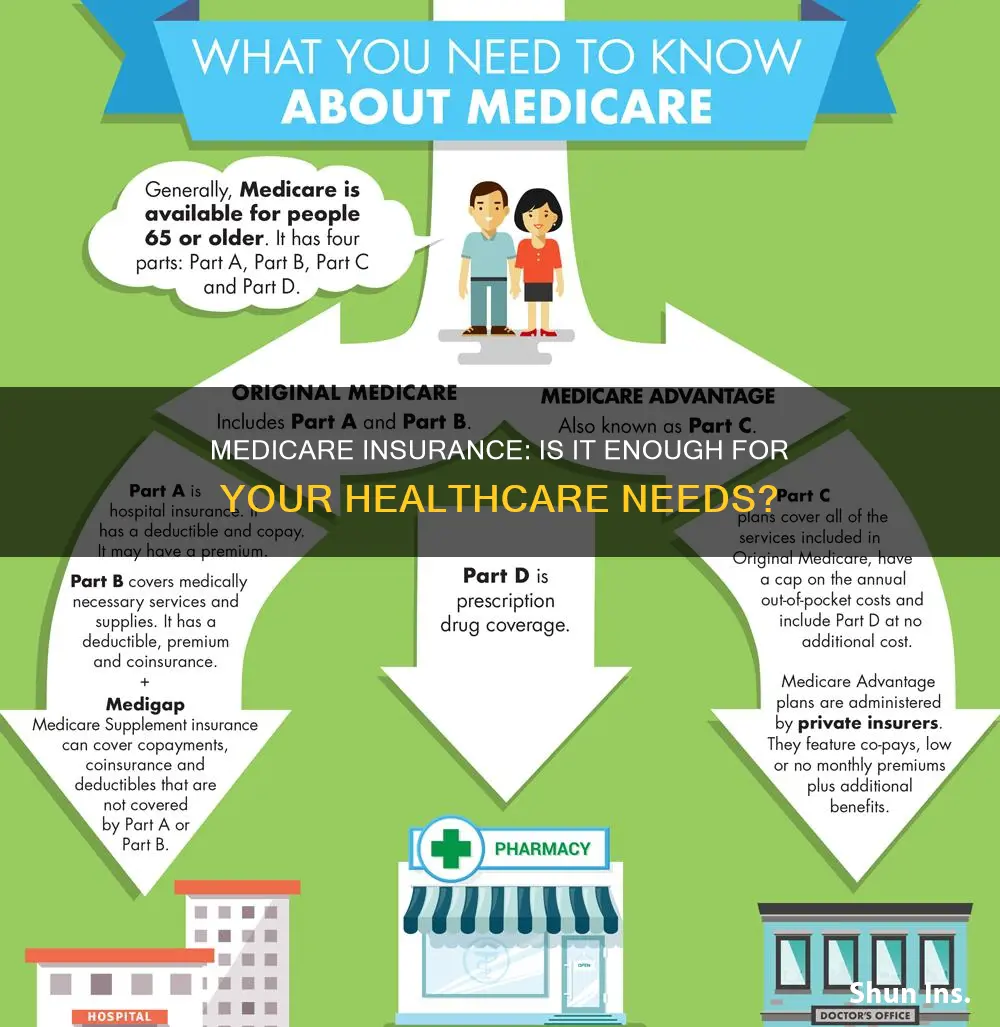

Medicare is a federal insurance program that provides health coverage for people over the age of 65 and some younger people with disabilities. While Medicare Part A and Part B (Original Medicare) provide a solid insurance base, there are gaps in coverage that can lead to significant out-of-pocket expenses for beneficiaries. For example, Original Medicare does not include prescription drug coverage or an out-of-pocket maximum, and it may not cover all hospital stays, inpatient rehabilitation, or skilled nursing facility stays. As a result, many individuals opt for additional coverage, such as Medicare Advantage (Part C) plans or Medicare Supplement Insurance (Medigap) plans, to help cover these gaps and reduce potential financial risks associated with out-of-pocket costs.

