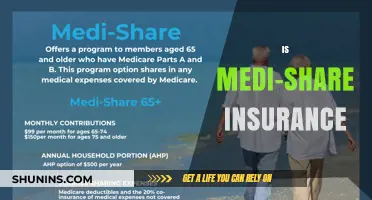

Medi-Share is a faith-based, health care-sharing ministry that operates as an alternative to traditional health insurance. It is not reciprocal insurance in the conventional sense, as it does not involve a contractual agreement between policyholders and an insurer. Instead, Medi-Share members share medical expenses based on biblical principles of mutual support and community. Members pay monthly contributions, which are then used to cover eligible medical expenses of other members. While it functions similarly to insurance by pooling resources to manage health care costs, Medi-Share is not regulated as insurance and does not guarantee coverage for all medical needs. Its reciprocal nature lies in the shared commitment of members to support one another financially during times of medical need, guided by shared religious values.

| Characteristics | Values |

|---|---|

| Type | Medi-Share is not traditional reciprocal insurance. It is a healthcare sharing ministry (HSM). |

| Structure | Members share medical expenses directly with each other, based on Christian principles of mutual aid. |

| Regulation | Not regulated by state insurance departments. Operates under the federal Religious Freedom Restoration Act (RFRA). |

| Eligibility | Requires members to adhere to a Statement of Faith, including agreement with biblical principles and lifestyle guidelines. |

| Coverage | Covers eligible medical expenses after a set Annual Household Portion (similar to a deductible). |

| Pre-existing Conditions | May have waiting periods or limitations for pre-existing conditions. |

| Network | No specific provider network. Members can choose any healthcare provider. |

| Monthly Share Amount | Members pay a monthly share amount based on their chosen program and household size. |

| Sharing Guidelines | Expenses are shared according to specific guidelines outlined in the Medi-Share Member Guidelines. |

| Legal Status | Recognized by the Affordable Care Act (ACA) as an exemption from the individual mandate (until 2019). |

| Tax Treatment | Monthly shares are not tax-deductible as insurance premiums, but may be eligible for Health Savings Account (HSA) contributions. |

| Reciprocal Nature | While not technically reciprocal insurance, Medi-Share operates on a reciprocal sharing model among members. |

Explore related products

What You'll Learn

- Medi-Share Basics: Understanding how Medi-Share operates as a health care sharing ministry

- Reciprocal Insurance Definition: Explaining reciprocal insurance and its legal structure compared to traditional models

- Medi-Share vs. Insurance: Key differences between Medi-Share and conventional health insurance policies

- Eligibility & Coverage: Who qualifies for Medi-Share and what medical expenses are covered

- Legal & Financial Risks: Potential risks and limitations of using Medi-Share as a health care option

![]()

Medi-Share Basics: Understanding how Medi-Share operates as a health care sharing ministry

Medi-Share is not reciprocal insurance but a health care sharing ministry (HCSM) rooted in faith-based principles. Unlike traditional insurance, which pools premiums into a risk pool managed by a company, Medi-Share members share medical expenses directly with one another, guided by biblical values of community and mutual support. This distinction is critical: Medi-Share operates under federal law exemptions for religious organizations, allowing it to bypass certain Affordable Care Act (ACA) regulations, such as covering pre-existing conditions or guaranteeing acceptance. Members must agree to a Statement of Faith, commit to a healthy lifestyle, and pay a monthly "share" amount, which is then distributed to cover eligible medical expenses of other members.

To participate in Medi-Share, individuals or families must first choose a sharing plan based on their needs and budget. Each plan includes an Annual Household Portion (AHP), similar to a deductible, which members must pay out-of-pocket before sharing begins. For example, the Basic plan might have a $5,000 AHP, while the Complete plan could offer a $1,000 AHP but with higher monthly shares. Once the AHP is met, eligible medical expenses—such as hospital stays, surgeries, or maternity care—are shared among members. Notably, Medi-Share does not cover all services; preventive care, mental health treatment, and certain pre-existing conditions may have limitations or require pre-approval. Members are also encouraged to negotiate provider bills, as Medi-Share often reimburses at a discounted rate.

