When comparing marketplace insurance to insurance exchange options, it’s essential to understand their distinctions and benefits. Marketplace insurance, often facilitated through platforms like Healthcare.gov, offers standardized plans with subsidies for eligible individuals, ensuring affordability and compliance with the Affordable Care Act (ACA). On the other hand, insurance exchanges, which can be private or state-run, provide a broader range of plans, including those that may not meet ACA requirements, offering more flexibility but potentially fewer protections. The choice between the two depends on factors like income, subsidy eligibility, and specific healthcare needs, making it crucial to evaluate which option aligns best with your financial and medical circumstances.

| Characteristics | Values |

|---|---|

| Definition | Marketplace Insurance: Plans offered through HealthCare.gov or state-based marketplaces. Insurance Exchange: Another term for the same marketplace, often used interchangeably. |

| Plan Options | Both offer standardized plans (Bronze, Silver, Gold, Platinum) with similar coverage levels. |

| Subsidy Eligibility | Both provide access to premium tax credits and cost-sharing reductions based on income. |

| Network Coverage | Plans may have varying provider networks; depends on the specific insurer, not the platform. |

| Cost Comparison | Costs are comparable since plans are regulated under the ACA; differences arise from insurer rates, not the platform. |

| Enrollment Periods | Both follow the same open enrollment and special enrollment periods. |

| Regulation | Both are regulated under the Affordable Care Act (ACA), ensuring essential health benefits. |

| User Experience | HealthCare.gov and state marketplaces may differ in interface, but functionality is similar. |

| Availability | Both are available in all states, though some states operate their own marketplaces. |

| Conclusion | There is no inherent difference; "marketplace" and "exchange" refer to the same platform. |

Explore related products

What You'll Learn

- Cost comparison: premiums, deductibles, and out-of-pocket expenses between marketplace and exchange plans

- Plan flexibility: differences in coverage options, provider networks, and policy customization

- Subsidy eligibility: availability of financial assistance on marketplace versus exchange platforms

- Enrollment process: ease of application, documentation, and approval timelines for both options

- Customer support: quality of assistance, resources, and guidance offered by each platform

![]()

Cost comparison: premiums, deductibles, and out-of-pocket expenses between marketplace and exchange plans

Navigating the cost landscape of health insurance requires a keen eye for detail, especially when comparing marketplace and exchange plans. Premiums, deductibles, and out-of-pocket expenses are the trifecta of financial considerations, each playing a distinct role in your overall healthcare expenditure. Let’s dissect these components to uncover where marketplace and exchange plans diverge and converge.

Premiums are the monthly payments you make to maintain coverage, and they often serve as the initial point of comparison. Marketplace plans, offered through the Health Insurance Marketplace (Healthcare.gov), tend to provide a wider range of premium options, catering to diverse income levels. For instance, a 30-year-old in Texas might find marketplace premiums ranging from $200 to $500 monthly, depending on the metal tier (Bronze, Silver, Gold, Platinum). Exchange plans, often provided by state-based exchanges or private brokers, may offer competitive premiums but with less variability. A Silver plan on a state exchange could cost $350 monthly, comparable to a similar marketplace plan but with fewer subsidy options for lower-income individuals.

Deductibles introduce a layer of complexity, representing the amount you pay out-of-pocket before insurance kicks in. Marketplace plans frequently feature lower deductibles for higher-tier plans (e.g., a Gold plan with a $1,000 deductible), making them appealing for those anticipating frequent medical needs. Exchange plans, however, might offer lower-premium options with higher deductibles (e.g., a Bronze plan with a $6,000 deductible), suitable for healthier individuals willing to gamble on fewer medical expenses. For a family of four, this difference could mean paying $2,000 versus $24,000 out-of-pocket before coverage begins.

Out-of-pocket expenses, including copays and coinsurance, further differentiate the two. Marketplace plans often cap these expenses at federally mandated limits (e.g., $9,450 for an individual in 2023), providing predictability. Exchange plans may adhere to similar caps but could vary based on the insurer’s policies. A Silver marketplace plan might cover 70% of costs after the deductible, leaving you with $3,000 in out-of-pocket expenses for a $10,000 procedure, while an exchange plan might cover only 60%, increasing your share to $4,000.