Explore related products

What You'll Learn

![]()

Medicare Part A and Part B

Medicare Part A covers inpatient care in hospitals, skilled nursing facility care, hospice care, and some home health services. Most people get Part A for free, but some have to pay a premium for this coverage. To be eligible for premium-free Part A, an individual must be entitled to receive Medicare based on their own earnings or those of a spouse, parent, or child.

Medicare Part B covers medical services and outpatient care, including doctor visits, preventive services, durable medical equipment, and some medical services delivered in an outpatient hospital setting, such as surgeries, diagnostic imaging, and medical supplies. There is typically a premium associated with Part B, and many services come with cost-sharing that the beneficiary must pay, such as coinsurance or copayments.

While Original Medicare provides a solid insurance base, it does not include prescription drug coverage or an out-of-pocket maximum. As a result, beneficiaries with significant medical conditions may face unpredictable healthcare costs. To mitigate this, individuals can consider a Medicare Advantage (Part C) plan, which bundles Part A, Part B, and usually Part D (prescription drug coverage), or they can supplement Original Medicare with a Medigap policy and a Part D plan.

It is important to note that Medicare Advantage plans typically have provider network restrictions, and beneficiaries must be enrolled in Part A or Part B before enrolling in a Medicare Advantage plan. Additionally, Medigap policies are only available for purchase within six months of enrolling in Part B without undergoing medical underwriting.

In conclusion, while Medicare Part A and Part B provide a good foundation for healthcare coverage, many individuals may benefit from additional coverage options to help manage their healthcare costs and ensure their specific needs are met.

Medical Insurance: Understanding Your Personal Data

You may want to see also

Explore related products

$19.95 $14.95

![]()

Medicare Advantage plans

Before enrolling in a Medicare Advantage plan, it is important to speak with your employer, union, or benefits administrator, as joining one of these plans may cause you to lose your existing coverage. Additionally, if a plan decides to stop participating in Medicare, enrollees will need to join another health plan or return to Original Medicare.

Beneficiaries can change their Medicare Advantage plans during specific enrollment periods, such as the Annual Enrollment Period (AEP).

Fertility Treatments: Are They Covered by Medical Insurance?

You may want to see also

Explore related products

![]()

Medigap policies

Medicare Part A and Part B, also known as Original Medicare, generally covers inpatient hospital stays, skilled nursing facility care, doctor visits, outpatient care, preventive services, and durable medical equipment. However, it does not include prescription coverage or an out-of-pocket maximum, which can result in significant financial risk for beneficiaries in the event of a major medical issue.

When enrolling in Medicare Part B, individuals have six months to purchase a Medigap policy without undergoing medical underwriting. After this initial period, insurance companies will consider an individual's health history before offering coverage. The plans are standardized and assigned letters (A, B, C, D, F, G, K, L, M, and N), with some states offering high-deductible versions. While the benefits within each plan type are consistent across insurance companies, not every plan is available in all states.

It is important to note that Medigap plans do not cover costs associated with Part D prescription drug coverage. Additionally, beginning on January 1, 2020, newly sold Medigap plans are no longer allowed to cover the Part B deductible. Individuals considering Medigap should carefully review the available plans and their benefits to ensure they select the most suitable option for their needs.

Florida Medical Insurance: Understanding the Cost

You may want to see also

Explore related products

![]()

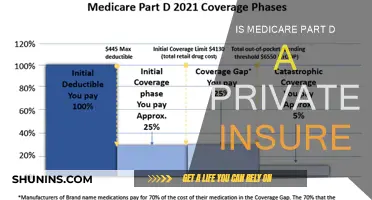

Out-of-pocket costs

Out-of-pocket (OOP) costs are a significant consideration when choosing a Medicare plan. These costs refer to the expenses you must cover beyond what Medicare covers. While Medicare is designed to cover most of your medical expenses, the system was initially designed with high cost-sharing and no out-of-pocket limits for Original Medicare. This means that the more medical services you require, the more you'll pay in Medicare costs.

Medicare Part A (Hospital Insurance) typically doesn't require a premium if you've worked for 10+ years and paid Social Security taxes. However, if you don't qualify for premium-free Part A, you may pay up to $518 monthly in premiums. For a hospital stay, there's also a deductible of $1,676 per benefit period.