A key aspect of Medi-Share’s operation is its emphasis on member accountability and transparency. Unlike insurance companies, which profit from premiums, Medi-Share is member-driven, with administrative fees deducted from monthly shares to cover operational costs. Members submit medical bills to Medi-Share, which are then reviewed for eligibility and shared with the community. This process fosters a sense of shared responsibility, as members are encouraged to pray for one another and live healthily to minimize collective costs. However, this model also means Medi-Share is not legally obligated to pay claims, though it has a strong track record of fulfilling eligible expenses.

For those considering Medi-Share, understanding its limitations is crucial. While it can offer lower monthly costs compared to traditional insurance, it lacks the legal guarantees of ACA-compliant plans. For instance, Medi-Share may exclude coverage for pre-existing conditions during the first 12 months of membership or deny sharing for lifestyle-related illnesses if members fail to adhere to its health guidelines. Additionally, Medi-Share is not available in all states, and members must be willing to align with its Christian values. Practical tips include thoroughly reviewing the Member Guidelines, maintaining detailed medical records, and exploring supplemental plans for gaps in coverage, such as dental or vision care.

In summary, Medi-Share operates as a faith-driven alternative to traditional insurance, offering a community-based approach to health care sharing. Its structure prioritizes member involvement, transparency, and adherence to religious principles, making it a viable option for those who align with its values. However, potential members must carefully weigh its benefits against the lack of legal protections and coverage limitations. By understanding how Medi-Share functions as an HCSM, individuals can make informed decisions about whether it meets their health care needs and aligns with their beliefs.

Understanding Insurance Prefixes: What They Mean and How They Impact Your Coverage

You may want to see also

Explore related products

![]()

Reciprocal Insurance Definition: Explaining reciprocal insurance and its legal structure compared to traditional models

Reciprocal insurance operates on a unique legal framework that distinguishes it from traditional insurance models. Unlike conventional insurers, which are often structured as stock companies or mutual insurers, reciprocal insurance exchanges are unincorporated associations where members agree to insure one another. This model is facilitated by an attorney-in-fact (AIF), who acts as the legal representative and manages the exchange’s operations. The AIF collects premiums, pays claims, and ensures compliance with state regulations, but the members themselves bear the risk collectively. This structure eliminates the profit motive typical of stock insurers, as any surplus is returned to members or retained for future claims.

To illustrate, consider Medi-Share, a health care sharing ministry (HCSM) often compared to reciprocal insurance. While Medi-Share is not technically a reciprocal exchange, it shares similarities in its member-driven, risk-sharing approach. Members contribute monthly shares to cover one another’s medical expenses, guided by shared values and faith-based principles. In contrast, a true reciprocal insurer like USAA’s reciprocal model (though primarily known for its stock company structure) would involve members legally agreeing to insure one another, with the AIF managing the exchange. This distinction highlights how reciprocal insurance prioritizes mutual obligation over corporate ownership.

Legally, reciprocal insurance exchanges are regulated differently from traditional insurers. They are subject to state insurance laws but often benefit from exemptions or tailored regulations due to their unique structure. For instance, in some states, reciprocal exchanges are not required to maintain the same capital and surplus levels as stock insurers, as members’ collective assets serve as a financial backstop. However, this also means members may face greater liability in the event of significant claims, as they are legally bound by the exchange’s obligations. This risk-sharing aspect underscores the importance of understanding the legal commitments involved in joining a reciprocal exchange.

From a practical standpoint, reciprocal insurance can offer cost savings and flexibility compared to traditional models. Without shareholders demanding profits, premiums may be lower, and members have more control over how funds are allocated. However, this model requires active member participation and trust in the AIF’s management. For example, a small business owners’ reciprocal exchange might pool resources to self-insure against property damage, reducing reliance on external insurers. Yet, such arrangements demand careful planning and legal advice to ensure compliance and mitigate risks.

In conclusion, reciprocal insurance represents a distinct alternative to traditional insurance, emphasizing mutuality and shared risk. Its legal structure, centered on an AIF and member agreements, offers both advantages and challenges. While it can foster cost efficiency and community-driven solutions, it also requires members to accept greater responsibility and understand the legal implications of their participation. Whether considering Medi-Share’s HCSM model or a true reciprocal exchange, individuals and organizations must weigh the benefits of collective risk-sharing against the complexities of this non-traditional insurance framework.