To maximize cost-effectiveness, consider these practical tips: assess your annual healthcare usage, factor in potential subsidies (available only on the marketplace), and compare metal tiers across both platforms. For example, a 45-year-old with chronic conditions might save $1,500 annually by choosing a marketplace Gold plan over an exchange Silver plan, despite higher premiums, due to lower deductibles and out-of-pocket costs. Conversely, a healthy 25-year-old could save $200 monthly with an exchange Bronze plan, accepting higher financial risk for lower premiums.

In conclusion, the cost comparison between marketplace and exchange plans hinges on individual needs and financial flexibility. While marketplace plans offer broader subsidy access and predictable out-of-pocket limits, exchange plans may provide tailored premium options for specific demographics. By scrutinizing premiums, deductibles, and out-of-pocket expenses, you can align your insurance choice with your healthcare and budgetary priorities.

Life Insurance and Probate: What's the Connection?

You may want to see also

Explore related products

![]()

Plan flexibility: differences in coverage options, provider networks, and policy customization

One of the most significant distinctions between marketplace insurance and insurance exchanges lies in the flexibility they offer consumers in tailoring their health plans. Coverage options vary widely, with marketplace insurance often providing a broader range of choices, from high-deductible plans suited for healthy individuals to comprehensive policies for those with chronic conditions. Insurance exchanges, while offering standardized plans, may limit options to a few tiers (bronze, silver, gold, platinum), which can restrict customization based on specific health needs. For instance, a 35-year-old freelancer might find a marketplace plan with telehealth services included, whereas an exchange plan might exclude such benefits unless purchased as an add-on.

Provider networks are another critical factor in plan flexibility. Marketplace insurance plans often feature larger, more diverse networks, allowing policyholders to access a wider array of specialists and hospitals. In contrast, insurance exchange plans may have narrower networks to keep premiums low, which can be problematic for individuals requiring specialized care. For example, a patient with a rare autoimmune disorder might struggle to find an in-network rheumatologist under an exchange plan, whereas a marketplace plan could offer access to multiple specialists within a reasonable distance.

Policy customization is where marketplace insurance truly shines. Many marketplace plans allow consumers to add optional riders, such as dental, vision, or maternity coverage, depending on their life stage and health priorities. Insurance exchanges, however, typically bundle these benefits into standardized tiers, leaving less room for personalization. A young couple planning to start a family, for instance, might opt for a marketplace plan with enhanced prenatal care coverage, which could be absent or inadequate in an exchange plan.

To maximize plan flexibility, consumers should assess their current and anticipated health needs before choosing between marketplace insurance and an exchange. For those with stable health and a preference for lower premiums, an exchange plan might suffice. However, individuals with complex medical histories or a desire for tailored coverage should lean toward marketplace options. Practical tips include reviewing the provider directory for in-network specialists, comparing prescription drug formularies, and calculating out-of-pocket costs for anticipated medical services. Ultimately, the choice hinges on balancing cost with the need for personalized care and access to a robust provider network.

Life Insurance: When Payments Outweigh Benefits

You may want to see also

Explore related products

![]()

Subsidy eligibility: availability of financial assistance on marketplace versus exchange platforms

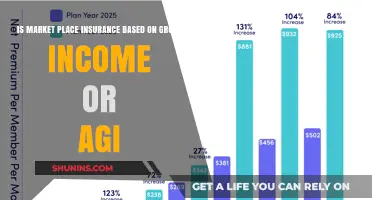

Subsidies can significantly reduce health insurance costs, but their availability differs between marketplace and exchange platforms. Marketplaces, often referred to as Health Insurance Marketplaces or state-based exchanges, are primarily established under the Affordable Care Act (ACA). These platforms offer a unique advantage: access to Advanced Premium Tax Credits (APTC) and Cost-Sharing Reductions (CSRs). APTCs lower monthly premiums, while CSRs reduce out-of-pocket costs like deductibles and copayments. Eligibility for these subsidies is based on income, typically for individuals and families earning between 100% and 400% of the Federal Poverty Level (FPL). For example, in 2023, a family of four earning between $28,000 and $112,000 annually could qualify.