Medicare Part B (Medical Insurance) has a standard monthly premium of $185, and a deductible of $257 per year. After meeting the deductible, you'll pay 20% coinsurance for each Medicare-approved service or item, contributing to your total out-of-pocket costs.

Medicare Part D covers prescription drug costs. The monthly premium for standard coverage is estimated to average around $46.50 in 2025, and the deductible can be no more than $590 annually. In 2025, the out-of-pocket spending on covered Part D drugs is capped at $2,000. After meeting this limit, you pay nothing for covered drugs for the rest of the year.

Medicare Advantage Plans (Part C) are offered by private insurance companies and combine Parts A, B, and prescription drug coverage. These plans vary in their premiums, deductibles, coinsurance, and out-of-pocket costs.

Medigap (Supplemental Insurance) policies provide additional coverage for Parts A and B costs. They can help lower your out-of-pocket expenses, and some include benefits like international travel coverage.

To manage out-of-pocket expenses, you can choose plans with lower upfront costs or higher upfront costs with lower out-of-pocket expenses. Additionally, some states offer assistance programs to help with drug plan premiums and cost-sharing. If you have limited income and resources, you may qualify for Extra Help to cover drug costs and avoid the Part D late enrollment penalty.

TRS and Social Security: Medical Insurance Deductions?

You may want to see also

Explore related products

![Medicare and Social Security: [5 in 1] Maximize Your Retirement Benefits, Secure Medical Coverage and Quality Healthcare | Proven Strategies to Protect Your Financial Future Avoiding Costly Mistakes](https://m.media-amazon.com/images/I/71sRJGiWeQL._AC_UL320_.jpg)

![]()

Supplemental insurance

Medicare Supplement Insurance, also known as Medigap, is extra insurance you can buy from a private health insurance company. It helps pay for some of the healthcare costs that Original Medicare (Parts A and B) does not cover, such as coinsurance, copayments, or deductibles. It can also help with cost-sharing aspects of Parts A and B, including deductibles, copays, and coinsurance.

Medigap policies are available to those aged 65 and over enrolled in Medicare Parts A and B, and in some states to those under 65 eligible for Medicare due to disability or end-stage renal disease. When you first enrol in Medicare Part B, you have six months to purchase a Medigap policy without undergoing medical underwriting. After that, you will need to go through medical underwriting unless your state allows special exceptions.

There are several Medigap plans available, each assigned a letter from A to N. The plans differ in what they cover and the benefits provided. For example, Plan F pays your Medicare deductibles, while Plan A does not. Plans A through G generally provide benefits at higher premiums with limited out-of-pocket costs compared to Plans K through N. It is important to note that Medigap plans do not cover any costs associated with Part D prescription drug coverage.

Therefore, it is generally recommended to have some form of supplemental coverage, such as a Medigap policy or a Medicare Advantage Plan, to ensure more predictable healthcare costs and comprehensive protection.

Flight Bookings with Medical Travel Insurance: Best Sites

You may want to see also

Frequently asked questions

Medicare is a federal insurance program that provides health insurance to people over 65 and younger people with disabilities. There are four parts to Medicare: Part A covers inpatient hospital stays, skilled nursing facility care, and some home health services. Part B covers doctor visits, outpatient care, preventive services, and durable medical equipment. Part C, also known as Medicare Advantage, is offered by private insurance companies and covers everything that Parts A and B cover, as well as some additional benefits like vision, hearing, and dental services. Part D is for prescription drug coverage.

Original Medicare (Parts A and B) does not cover everything and has no cap on out-of-pocket costs, meaning that a serious medical issue could result in very high expenses. For this reason, it is generally recommended that people with Original Medicare purchase additional coverage, such as a Medigap policy or a Medicare Advantage plan.

A Medigap policy is a supplemental insurance plan that helps to cover the gaps in Original Medicare coverage. Medigap policies are sold by private insurance companies and can help cover deductibles, copays, and coinsurance. When you first enroll in Medicare Part B, you have six months to purchase a Medigap policy without having to go through medical underwriting.

Medicare Advantage plans, also known as Part C, are offered by private insurance companies and cover everything that Original Medicare covers, as well as some additional benefits. Many Medicare Advantage plans also include prescription drug coverage (Part D). These plans typically have out-of-pocket maximums, which can help protect against high medical costs.