Medicare Supplement Insurance, also known as Medigap, is an optional add-on that can fill the gaps in Medicare Part A and Part B. While it is not mandatory, Medigap could be beneficial for many seniors as a way to cover the gaps left by other insurance coverage. It is important to consider the costs and benefits of Medigap plans in relation to your personal situation, as premiums vary by insurance company, plan type, location, age, and health status. Ultimately, Medigap can provide peace of mind and protect against unexpected and expensive high deductibles, copays, and coinsurance.

| Characteristics | Values |

|---|---|

| Purpose | Fills "gaps" in Medicare Part A and Part B |

| Cost | Premiums vary by plan type, location, age, insurance company, and health status |

| Coverage | Covers deductibles, copays, and coinsurance |

| Peace of Mind | Protects against unexpected and expensive costs |

| Doctor Choice | No referral needed to see any doctor |

| Pros | Brings predictability and peace of mind |

| Cons | Additional cost during retirement |

| Eligibility | Must have Original Medicare (Part A and Part B) |

| Alternatives | Medicare Advantage Plan |

Explore related products

What You'll Learn

![]()

Medicare Supplement Insurance (Medigap) is optional

Medicare Supplement Insurance, or Medigap, is an optional add-on that can fill "gaps" in Medicare Part A and Part B. It is extra insurance that you can buy from a private health insurance company to help pay your share of out-of-pocket costs in Original Medicare. You're not required to sign up for Medicare Supplement Insurance, but it can be beneficial in certain situations.

Medicare Part A and Part B don't have maximum out-of-pocket caps, so there's no limit on what you could owe in copays and coinsurance. Medigap policies can help put a cap on these yearly costs. For example, if you had a $100,000 surgery and Medicare Part B covered 80%, you would still owe $20,000 yourself. A Medigap policy could help cover this large bill.

Additionally, Medigap can give you more flexibility in choosing your doctor. As John Hill, president of Gateway Retirement, points out, "You may also want to consider a supplement when you want your doctor and not the insurance company in charge of your care. A supplement does not require a referral to see any doctor."

However, Medigap is not for everyone. If you're generally healthy and have other coverage that takes care of most of your medical expenses, you may not need it. Also, if the cost of the premiums is a stretch for your budget, there are other options to consider. It's important to weigh the pros and cons and consider your overall health, family history, how often you see a doctor, and your lifestyle before deciding if Medigap is right for you.

While Medigap is optional, it can provide valuable peace of mind and protection against unexpected and expensive medical costs. However, it's essential to consider your unique financial situation, health, and lifestyle goals before deciding if it's worth it for you.

How to Remove Your Adult Son from Your Health Insurance

You may want to see also

Explore related products

![]()

Medigap covers gaps in Medicare Part A and B

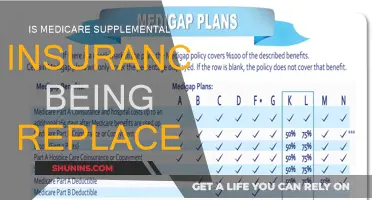

Medicare Supplement Insurance, also known as Medigap, is an optional add-on that can fill the "gaps" in Medicare Part A and Part B. Medigap policies help cover out-of-pocket costs associated with Original Medicare, such as deductibles, copays, and coinsurance. While it is not mandatory to purchase a Medigap policy, it can provide financial protection against unexpected or high medical expenses.

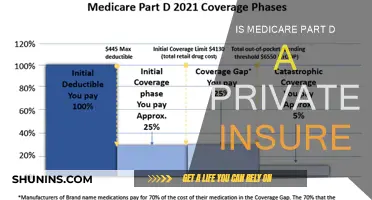

Medigap plans generally help cover the beneficiary's share of costs for services that are covered by Original Medicare (Part A and Part B). These costs can include deductibles, copays, and coinsurance. It's important to note that Medigap policies only cover one person, so spouses would each need their own policy. Additionally, Medigap plans do not include prescription drug coverage; for that, a separate Medicare drug plan (Part D) can be enrolled in.

The benefits offered by each Medigap plan are standardised, but premiums can vary depending on the insurance company, the specific plan chosen, and the beneficiary's location. As such, it is recommended to compare prices and plans to find the best option for one's needs and budget. While Medigap can provide valuable financial protection, it may not be necessary for everyone. Individuals who are generally healthy and have other coverage for most of their medical expenses may not need the additional protection offered by Medigap.

Medigap can be particularly beneficial for individuals who value having a choice of doctors and do not want the insurance company to dictate their care. Additionally, for those who want peace of mind and predictability in their medical expenses, Medigap can help protect against unexpected high costs. However, it is important to consider one's overall health, family history, frequency of doctor visits, and lifestyle when deciding whether to enrol in Medigap.

