Medicare Supplement Insurance, also known as Medigap, is extra insurance that can be purchased from a private health insurance company to help pay for out-of-pocket costs not covered by Original Medicare (Parts A and B). Medigap policies are designed to 'fill in the gaps' left by Medicare, such as deductibles, copays, and costs incurred when travelling outside the US. They do not typically cover long-term care, vision or dental care, hearing aids, or private-duty nursing. Individuals interested in purchasing a Medigap policy must generally have Original Medicare (Part A and Part B) and will need to pay separate monthly premiums for both.

| Characteristics | Values |

|---|---|

| Type of Insurance | Medicare Supplement Insurance (Medigap) is extra insurance that helps pay your share of out-of-pocket costs in Original Medicare. |

| Who can buy it? | Individuals must have Original Medicare – Part A (Hospital Insurance) and Part B (Medical Insurance) to buy a Medigap policy. |

| Who provides it? | Medigap policies are provided by private health insurance companies. |

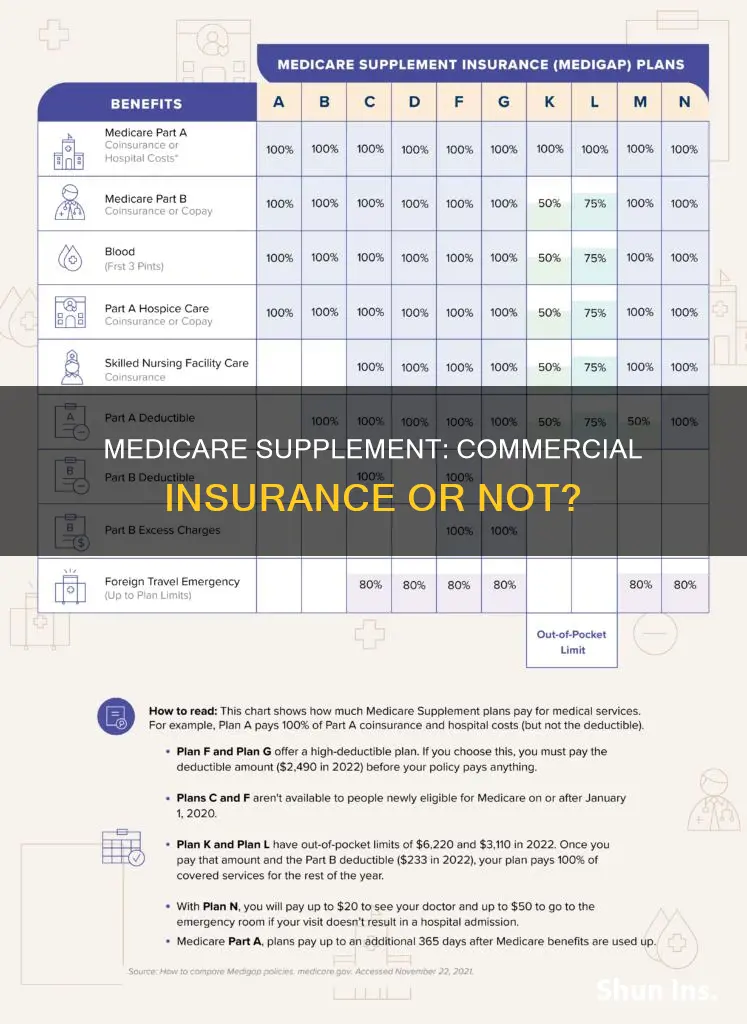

| Cost | The cost of Medigap policies varies, and each plan is identified by a letter. The type and amount of benefits covered by each plan determine the cost. |

| Coverage | Medigap policies generally do not cover long-term care, vision, dental, hearing aids, private-duty nursing, or prescription drugs. Some policies offer coverage when travelling outside the U.S. |

| Spouse Coverage | Your Medigap policy will not cover your spouse; they must purchase an individual policy. |

| Renewability | As long as the premium is paid, Medigap policies are guaranteed renewable and will automatically renew each year. |

Explore related products

What You'll Learn

- Medicare Supplement Insurance (Medigap) is extra insurance bought from private companies

- Medigap policies are available to those under 65 and over 65

- Medigap policies don't cover long-term care, vision or dental care

- Medigap policies are guaranteed renewable as long as premiums are paid

- Medigap policies are standardised and must follow federal and state laws

![]()

Medicare Supplement Insurance (Medigap) is extra insurance bought from private companies

Medicare Supplement Insurance, also known as Medigap, is extra insurance bought from private companies to help pay for out-of-pocket costs in Original Medicare. Medigap policies are designed to fill in the gaps left by Medicare, such as deductibles and copays. Generally, individuals must have Original Medicare, including Part A (Hospital Insurance) and Part B (Medical Insurance), to be eligible for a Medigap policy. It is important to note that Medigap policies do not typically cover long-term care, vision, dental, hearing aids, private-duty nursing, or prescription drugs.