Understanding Comprehensive Life Insurance Coverage

You may want to see also

Explore related products

![]()

Medi-Share vs. Insurance: Key differences between Medi-Share and conventional health insurance policies

Medi-Share is not reciprocal insurance in the traditional sense but rather a health care sharing ministry (HCSM) where members share medical expenses based on Christian principles. Unlike conventional insurance, which is regulated by state and federal laws, Medi-Share operates under religious freedom protections granted by the Affordable Care Act. This distinction is crucial because it means Medi-Share is not legally obligated to cover pre-existing conditions or adhere to the same coverage mandates as standard insurance policies. For example, while a typical insurance plan must cover preventive services at 100%, Medi-Share’s coverage depends on member contributions and shared agreements, which can vary widely.

One key difference lies in how costs are managed. Conventional insurance policies have fixed premiums, deductibles, and copays, providing predictability for policyholders. Medi-Share, however, operates on a monthly share amount, which is similar to a premium but is not guaranteed to cover all medical expenses. Members submit their medical bills to Medi-Share, which then distributes funds from other members to cover eligible expenses. This model can result in lower monthly costs for healthy individuals but may leave members vulnerable to gaps in coverage for unexpected or high-cost treatments. For instance, a $10,000 emergency room visit might be fully covered by insurance but only partially shared by Medi-Share members, depending on their collective contributions.

Another critical distinction is the lack of guaranteed renewability in Medi-Share. Traditional insurance policies cannot be canceled due to health status changes, but Medi-Share reserves the right to terminate membership for lifestyle choices that conflict with its Christian values, such as tobacco use or extramarital relationships. This moral underwriting can exclude individuals who do not align with Medi-Share’s guidelines, whereas conventional insurance must accept all applicants during open enrollment periods. For someone with a chronic condition or a lifestyle that doesn’t meet Medi-Share’s criteria, this could mean being left without coverage options.

From a practical standpoint, Medi-Share’s network limitations are a significant drawback compared to insurance. Most insurance plans have established provider networks, ensuring access to a wide range of doctors and hospitals. Medi-Share, however, does not have a formal network, and members may struggle to find providers willing to accept shared payments. This can lead to out-of-pocket expenses if providers require upfront payment and refuse to bill Medi-Share directly. For example, a specialist might refuse to treat a Medi-Share member unless payment is guaranteed, whereas an insured patient would have coverage through their network.

In conclusion, while Medi-Share offers a faith-based alternative to traditional insurance with potentially lower costs, it lacks the regulatory protections, predictability, and comprehensive coverage of conventional policies. Individuals considering Medi-Share should carefully evaluate their health needs, lifestyle, and financial risk tolerance. For those with pre-existing conditions or a preference for guaranteed coverage, traditional insurance remains the more reliable option. Conversely, healthy individuals aligned with Medi-Share’s values may find it a cost-effective solution, but they must be prepared for potential gaps and limitations in coverage.

Mastering Insurance SOL Preparation: Essential Steps for Success

You may want to see also

Explore related products

![]()

Eligibility & Coverage: Who qualifies for Medi-Share and what medical expenses are covered

Medi-Share, a health care sharing ministry (HCSM), operates on the principle of like-minded individuals pooling resources to cover medical expenses. Unlike traditional insurance, eligibility hinges on shared beliefs and lifestyle choices, not just financial status. To qualify, members must affirm a Christian faith statement, attend church regularly, and abstain from tobacco, illegal drugs, and extramarital sexual activity. This unique eligibility criteria fosters a community of shared values but also limits accessibility for those outside this framework.

Coverage under Medi-Share is comprehensive but not all-encompassing. Routine medical care, including doctor visits, preventive services, and prescriptions, are typically shared among members. Major expenses like hospitalizations, surgeries, and emergency room visits are also covered, often with annual sharing limits ranging from $100,000 to $1 million, depending on the chosen program. However, pre-existing conditions may face a waiting period before they’re eligible for sharing, usually 36 months. Notably, Medi-Share does not cover expenses related to abortion, substance abuse treatment, or injuries from illegal activities, aligning with its faith-based principles.

