Medicare Advantage (MA) is the privatized portion of Medicare, where tax dollars are funnelled through insurance companies to pay for administrative costs and profits before the remainder is sent to doctors and hospitals. Medicare Advantage insurers have been criticized for making large profits by overcharging for their services. For example, a 2021 KFF paper on health insurer financial performance found that American health insurance companies make 2.5 times as much profit per enrollee on Medicare as they do on their private-sector customers. However, defenders of Medicare Advantage argue that their coding is more accurate and complete, and that the high margins per member occur following years of rapid growth in the market. With Medicare Advantage nearing dominance, it is important to evaluate beneficiaries' experiences and the sustainability of the program.

Explore related products

![[7.5"x3.75",] Healthcare for Profit is A Crime Against Humanity Sticker Healthcare is Human Right Bumper Sticker People Before Profit Sticker Medicare Gift Vinyl Decal for Car Truck](https://m.media-amazon.com/images/I/51SHBCzqx9L._AC_UY218_.jpg)

What You'll Learn

- Medicare Advantage plans are more profitable than traditional Medicare

- Medicare Advantage insurers report higher gross margins per enrollee

- Medicare Advantage insurers' profits are driven by overpayments

- Medicare Advantage plans have higher administrative costs

- Medicare Advantage insurers' profits are impacted by regulatory changes

![]()

Medicare Advantage plans are more profitable than traditional Medicare

Medicare Advantage, or Medicare Part C, is the privatized portion of Medicare. It is a system where tax dollars are funnelled through insurance companies so they can take 15% off the top to pay for administrative costs and profit before sending the remaining 85% to healthcare providers with strings attached. Traditional Medicare, on the other hand, does not funnel money through insurance companies; it pays healthcare providers directly and devotes only 2% of its expenditures to administrative costs.

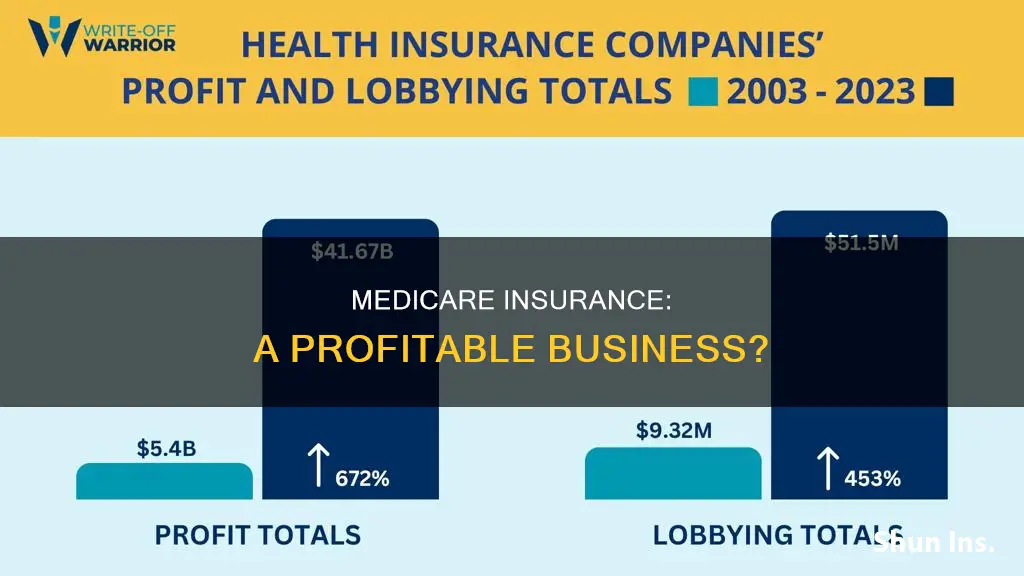

Medicare Advantage plans have been described as a "money grab" by insurance companies, which make 2.5 times as much profit per enrollee on Medicare Advantage as they do on their private-sector customers. A report by Physicians for a National Health Program estimated that the overpayment in 2022 was somewhere between 22% and 35%, meaning the cost of insuring Medicare beneficiaries through Medicare Advantage was between $88 billion and $140 billion more than it would have been through traditional Medicare.

Medicare Advantage plans have also been criticised for their practice of "upcoding", where enrollees are made to look sicker by adding false or irrelevant diagnoses to patient medical records, thus warranting higher reimbursement. Other issues include the requirement for prior authorisation, which can be difficult to obtain, and restrictions on out-of-network care, which can be limited or costly.

Despite these criticisms and the enactment of the Affordable Care Act (ACA) in 2010, which aimed to reduce overpayments to Medicare Advantage plans, the market for these plans has remained strong. This suggests that Medicare Advantage plans continue to be a significant source of profits for insurance companies.