Medigap policies are offered by a variety of private insurance companies, such as Cigna Health and Life Insurance Company, Loyal American Life Insurance Company, and United World Life Insurance. These companies may have different rates and restrictions for their Medigap policies, so it is essential for individuals to review the policy language closely to understand their coverage. Additionally, Medigap policies are guaranteed renewable as long as the individual continues to pay their premiums.

When an individual has both Medicare and Medigap insurance, they have two "payers" for their healthcare costs. Medicare, as the "primary payer", pays its approved amount first, after which the Medigap insurance, as the "secondary payer", covers the remaining costs as per the policy terms. It is important to understand the coordination of benefits between Medicare and Medigap to avoid unexpected costs.

Medigap policies can vary in terms of the benefits and coverage they offer. Each Medigap plan is identified by a letter, and the type and amount of benefits covered by each plan determine its cost. Some Medigap policies may offer additional benefits not covered by Medicare, such as coverage for travel outside the US. However, Medigap policies do not cover all types of expenses, and individuals should carefully review the specific benefits and exclusions of their chosen plan.

Individuals interested in purchasing a Medigap policy can explore their options by reviewing the list of Medicare Supplement Insurance companies and their respective plans. They can also contact their State Health Insurance Assistance Program (SHIP) for free personalized health insurance counselling to make informed decisions about their Medigap choices.

Commercial Vehicle Insurance: Saving Money, Saving Time

You may want to see also

Explore related products

![Medicare and Social Security: [5 in 1] Maximize Your Retirement Benefits, Secure Medical Coverage and Quality Healthcare | Proven Strategies to Protect Your Financial Future Avoiding Costly Mistakes](https://m.media-amazon.com/images/I/71sRJGiWeQL._AC_UY218_.jpg)

![]()

Medigap policies are available to those under 65 and over 65

Medicare Supplement Insurance, commonly known as Medigap, is extra insurance that helps pay for "gaps" in Medicare payment. Medigap policies are available to those under 65 and over 65, but the rules and availability vary by state. While federal law requires insurance companies that sell Medigap policies to follow certain consumer protection requirements, these only apply to beneficiaries who are 65 and older.

For those under 65, eligibility for Medigap depends on qualifying for traditional Medicare due to a disability or End-Stage Renal Disease (ESRD). However, there is no uniform regulation among the states regarding the guaranteed issue of Medigap policies for this group, and many beneficiaries under 65 face barriers to purchasing these policies due to restricted access and higher premium costs. In some states, insurers are allowed to charge significantly higher premiums for enrollees under 65, making Medigap policies prohibitively expensive for younger beneficiaries.

Some states, such as Rhode Island, Hawaii, Idaho, Illinois, Indiana, Kansas, Kentucky, Maine, and South Dakota, have implemented laws or proposed legislation to address this issue. These states have enacted provisions to ensure access to supplemental coverage for Medicare beneficiaries under 65, with some states requiring Medigap insurers to offer all their plans to any newly eligible Medicare beneficiary, regardless of age. Additionally, some states have rating restrictions that prevent insurers from charging higher premiums for enrollees under 65 or limit the additional premiums that can be applied.

It is important to note that Medigap policies do not cover long-term care, vision, dental, hearing aids, private-duty nursing, or prescription drugs. However, some Medigap policies offer coverage when travelling outside the US.

Insuring Your Own Commercial Vehicle in Texas

You may want to see also

Explore related products

![]()

Medigap policies don't cover long-term care, vision or dental care

Medicare Supplement Insurance, also known as Medigap, is an additional insurance policy that can be purchased from a private health insurance company. It helps to cover out-of-pocket costs associated with Original Medicare (Part A and Part B), such as deductibles, copayments, and coinsurance. However, it is important to note that Medigap policies generally do not include coverage for long-term care, vision, or dental care.

Long-term care, such as care provided in a nursing home, is not typically covered by Medigap policies. If individuals require extended care services, they may need to explore other options, such as long-term care insurance or alternative coverage plans. Medigap is designed to supplement traditional Medicare coverage and does not extend to long-term care expenses.

Vision care is also excluded from Medigap coverage. Original Medicare does not include routine eye exams or vision correction services. While Part A of Medicare may cover vision-related medical emergencies, such as traumatic eye injuries requiring hospital admission, Medigap policies do not typically provide benefits for routine vision care or corrective eyewear. Individuals seeking coverage for eye exams, eyeglasses, or contact lenses would need to explore alternative options beyond Medigap.