For families, Medi-Share offers a practical advantage: dependents under 26 are covered under the same membership, simplifying health care management. Monthly share amounts, akin to premiums, vary based on age, household size, and chosen Annual Household Portion (AHP), which functions like a deductible. For instance, a family of four might pay $400–$600 monthly, with an AHP of $1,000–$5,000. This structure provides flexibility but requires careful consideration of potential out-of-pocket costs.

One critical distinction is Medi-Share’s lack of guaranteed coverage. While it operates under federal law as an HCSM, it is not subject to ACA regulations, meaning it doesn’t cover pre-existing conditions immediately or guarantee payment for all eligible expenses. Members rely on the community’s willingness to share, though Medi-Share has a strong track record of fulfilling eligible needs. Prospective members should weigh this against the potential risks, especially if they have ongoing health concerns.

Practical tips for maximizing Medi-Share’s benefits include submitting bills promptly, as delays can affect sharing eligibility. Members should also familiarize themselves with the sharing guidelines, which outline what expenses qualify. For instance, preventive care like vaccinations and cancer screenings are fully shared after the AHP is met. Additionally, Medi-Share’s telehealth services offer convenient, cost-effective access to medical advice, often with no out-of-pocket cost. By understanding these nuances, members can navigate Medi-Share effectively, ensuring they receive the support they need while adhering to its unique framework.

Understanding UMR Insurance: Coverage, Benefits, and How It Works

You may want to see also

Explore related products

![]()

Legal & Financial Risks: Potential risks and limitations of using Medi-Share as a health care option

Medi-Share, a health care sharing ministry (HCSM), operates outside the traditional insurance framework, which introduces unique legal and financial risks for its members. Unlike insurance, Medi-Share is not regulated by state insurance laws or guaranteed by a state insurance fund. This lack of oversight means members have fewer protections if the organization fails to meet its obligations. For instance, if Medi-Share denies a medical expense, members cannot appeal to a state insurance commissioner, leaving them with limited recourse. This regulatory gap underscores the importance of understanding Medi-Share’s limitations before enrolling.

Financially, Medi-Share’s structure exposes members to unpredictable out-of-pocket costs. While monthly share amounts may seem affordable, the program does not guarantee coverage for all medical expenses. Pre-existing conditions, for example, may not be fully covered until a member has been part of the program for several years. Additionally, Medi-Share caps annual sharing limits, leaving members responsible for costs exceeding these thresholds. For instance, a major surgery or chronic illness could result in tens of thousands of dollars in uncovered expenses. Without the safety net of traditional insurance, members must carefully assess their financial ability to handle such risks.

Legally, Medi-Share’s religious exemption from the Affordable Care Act (ACA) creates further complications. While this exemption allows members to avoid the ACA’s individual mandate penalty, it also means Medi-Share is not required to cover essential health benefits like mental health services, maternity care, or prescription drugs. Members relying on these services may find themselves underinsured, facing significant gaps in coverage. Moreover, Medi-Share’s faith-based guidelines exclude certain treatments, such as those related to substance abuse or sexually transmitted infections, which could leave members without critical care options.

To mitigate these risks, prospective Medi-Share members should take proactive steps. First, thoroughly review the program’s guidelines and sharing eligibility criteria to understand what is and isn’t covered. Second, maintain an emergency fund to cover unexpected medical expenses, especially if you have a history of health issues. Finally, consider pairing Medi-Share with supplemental insurance plans, such as accident or critical illness policies, to fill coverage gaps. While Medi-Share can be a cost-effective option for some, its legal and financial risks demand careful consideration and planning.

Understanding Professional Malpractice Insurance: Essential Coverage for Your Career

You may want to see also

Frequently asked questions

Medi-Share is not traditional reciprocal insurance. It operates as a healthcare sharing ministry (HSM), where members share medical expenses based on Christian principles of mutual support.

Reciprocal insurance involves policyholders pooling premiums to cover claims, while Medi-Share relies on members voluntarily sharing medical expenses according to their monthly contributions.

No, Medi-Share is legally classified as a healthcare sharing ministry, not reciprocal insurance. It is exempt from certain insurance regulations under federal law.

Medi-Share does not offer reciprocal insurance benefits. Instead, members share eligible medical expenses within the community, following specific guidelines and eligibility criteria.