How to Negotiate Medical Bills with Your Insurance Provider

You may want to see also

Explore related products

![Property and Casualty Insurance License Exam Study Guide: Property Casualty Insurance Book and Practice Test Questions [3rd Edition]](https://m.media-amazon.com/images/I/71MhA+5nDML._AC_UY218_.jpg)

![]()

Medigap policies have varying premiums

Medicare Supplement Insurance, or Medigap, is an optional add-on that fills the "gaps" in Medicare Part A and Part B. Medigap policies have their own premiums, which vary by plan type, location, age, health status and insurance company. The premiums could be different, but the benefits will be the same. For instance, you can expect to pay $100-$150 per month or more for the popular Medigap Plan G, when you sign up at age 65. Plan G will be more expensive if you sign up at an older age.

Medigap Plan K may have a lower premium because it only covers 50% of Medicare Part B coinsurance. On the other hand, Plan C covers the entire Medicare Part B coinsurance but will likely charge a higher monthly premium. The Medigap plans with the most comprehensive coverage can have the highest premiums. If you access lots of healthcare, one way to make the most of your costs upfront and savings later is to choose a plan with a high deductible, which offers lower premiums.

The Medicare Supplement Open Enrollment period is the six-month period that starts the first day of the month in which you turn 65 and are enrolled in Medicare Part B. Some states may have additional open enrollment periods, including for people under 65.

Government-Assisted Medical Insurance: What You Need to Know

You may want to see also

Explore related products

![]()

Medigap policies can be expensive

The cost of Medigap policies varies by insurance company, plan, and location. The premium prices differ, but the benefits remain the same across companies. For example, Medigap Plan G offers identical coverage across all companies, but the premium amount varies. Medigap Plan K has a lower premium because it only covers 50% of Medicare Part B coinsurance, while Plan C covers 100% of Medicare Part B coinsurance but charges a higher monthly premium.

The decision to purchase a Medigap policy depends on your financial situation, health, and lifestyle goals. If you are generally healthy and have other coverage that takes care of most of your medical expenses, you may not need Medigap insurance. Additionally, if the premium costs are a strain on your budget, you may want to consider other options. It is important to weigh the pros and cons of Medigap insurance and evaluate whether the benefits outweigh the costs for your personal situation.

While Medigap policies can be expensive, they offer valuable protection against unexpected and costly deductibles, copays, and coinsurance. Medigap fills the "`gaps`" in Medicare Part A and Part B, providing peace of mind and predictability for seniors. By paying more upfront for premiums, you can limit your future out-of-pocket spending and protect your finances from high medical costs.

Medical Insurance Premiums: Tax-Deductible Monthly Expenses?

You may want to see also

Explore related products

![Medicare and Social Security: [5 in 1] Maximize Your Retirement Benefits, Secure Medical Coverage and Quality Healthcare | Proven Strategies to Protect Your Financial Future Avoiding Costly Mistakes](https://m.media-amazon.com/images/I/71sRJGiWeQL._AC_UL320_.jpg)

![]()

Medigap policies are beneficial for seniors

Medicare Supplement Insurance, or Medigap, is an optional add-on that can fill "gaps" in Medicare Part A and Part B. Medigap plans generally help cover out-of-pocket costs for services that are covered by Original Medicare (Part A and Part B). The benefits are different for each plan, and you can buy the one that meets your needs.

Medigap could also be beneficial for seniors who value doctor choice. A supplement does not require a referral to see any doctor, so you can choose your doctor rather than the insurance company being in charge of your care.

Additionally, Medigap policies can provide peace of mind for seniors, knowing that if Medicare covers it, their supplements will too. With Medicare supplements, there won't be any medical cost surprises, which could wreck your budget.

Medigap may not be for everyone, and deciding whether to opt for it will depend on an individual's financial situation, health, lifestyle goals, and other considerations. For example, if you are pretty healthy and have other coverage that takes care of most of your medical expenses, you might not need Medigap. Additionally, if the cost of the premiums feels like too much of a stretch for your budget, you may need to consider other options.

Understanding Medical Insurance Networks: In and Out

You may want to see also

Frequently asked questions

Medicare Supplement Insurance, also known as Medigap, is extra insurance that can be purchased to help pay for out-of-pocket costs in Original Medicare (Part A and Part B). Medigap policies fill in the gaps in coverage that exist in Original Medicare.

Medicare Supplement Insurance can provide peace of mind by protecting against unexpected and expensive deductibles, copays, and coinsurance costs. It gives you the freedom to choose your doctor without needing a referral and ensures that you won't face surprises with medical costs. Additionally, Medigap plans can put a cap on your yearly expenses, preventing them from adding up to large amounts.

The main downside is the additional cost. You need to pay premiums throughout the year, which can be a significant expense, especially if you don't end up needing extensive medical treatment. Additionally, Medigap plans do not cover costs for prescription drugs, dental care, routine eye care, or long-term care.

The decision depends on your personal situation, including your financial situation, health, lifestyle goals, and budget. Consider your overall health, family history, frequency of doctor visits, and whether you value having a choice of doctors. Evaluate the potential costs, such as premiums, deductibles, copays, and how they would impact your budget. If you're generally healthy, have other adequate coverage, and the premiums are a strain on your budget, you may not need Medicare Supplement Insurance.