities of offering health insurance in a way that meets the ACA's standards.

In summary, employer-sponsored health insurance requirements under the ACA are a critical aspect of the law's efforts to expand health coverage. Compliance involves accurately determining employee eligibility, ensuring plans meet essential health benefits and cost-sharing standards, avoiding penalties, and effectively communicating with employees. Employers must stay vigilant and informed to meet these requirements and provide adequate health insurance to their workers.

Is Acupuncture Covered by Specialist Health Insurance Plans?

You may want to see also

Explore related products

![]()

Medicaid expansion and its influence on mandatory health insurance coverage across states

Medicaid expansion has significantly influenced mandatory health insurance coverage across states. Under the Affordable Care Act (ACA), states were given the option to expand Medicaid to cover more low-income individuals. This expansion has had a profound impact on the number of people with health insurance, particularly in states that chose to participate. For instance, states like California and New York saw substantial increases in Medicaid enrollment, leading to higher overall insurance coverage rates.

One of the key aspects of Medicaid expansion is its role in filling the coverage gap for individuals who earn too much to qualify for traditional Medicaid but still cannot afford private insurance. By expanding Medicaid, these states have been able to provide a safety net for a larger portion of their population, reducing the number of uninsured individuals. This, in turn, has contributed to the overall effectiveness of mandatory health insurance laws.

However, not all states opted for Medicaid expansion. States like Texas and Florida chose not to participate, citing concerns about cost and the desire to maintain more control over their healthcare programs. As a result, these states have seen smaller improvements in insurance coverage rates compared to their counterparts that expanded Medicaid. This disparity highlights the significant role that state policies play in determining the reach and impact of mandatory health insurance laws.

Furthermore, Medicaid expansion has also had economic benefits for states. By increasing access to healthcare, states have seen reductions in uncompensated care costs, which occur when hospitals and other healthcare providers treat uninsured patients without receiving payment. Additionally, Medicaid expansion has created jobs in the healthcare sector and stimulated local economies.

In conclusion, Medicaid expansion has been a critical factor in shaping the landscape of mandatory health insurance coverage across states. While the ACA set the framework for expanding Medicaid, the decision to participate has been left to individual states, leading to varying degrees of success in improving insurance coverage rates. The experiences of states that have expanded Medicaid serve as valuable lessons for policymakers considering similar initiatives in the future.

Key Stakeholders in Insurance Companies: Roles and Impact Explained

You may want to see also

Frequently asked questions

Yes, as of my last update in June 2024, the Affordable Care Act (ACA), which includes the individual mandate for health insurance, is still in effect. However, the penalty for not having health insurance was reduced to $0 starting in 2019.

Yes, some states have implemented their own individual mandates. For example, Massachusetts has a state-level individual mandate that requires residents to maintain health insurance coverage. Other states, like California, have also considered or implemented similar measures.

While the federal penalty for not having health insurance is currently $0, there can still be significant financial risks associated with being uninsured. These include being responsible for the full cost of medical services, which can be very high in the event of an illness or injury. Additionally, uninsured individuals may face difficulties accessing certain healthcare services or providers.

The debate around mandatory health insurance has been ongoing for many years. The ACA, passed in 2010, was a significant step towards universal coverage, but it has faced numerous challenges and attempts at repeal. The individual mandate, in particular, has been a contentious issue, with some arguing it is necessary to ensure the stability of the health insurance market, while others view it as an infringement on personal freedom. The reduction of the penalty to $0 in 2019 was part of the Tax Cuts and Jobs Act of 2017, reflecting a shift in the political landscape and priorities.

![Tax Compliance Q&A 2017 [FA2016]](https://m.media-amazon.com/images/I/41EN-H9KmPL._AC_UY218_.jpg)

![Tax Compliance Q&A 2015 [FA2014]](https://m.media-amazon.com/images/I/41kpkTXqUuL._AC_UY218_.jpg)

![Tax Compliance Q&A 2014 [FA2013]](https://m.media-amazon.com/images/I/41aRIaaGKzL._AC_UY218_.jpg)