Insurance Medication Denials: Understanding the Complexities

You may want to see also

Explore related products

![[11.5"x3"] Healthcare for Profit is A Crime Against Humanity Sticker Healthcare is Human Right Bumper Sticker People Before Profit Decal for Car Medicare GIF Vinyl Decal for Car Vehicle Window](https://m.media-amazon.com/images/I/51Urk1oI-lL._AC_UY218_.jpg)

![]()

Medicare Advantage insurers report higher gross margins per enrollee

Medicare Advantage insurers have reported much higher gross margins per enrollee compared to insurers in other markets. In 2021, Medicare Advantage insurers reported gross margins averaging $1,730 per enrollee, which was at least double the margins reported by insurers in the individual/non-group market ($745), the fully insured group/employer market ($689), and the Medicaid managed care market ($768). These margins are an indicator of financial performance and signal how much insurers retain after paying for enrollees' medical expenses.

The higher gross margins in the Medicare Advantage market can be attributed to higher medical expenses and premiums for Medicare Advantage enrollees. People on Medicare tend to use more healthcare and incur higher medical expenses than those in the individual and group markets. Additionally, federal payments (premiums) to Medicare Advantage plans are tied to the medical expenses of people in traditional Medicare. As a result, a 5% margin in the Medicare Advantage market represents a larger amount than a 5% margin in the individual or group market.

The Medicare Advantage market has grown substantially in the last decade, with more than 50% of eligible beneficiaries enrolled in a Medicare Advantage plan in 2023. This growth has been spurred by the prospect of strong financial returns, as Medicare Advantage plans offer extra services and benefits that traditional Medicare does not cover. However, it is important to note that gross margins do not necessarily translate directly into profitability, as they do not account for administrative expenses or tax liabilities.

While Medicare Advantage plans have higher gross margins, there are also concerns about overpayment and profitability. According to a report by Physicians for a National Health Program, the cost of insuring Medicare beneficiaries through Medicare Advantage was estimated to be 22% to 35% higher than it would have been through traditional Medicare. This has led to criticisms that Medicare Advantage is a "money grab" by big insurance companies, who are able to profit from tax dollars and higher reimbursements.

In conclusion, while Medicare Advantage insurers report higher gross margins per enrollee, the profitability of these plans is influenced by various factors, including medical expenses, premiums, administrative costs, and potential overpayments. The higher gross margins do not always translate directly into higher profits, and there are ongoing discussions and policy changes aimed at improving alignment between plan costs and payments in the Medicare Advantage market.

Is Your Medical Insurance a Marketplace Plan?

You may want to see also

Explore related products

$14.75

![]()

Medicare Advantage insurers' profits are driven by overpayments

Medicare Advantage, the privatized portion of Medicare, has been criticized for being a "money grab" by big insurers. This is because Medicare Advantage insurers report much higher gross margins per enrollee than insurers in other markets. In 2021, Medicare Advantage insurers reported gross margins averaging $1,730 per enrollee, at least double the margins reported by insurers in other markets. This is due in part to the fact that Medicare Advantage insurers are overpaid by 22% to 39% compared to traditional Medicare, resulting in overpayments of $83 billion to $127 billion in 2024 alone. This is driven by a combination of calculated insurer behaviors and policy design flaws, including "upcoding," which makes patients appear sicker than they are, and selective enrollment of more profitable patients.

The Affordable Care Act (ACA) has made efforts to improve the alignment of plan costs and payments in Medicare Advantage by requiring a Medical Loss Ratio (MLR) of 0.85, which is the share of premiums spent on medical care. However, despite these efforts, Medicare Advantage insurers continue to report higher profits. This may be due to the challenge of obtaining a precise estimate of overpayments that distinguishes legitimate coding from "upcoding."

Medicare Advantage insurers also have higher total revenue per enrollee, with UnitedHealth Group enrolling nearly 7.3 million people. This higher revenue consists largely of taxpayer dollars, as Medicare Advantage funnels tax dollars through insurance companies, allowing them to take a portion for administrative costs and profit before passing the rest on to healthcare providers. This has led to concerns about the value provided by Medicare Advantage, as plans spend 9% less on medical services than traditional Medicare for comparable enrollees, despite the higher costs.

The high margins and profits of Medicare Advantage insurers have made it an attractive market for insurers, with strong market entry and growth. This has resulted in a rapid increase in the number of eligible beneficiaries enrolling in Medicare Advantage plans, with over half of eligible beneficiaries enrolled in 2023. This trend is expected to continue, with projections that Medicare Advantage will enroll 50% of Medicare beneficiaries by 2025 or sooner.

While Medicare Advantage insurers report higher profits, it is important to note that margins can be a misleading indicator of profitability, especially in high-volume industries. Additionally, assessing financial performance ratios can be challenging due to the diverse business portfolios of many large insurers. Despite the challenges in measuring profitability, the combination of higher margins, overpayments, and total revenue suggests that Medicare Advantage insurers are driven by profits, and their financial gains have come at the expense of taxpayers and Medicare funding.

Medical Insurance: A Malaysian Perspective on Coverage and Access

You may want to see also

Explore related products

![]()

Medicare Advantage plans have higher administrative costs

Medicare Advantage, the privatized portion of Medicare, has been described as a "money grab" by insurance companies. These companies take 15% off the top of taxpayer dollars to pay for administrative costs and profits before sending the remaining 85% to doctors and hospitals. This is in contrast to traditional Medicare, which does not funnel money through insurance companies and devotes only around 2% of its expenditures to administrative costs.