In contrast, insurance exchanges not tied to the ACA may not offer these federal subsidies. Private exchanges, often operated by brokers or employers, typically provide plans without APTCs or CSRs. While these platforms might offer competitive rates or group discounts, they lack the financial assistance available on ACA-compliant marketplaces. This makes marketplace plans more affordable for individuals and families with moderate incomes. For instance, a 35-year-old earning $35,000 annually might pay $150/month for a marketplace plan with subsidies, compared to $300/month on a private exchange.

However, recent policy changes have expanded subsidy eligibility on marketplaces. The American Rescue Plan Act (ARPA) of 2021 removed the 400% FPL cap for APTCs, allowing higher-income individuals to qualify for assistance. Additionally, it increased subsidy amounts, reducing premiums for many enrollees. For example, a 40-year-old earning $58,000 annually, previously ineligible for subsidies, might now pay $200/month instead of $450. These changes make marketplace plans even more attractive compared to exchange options.

To maximize subsidy eligibility, applicants should accurately report their income and compare plans during open enrollment. Tools like the Healthcare.gov subsidy calculator can estimate potential savings. For those near the FPL threshold, small income adjustments—such as contributing to a retirement account—could increase subsidy amounts. Conversely, private exchange users should explore group discounts or employer-sponsored plans to offset the lack of federal assistance.

In conclusion, while both marketplace and exchange platforms offer health insurance options, marketplaces provide unparalleled financial assistance through subsidies. Eligibility criteria, expanded by recent legislation, make marketplace plans more affordable for a broader population. For those seeking cost-effective coverage, understanding and leveraging these subsidies is crucial.

Annuities vs Life Insurance: What's the Real Difference?

You may want to see also

Explore related products

![]()

Enrollment process: ease of application, documentation, and approval timelines for both options

Navigating the enrollment process for health insurance can feel like deciphering a complex puzzle, but understanding the differences between marketplace insurance and insurance exchanges can simplify the journey. Both platforms aim to provide accessible coverage, yet their application procedures, documentation requirements, and approval timelines vary significantly. Let’s break it down.

Application Ease: Streamlined vs. Customized

Marketplace insurance, often facilitated through government platforms like Healthcare.gov, offers a standardized application process. Users typically complete a single, unified form that assesses eligibility for subsidies, Medicaid, or private plans. This one-stop-shop approach is ideal for those seeking simplicity, especially first-time applicants. In contrast, insurance exchanges, which can be state-run or private, often require users to navigate multiple plans and applications. While this may feel overwhelming, it allows for more tailored comparisons and direct communication with insurers, appealing to those who prioritize customization over convenience.

Documentation Demands: What You’ll Need

Both options require proof of identity, income, and citizenship or immigration status. However, marketplace insurance applications often integrate with government databases to verify this information automatically, reducing the need for manual uploads. For instance, income verification may pull directly from IRS records, streamlining the process. Insurance exchanges, particularly private ones, may require more manual submission of documents, such as pay stubs or tax returns. This can add steps but also provides greater control over the information shared.

Approval Timelines: Speed vs. Thoroughness

Marketplace insurance approvals are generally faster, often processed within 24 to 48 hours, thanks to automated systems and standardized criteria. Subsidy eligibility is determined instantly, allowing for immediate plan selection. Insurance exchanges, however, may take 3 to 7 business days, as applications often undergo manual review by insurers. While this delay can be frustrating, it ensures a thorough assessment, particularly for applicants with complex health histories or income situations.

Practical Tips for a Smooth Enrollment

To expedite the process, gather all required documents beforehand, including Social Security numbers, income statements, and employer details. For marketplace applications, double-check your eligibility for subsidies by using the built-in calculators. If opting for an exchange, compare plans side-by-side and consider contacting insurers directly to clarify coverage details. Regardless of the platform, submitting applications during off-peak hours can reduce processing delays.