Similarly, dental care is generally not covered by Medigap policies. Original Medicare does not include routine dental exams, x-rays, cleanings, or comprehensive dental services. While Part A may cover dental procedures performed in a hospital setting, such as jaw surgery, Medigap plans do not typically extend to routine or preventive dental care. Individuals requiring dental services beyond emergency or hospital-based procedures would need to seek alternative coverage options.

It is worth noting that while Medigap policies do not directly cover these areas, they can still provide indirect assistance. For instance, some Medigap plans offer coverage for emergency medical care when travelling outside the United States, which could include dental or vision emergencies. Additionally, Medigap plans can help beneficiaries budget for their dental and vision care needs by making overall healthcare costs more predictable. However, for comprehensive coverage of long-term care, vision, and dental services, individuals may need to consider supplemental policies or alternative insurance plans tailored to these specific needs.

Strategies for Negotiating with Insurance Adjusters After a Collision: A Comprehensive Guide

You may want to see also

Explore related products

$9.97 $19.99

$8

![]()

Medigap policies are guaranteed renewable as long as premiums are paid

Medicare Supplement Insurance, also known as Medigap, is an additional insurance that can be purchased from a private health insurance company. It helps pay for some of the out-of-pocket costs associated with Original Medicare, which includes Part A (Hospital Insurance) and Part B (Medical Insurance). Medigap policies are designed to fill the "gaps" in Original Medicare coverage, and the insured pays a monthly premium to the Medigap insurance company.

The right to purchase a Medigap policy is guaranteed under certain circumstances. For example, if an employer stops providing insurance that covers all of Medicare's 20% co-insurance, the individual has the right to buy a Medigap policy without undergoing health screenings or waiting periods. Additionally, open enrollment rights have been extended to include situations where individuals lose their employer coverage (COBRA) or experience an increase in income or assets that makes them eligible for "Medi-Cal with a share of cost."

It is important to note that Medigap policies may vary by state, and not all plans are offered in every state. Individuals considering Medigap coverage should research the options and costs available in their state. Additionally, Medigap policies do not cover certain expenses, such as long-term care, vision, dental, hearing aids, private-duty nursing, or prescription drugs.

Flood Insurance: Worth the Cost?

You may want to see also

Explore related products

![]()

Medigap policies are standardised and must follow federal and state laws

Medicare Supplement Insurance, also known as Medigap, is extra insurance that helps pay some of the healthcare costs that the Original Medicare Plan doesn't cover. Generally, when buying a Medigap policy, you must already have Medicare Part A (Hospital Insurance) and Part B (Medical Insurance).

Medigap policies are standardized and must adhere to federal and state laws. As of July 31, 1992, Medigap policies were standardized across the United States due to legislation passed by Congress through the Omnibus Budget Reconciliation Act of 1990. This mandatory standardization ensures that Medigap policies follow certain guidelines and offer specific benefits. Insurance companies are only permitted to sell these "standardized" Medigap policies, and individuals with an old policy are encouraged to switch to the new standardized plans to avoid unnecessary costs of duplicate coverage.

There are ten specific benefit plans that federal law permits to be sold as Medigap policies, with two additional plans added in 2006. While states may allow the marketing of all or some of these plans, there is a basic benefit package, known as the "core benefit" plan, that must be offered in all states and by all companies selling Medigap insurance. This core benefit plan serves as the foundation for the other policies, which include additional benefits on top of the core offering.

It's important to note that Medigap policies do not cover all expenses. For example, they typically do not cover long-term care, vision, dental, hearing aids, private-duty nursing, or prescription drugs. Additionally, in some states like Massachusetts, Minnesota, and Wisconsin, Medigap policies are standardized differently, and it is crucial to be aware of illegal practices by insurance companies when shopping for a Medigap policy.

Medigap policies provide supplemental coverage to help pay your share of costs in the Original Medicare plan. They are designed to work alongside your existing Medicare coverage and fill in some of the gaps in out-of-pocket expenses. By understanding the standardization and legal framework surrounding Medigap policies, individuals can make informed decisions about their healthcare coverage options.

In-House Insurance Adjusters: Walking the Legal Tightrope

You may want to see also

Frequently asked questions

Medicare Supplement Insurance, also known as Medigap, is extra insurance that helps pay your share of out-of-pocket costs in Original Medicare. It is purchased from a private health insurance company and is used to fill in the gaps left by Medicare.

Medicare Supplement Insurance covers costs such as deductibles and copays. Some policies also offer coverage for travel outside the U.S. and additional benefits not covered by Medicare. However, Medigap policies generally do not cover long-term care, vision, dental, hearing aids, private-duty nursing, or prescription drugs.

To purchase a Medigap policy, you must have Original Medicare, which includes Part A (Hospital Insurance) and Part B (Medical Insurance). Medicare Supplement Insurance is available to individuals under and over the age of 65.