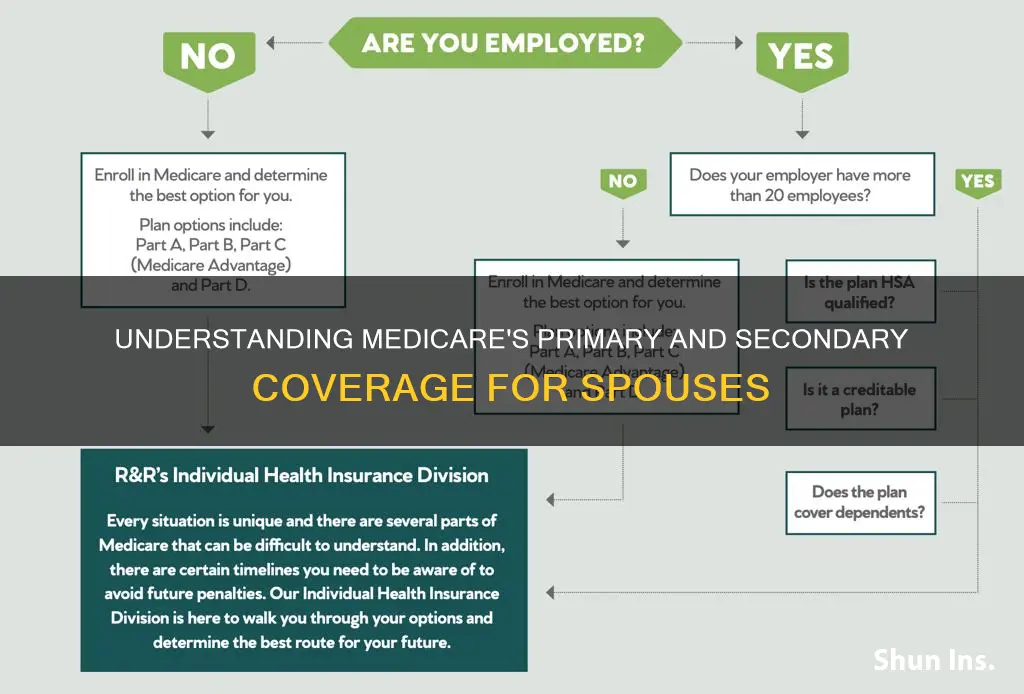

Whether Medicare is primary or secondary to a spouse's insurance depends on the specific circumstances. If an individual has Medicare and other health insurance, each type of coverage is called a payer. The primary payer pays up to the limits of its coverage, then sends the rest of the balance to the secondary payer. Medicare may be the primary payer, while in other cases, it may be the secondary payer. If an individual is covered by their spouse's employer plan and eligible for Medicare, they may choose to delay enrolling until they lose their spouse's employer coverage. If an individual is covered under their spouse's private insurance, they can have Medicare and also be covered by a group plan provided by their spouse's employer.

| Characteristics | Values |

|---|---|

| Medicare as primary payer | If the spouse's company has 20 or more employees, or is a retiree, or has a disability, or has ALS, or has ESRD, or is on active duty |

| Medicare as secondary payer | If the spouse's company has fewer than 20 employees, or is not a retiree, or doesn't have a disability, or doesn't have ALS, or has ESRD, or is not on active duty |

| Medicare not required | If the spouse works for a large employer (20+ employees), or if the spouse's insurance is creditable |

| Medicare Part A only | If the spouse's company has fewer than 20 employees, or if the spouse continues their employer's coverage through COBRA |

| Medicare Part B required | If the spouse's company has fewer than 20 employees, or if the spouse doesn't have creditable prescription drug coverage |

| Medicare Part D required | If the spouse doesn't have creditable prescription drug coverage |

Explore related products

What You'll Learn

![]()

Medicare and private insurance

Medicare is a public health insurance programme provided by the government. Private insurance, on the other hand, is offered by private companies, and many people get private health insurance through a group plan provided by their employers.

If you have Medicare and other health insurance, each type of coverage is called a "payer". The "primary payer" pays up to the limits of its coverage, then sends the remaining balance to the "secondary payer". If the "secondary payer" doesn't cover the remaining balance, the patient may be responsible for the remaining costs.

If you are covered by your spouse's employer plan and are eligible for Medicare, you may have a few options. Firstly, you can delay enrolling in Medicare until you lose your spouse's employer coverage. Secondly, you can enrol in Medicare Part A only and choose to delay Part B and Part D, but you'll need to ensure you have creditable coverage to avoid paying late premium penalties for Part B and/or Part D. Finally, you can enrol in Medicare Parts A & B, Part D prescription drug coverage, or a Medicare Advantage (Part C) plan. You can also look at adding a Medicare supplement insurance plan to Original Medicare (Parts A & B) to help with the out-of-pocket costs of Medicare.