The Takeaway: Choose Based on Your Needs

If speed and simplicity are your priorities, marketplace insurance offers a frictionless experience. However, if you value customization and are willing to invest time in research, insurance exchanges provide greater flexibility. Understanding these nuances ensures you select the path that aligns best with your circumstances, making enrollment less of a chore and more of a strategic decision.

How to Get Life Insurance for Your Stepfather

You may want to see also

Explore related products

$23.16 $26

![]()

Customer support: quality of assistance, resources, and guidance offered by each platform

The quality of customer support can significantly influence the overall experience of navigating health insurance options, whether through a marketplace or an exchange. Both platforms aim to assist users in understanding complex policies, but their approaches differ in accessibility, depth of resources, and personalized guidance. Marketplaces, often government-run like Healthcare.gov, typically offer standardized support through call centers, online chat, and FAQs. While these resources are reliable, they may lack the personalized touch needed for individuals with unique health needs or complex financial situations. Exchanges, on the other hand, frequently leverage private brokers or agents who provide tailored advice, often at no additional cost to the consumer. This individualized support can be invaluable for those overwhelmed by the sheer volume of options.

Consider the scenario of a 55-year-old self-employed individual with pre-existing conditions. On a marketplace platform, they might rely on general eligibility calculators and broad plan summaries, which could leave gaps in understanding how specific policies cover their chronic medications. In contrast, an exchange might connect them with a licensed agent who can analyze their medical history, income, and preferred providers to recommend the most cost-effective plan. This level of detail is not just convenient—it’s critical for making informed decisions that avoid unexpected out-of-pocket costs.

For those who prefer self-service, marketplaces often excel with user-friendly tools like subsidy estimators and side-by-side plan comparisons. For instance, Healthcare.gov’s "Plan Preview" tool allows users to input their expected medical needs and see estimated annual costs for each plan. However, these tools assume a baseline understanding of insurance terminology, which not all users possess. Exchanges, particularly those with broker networks, often supplement digital resources with educational webinars, workshops, or one-on-one consultations to bridge this knowledge gap. This hybrid approach—combining technology with human expertise—can cater to a wider range of learning styles and needs.

A cautionary note: while exchanges offer more personalized support, the quality of assistance can vary depending on the broker’s experience and training. Consumers should verify an agent’s credentials and ask about their familiarity with specific insurers or plan types. Marketplaces, though more standardized, may have longer wait times during peak enrollment periods, such as the final weeks before deadlines. Proactive users can mitigate this by seeking assistance earlier in the enrollment window or using off-peak hours for calls.

In conclusion, the choice between a marketplace and an exchange for customer support hinges on individual preferences and needs. Marketplaces provide robust, standardized resources ideal for self-directed users, while exchanges offer tailored guidance better suited for those requiring hands-on assistance. By understanding these differences, consumers can select the platform that aligns best with their decision-making style and ensures they receive the support necessary to choose the right insurance plan.

Gerber Life Insurance: Getting Your Money Back

You may want to see also

Frequently asked questions

Marketplace insurance and insurance exchange refer to the same thing—a platform where individuals and families can shop for and purchase health insurance plans. The terms are often used interchangeably, with "marketplace" being the more common term used by the federal government (Healthcare.gov) and "exchange" sometimes used by state-run platforms.

Since marketplace insurance and insurance exchange plans are essentially the same, there is no inherent difference in quality. The key is to compare specific plans available on the platform based on factors like coverage, cost, provider networks, and your healthcare needs.

Costs are the same because marketplace insurance and insurance exchange plans are offered through the same platform. Premiums, deductibles, and out-of-pocket costs depend on the specific plan you choose, not the platform itself. Financial assistance, such as subsidies, is also available through both.

Coverage quality depends on the plan you select, not whether it’s called a marketplace or exchange. All plans on these platforms must meet Affordable Care Act (ACA) standards, offering essential health benefits. Compare plans carefully to find the best fit for your needs.