The high administrative costs of Medicare Advantage plans can be attributed to several factors, including the practice of ""upcoding," where insurance companies make their enrollees appear sicker to warrant higher reimbursement by adding false or irrelevant diagnoses to patient medical records. Additionally, Congress has mandated pointless and gratuitous bonuses for Medicare Advantage plans, ranging from 2% to 7%, which further increases costs.

The Affordable Care Act (ACA) enacted in 2010 aimed to improve the alignment of plan costs and payments by requiring health plans in Medicare Advantage to attain a Medical Loss Ratio (the share of premiums spent on medical care) of 0.85. While this was intended to reduce overpayments, the actual experience has been quite different, with strong market entry and earnings growth for large insurers. Medicare Advantage plans have also been able to increase their profits through higher margins per enrollee, with gross margins averaging $1,730 per enrollee in 2021, double that of other insurance markets.

To address the high administrative costs of Medicare Advantage plans, there have been proposals to reduce federal payments, which could result in Medicare Advantage enrollees seeing fewer extra benefits and higher costs. Plans could also reduce their administrative costs and profits to make up the difference. However, it is important to note that margins can be a misleading indicator of profitability, especially in high-volume industries. For example, UnitedHealth Group, one of the largest MA insurers, enrolled nearly 7.3 million people in 2019.

VA Life Insurance: No Medical Questions Asked

You may want to see also

Explore related products

![]()

Medicare Advantage insurers' profits are impacted by regulatory changes

Medicare Advantage (MA) is a program offered by private health insurance companies that receive payments from the federal government to provide Medicare-covered services. MA insurers' profits are impacted by regulatory changes in a variety of ways. Firstly, regulatory changes can affect the rates that MA insurers are paid by the Centers for Medicare and Medicaid Services (CMS). For example, there was a 1.12% effective MA rate decrease in the amount paid per enrollee per year by CMS, which resulted in a loss to payers of an average of $150 per member per year. Such changes can have a significant impact on the profitability of MA plans.

Secondly, regulatory changes can impact the Medical Loss Ratio (MLR) requirements for MA plans. The MLR is the share of premiums spent on medical care, and since 2014, MA plans have been required to maintain an MLR of at least 85%. This means that administrative expenses and profits cannot exceed 15% of the total revenues received from the federal government. Changes to the MLR requirements can directly affect the profitability of MA plans.

Thirdly, regulatory changes can affect the risk adjustment methods used by MA plans. CMS has been required to adjust risk scores down over the years, which can impact the profitability of MA plans if they are unable to accurately reflect the risk profiles of their enrollees. Additionally, regulatory changes can impact the benefits that MA plans are required to cover. For example, MA plans are now allowed to include telehealth benefits as part of their basic benefit package, which may increase costs for insurers.

Finally, regulatory changes can impact the market dynamics and competition within the MA industry. For example, changes in MA benefits can lead to increased switching among seniors, as they may be uncertain about their best options. This member churn can result in higher customer acquisition costs for brokers and insurers, affecting their profitability. Overall, MA insurers need to be agile and responsive to regulatory changes to maintain profitability and provide valuable benefits to their members.

Understanding Limited Medical Indemnity Insurance Coverage

You may want to see also

Frequently asked questions

Yes, Medicare Advantage is profitable for insurance companies. Medicare Advantage insurers report much higher gross margins per enrollee than insurers in other markets. In 2021, Medicare Advantage insurers reported gross margins averaging $1,730 per enrollee, at least double the margins reported by insurers in other markets.

Insurance companies profit from Medicare Advantage by taking a cut of the premiums spent on medical care. This is known as the Medical Loss Ratio, which has been set at a minimum of 85% since 2014, meaning that plans' administrative expenses and profits can be no higher than 15% of the total revenues that plans receive from the federal government.

The profitability of Medicare Advantage has increased over time, with more than half of eligible beneficiaries expected to enroll in Medicare Advantage plans in 2023. The gross margins per enrollee for Medicare Advantage insurers in 2021 were similar to the period before the COVID-19 pandemic. However, the program is currently undergoing its biggest shifts in two decades, with regulatory changes affecting rates, risk adjustment, and Star ratings.

There are concerns about the profitability of Medicare Advantage, with critics arguing that insurance companies are vastly overpaid and engage in practices such as upcoding to increase their profits. According to a report from Physicians for a National Health Program, the overpayment in 2022 was estimated to be between 22% and 35%, resulting in excess spending of $88-140 billion.

Medicare Advantage insurers report much higher gross margins per enrollee than traditional Medicare. The administrative expenses for traditional Medicare are relatively low, totaling $10.8 billion or 1.3% of total program spending in 2021. In contrast, the administrative expenses and profits for Medicare Advantage plans are estimated to be higher, with medical loss ratios averaging 83% in 2020.