If your spouse works for a large employer (considered a company with 20 or more employees), you don't need to sign up for Medicare at 65. The company-sponsored health insurance will continue to be the primary payer, while Medicare will be the secondary payer. Employers with 20 or more employees must offer the same health benefits to all employees and their spouses, regardless of age, and they can't require you or your spouse to enrol in Medicare at age 65. However, if your spouse works for an employer with fewer than 20 employees, Medicare typically becomes the primary payer at age 65, and the employer coverage is secondary. In that case, you need to sign up for Medicare at 65 or else you may face gaps in coverage.

If you have both Medicare and private insurance, the guidelines will determine which provider pays for your healthcare services first, depending on the specific circumstances and the type of private insurance you have. For example, if you have retiree coverage, Medicare pays first, and your retiree coverage pays second. If you have both Medicare and COBRA, and you are 65 or older, or have a disability, Medicare pays first. However, if you have ESRD, COBRA pays first, and Medicare may pay second.

Medical Insurance: Accident Settlement and Your Payout

You may want to see also

Explore related products

![]()

Primary and secondary payers

When it comes to Medicare and a spouse's insurance plan, the primary and secondary payers depend on various factors, including the size of the employer and the type of insurance coverage. Here is some information on primary and secondary payers:

If your spouse works for a large employer, typically defined as a company with 20 or more employees, their insurance is likely to be the primary payer, and Medicare will be the secondary payer. In this case, you may not need to sign up for Medicare at 65, as the company-sponsored health insurance will cover medical bills first. However, it is important to note that this only applies if you have "creditable coverage," meaning that Medicare considers the coverage to be as good as Medicare Part D.

On the other hand, if your spouse's company has fewer than 20 employees, Medicare typically becomes the primary payer at age 65, and the spouse's employer coverage becomes secondary. In this case, enrolling in Medicare at 65 is essential to avoid gaps in coverage. Additionally, if your spouse is covered under their employer's plan through COBRA (Consolidated Omnibus Budget Reconciliation Act), Medicare may be the primary payer, depending on your specific situation, such as age and the type of coverage.

The coordination of benefits, where the primary payer pays up to its limits and the secondary payer covers the remaining balance, is an important consideration. If Medicare is the secondary payer and there are costs that the primary insurance doesn't cover, you may be responsible for those remaining expenses. Therefore, understanding the coordination of benefits and how your specific plans interact is crucial to avoiding unexpected costs.

It is worth noting that if you are on active duty and have Medicare, TRICARE often pays first for Medicare-covered services, and Medicare pays second. Additionally, if you have coverage through your employer or retiree coverage, Medicare typically pays first, followed by the private insurance as the secondary payer.

When determining primary and secondary payers, it is important to consult official Medicare resources and speak with healthcare benefits professionals to understand how Medicare coordinates with your spouse's insurance plan.

Primary Medical Insurance: What You Need to Know

You may want to see also

Explore related products

$20.65 $29.5

$20.65 $29.5

![]()

Medicare Part A and Part B

Medicare is federal health insurance for anyone aged 65 or older and some people under 65 with certain disabilities or conditions. If you are covered by your spouse's insurance plan and are eligible for Medicare, you have a few options. You can choose to delay enrolling until you lose your spouse's employer coverage, or you can choose to only enrol in Medicare Part A since it usually has no premium. Alternatively, you can enrol in Medicare Parts A & B, Part D prescription drug coverage, or a Medicare Advantage (Part C) plan.

Medicare Part A (Hospital Insurance) helps cover inpatient care in hospitals, skilled nursing facility care, hospice care, and home health care. Most people get Part A for free, but some have to pay a premium for this coverage. To be eligible for premium-free Part A, an individual must be entitled to receive Medicare based on their own earnings or those of a spouse, parent, or child. To receive premium-free Part A, the worker must have a specified number of quarters of coverage (QCs) and file an application for Social Security or Railroad Retirement Board (RRB) benefits.

Medicare Part B (Medical Insurance) is usually paid for, and you must enrol in or already have Part B to keep premium Part A. This means that the person must pay both the premium for Part B and the premium for Part A to keep this coverage. Premium Part A coverage begins the month following the month of enrolment. Medicare Part B is also required for TRICARE For Life (TFL) benefits, which provides expanded medical coverage to Medicare-eligible uniformed services retirees aged 65 or older, to their eligible family members and survivors, and to certain former spouses.

If you have Medicare and other health insurance, each type of coverage is called a "payer". The "primary payer" pays up to the limits of its coverage, then sends the rest of the balance to the "secondary payer". If the "secondary payer" doesn’t cover the remaining balance, you may be responsible for the rest of the costs. The insurance that pays first (primary payer) pays up to the limits of its coverage. The insurance that pays second (secondary payer) only pays if there are costs that the primary insurance didn't cover.

Disclosing Medical Insurance to VA: What You Need to Know

You may want to see also

Explore related products

![]()

Employer size and Medicare

If you are covered by your spouse's employer plan and are eligible for Medicare, you have a few options. You can choose to wait to enrol in Medicare until you lose your spouse's employer coverage, or you can enrol in Medicare Part A only and choose to delay Part B and Part D. However, you need to ensure you have creditable coverage to avoid paying late premium penalties for Part B and/or Part D. It is important to understand how enrolling in Medicare Part A will affect your health savings account (HSA).

The size of the employer determines whether your coverage will be creditable once you retire and are ready to enrol in Medicare Part B. If your employer has 20 or more employees, Medicare deems your group coverage creditable. On the other hand, if your employer has fewer than 20 employees, the coverage is not creditable. If you have creditable coverage, you can delay enrolling in Medicare Part B without incurring late enrolment penalties. When you leave your group health coverage, the insurance carrier will mail you a creditable coverage letter to provide proof of coverage to Medicare.

If your employer is considered a large employer with over 20 employees, you can drop Medicare without penalty. You will be given a Special Enrollment Period (SEP) to enrol when you leave your employer coverage and retire. However, if your employer has less than 20 employees, you need to contact your benefits administrator to find out if the coverage is considered creditable. In this case, it is recommended to enrol in both Medicare Part A and Part B as soon as you are eligible to avoid any gaps in coverage.

The Medicare Secondary Payer (MSP) rules apply to different employer sizes depending on whether the individual is entitled to Medicare based on age or disability. If an employer has 20 or more employees, Medicare is the secondary payer. If an employer has fewer than 20 employees, Medicare is the primary payer. For Medicare entitlement based on disability, the MSP rules apply to employers with at least 100 employees on a typical business day during the previous calendar year. This is defined as a "large group health plan" by the MSP rules.

Wisdom Teeth Removal: Insurance Coverage and Costs

You may want to see also

Explore related products

![Medicare and Social Security: [5 in 1] Maximize Your Retirement Benefits, Secure Medical Coverage and Quality Healthcare | Proven Strategies to Protect Your Financial Future Avoiding Costly Mistakes](https://m.media-amazon.com/images/I/71sRJGiWeQL._AC_UL320_.jpg)

![]()

Medicare and retirement plans

Medicare is considered the "primary payer" for retirees, meaning it pays first for your healthcare costs up to the limits of its coverage. If there is a remaining balance, your retiree insurance plan becomes the "secondary payer". This is known as "coordination of benefits".

Retiree coverage premiums can be costly, but it may be worthwhile to keep your plan if you anticipate high Medicare costs. Retiree coverage may also pay for care or other items and services that Medicare does not cover, such as vision care, dental care, and/or off-formulary or over-the-counter prescription drugs.

If you are covered by your spouse's employer plan and eligible for Medicare, you have several options. You can choose to wait to enrol in Medicare until you lose your spouse's employer coverage, or you can enrol in Medicare Part A only and choose to delay Part B and Part D. However, you will need to ensure you have creditable coverage to avoid paying late premium penalties for Part B and/or Part D. You can also look at adding a Medicare supplement insurance plan to Original Medicare (Parts A & B) to help with the out-of-pocket costs of Medicare.

If you decide to delay enrolling in Medicare, you will have a Special Enrollment Period of eight months that begins when the employer coverage is lost or when your spouse retires. During this time, you can enrol in Medicare Parts A & B, as well as a Part D prescription drug plan.

It's important to understand how retiree coverage works with Medicare, so be sure to talk to your job's benefits administrator and review your plan's description.

Becoming a Medical Insurance Auditor: Steps to Success

You may want to see also

Frequently asked questions

If your spouse works for a large employer (a company with 20 or more employees), you don't need to sign up for Medicare at 65. The company-sponsored health insurance will be the primary payer and will continue to pay medical bills first. Medicare will be the secondary payer. However, if your spouse works for an employer with fewer than 20 employees, Medicare typically becomes the primary payer at 65, and you will need to sign up to avoid gaps in coverage.

If your spouse is still working and you are becoming eligible for Medicare, you may want to consult a Licensed Medicare Agent to find the right plan for you. If you have creditable coverage, you don't need to sign up for Medicare. Your spouse's private insurance coverage is creditable if they work for a company with at least 20 employees.

If you are covered by your spouse's employer plan, you can delay enrolling in Medicare. You will have a Special Enrollment Period of eight months that begins when the employer coverage is lost or when your spouse retires. During this time, you can enroll in Medicare Parts A & B. You can also enroll in a Part D prescription drug plan.