Medigap and supplemental insurance are terms often used interchangeably, but they specifically refer to the same type of insurance product designed to cover costs that original Medicare doesn’t, such as copayments, coinsurance, and deductibles. Medigap, officially known as Medicare Supplement Insurance, is a standardized policy sold by private insurance companies to fill the gaps in Medicare coverage, ensuring beneficiaries have more predictable out-of-pocket expenses. While supplemental insurance is a broader term that can refer to any policy that complements primary insurance, in the context of Medicare, it typically means the same thing as Medigap. Understanding this distinction is crucial for Medicare beneficiaries seeking to enhance their coverage and minimize unexpected healthcare costs.

Explore related products

What You'll Learn

![]()

Medigap vs. Supplemental Insurance: Definitions

Medigap and supplemental insurance are terms often used interchangeably, but they refer to specific types of coverage with distinct characteristics. Medigap, also known as Medicare Supplement Insurance, is specifically designed to work alongside Original Medicare (Part A and Part B). Its primary purpose is to help cover out-of-pocket costs that Medicare doesn’t pay, such as copayments, coinsurance, and deductibles. Medigap policies are standardized by the federal government, meaning plans labeled with the same letter (e.g., Plan G) offer identical benefits regardless of the insurance company selling them. This standardization ensures clarity and consistency for beneficiaries.

Supplemental insurance, on the other hand, is a broader term that refers to any additional health insurance policy designed to cover costs not addressed by a primary insurance plan. Unlike Medigap, supplemental insurance is not exclusive to Medicare beneficiaries. It can be paired with employer-sponsored health plans, individual health insurance, or other primary coverage. Examples of supplemental insurance include dental, vision, critical illness, accident, or hospital indemnity policies. These plans provide extra financial protection but are not standardized and can vary widely in terms of coverage and benefits.

While Medigap is a type of supplemental insurance, not all supplemental insurance is Medigap. The key distinction lies in their scope and application. Medigap is strictly tied to Medicare and follows federal regulations, whereas supplemental insurance can be tailored to a variety of primary insurance plans and may cover non-medical expenses or specific health-related needs. For instance, a hospital indemnity plan (a form of supplemental insurance) pays a fixed amount for each day of hospitalization, regardless of actual costs, whereas Medigap covers specific Medicare-related expenses.

Another important difference is eligibility. Medigap is available only to individuals enrolled in Original Medicare, typically those aged 65 and older or with certain disabilities. Supplemental insurance, however, has no such restrictions and can be purchased by anyone seeking additional coverage beyond their primary plan. This flexibility makes supplemental insurance a versatile option for a broader audience, while Medigap remains a targeted solution for Medicare beneficiaries.

In summary, while both Medigap and supplemental insurance aim to provide additional financial protection, their definitions and applications differ significantly. Medigap is a standardized, Medicare-specific supplement, whereas supplemental insurance is a broader category of coverage that can be paired with various primary plans. Understanding these distinctions is crucial for individuals seeking to enhance their health insurance coverage and ensure they choose the right policy for their needs.

Life Alert: Insurance Coverage and Your Options

You may want to see also

Explore related products

![]()

Key Differences in Coverage

Medigap and supplemental insurance are terms often used interchangeably, but they are not exactly the same, especially when it comes to coverage. While both types of policies are designed to help cover costs that original Medicare doesn’t pay, such as copayments, coinsurance, and deductibles, there are key differences in their scope and structure. Understanding these differences is crucial for making an informed decision about which type of coverage best suits your healthcare needs.

Coverage Standardization in Medigap vs. Variability in Supplemental Insurance

One of the most significant differences lies in the standardization of Medigap plans compared to the variability of supplemental insurance. Medigap plans, also known as Medicare Supplement Insurance, are standardized by the federal government and labeled with letters (e.g., Plan G, Plan N). Each plan offers the same benefits regardless of the insurance company selling it. For example, Medigap Plan G covers the Medicare Part A deductible, coinsurance, and Part B coinsurance or copayments consistently across all providers. In contrast, supplemental insurance plans are not standardized and can vary widely in terms of coverage, benefits, and costs depending on the insurer and the state. This variability means that two supplemental insurance policies from different companies may offer entirely different levels of coverage for the same healthcare services.

Coverage for Additional Benefits

Another key difference is the inclusion of additional benefits beyond what original Medicare covers. Medigap plans primarily focus on filling the gaps in Medicare coverage, such as deductibles and coinsurance, but they do not typically cover services like dental, vision, hearing, or prescription drugs. For these additional benefits, beneficiaries would need separate plans, such as Medicare Part D for prescription drugs. Supplemental insurance, on the other hand, often includes additional benefits that Medigap does not cover. For instance, some supplemental plans may offer coverage for routine dental care, vision exams, hearing aids, or even gym memberships. These extra benefits can make supplemental insurance more appealing to individuals seeking comprehensive coverage beyond what Medicare provides.

Coverage for Out-of-Pocket Maximums

Medigap plans do not typically include an out-of-pocket maximum, meaning there is no cap on the amount a beneficiary might pay in a given year for covered services. While Medigap helps cover specific costs like copayments and deductibles, the total out-of-pocket expenses can still accumulate without a limit. Supplemental insurance, however, may offer policies with out-of-pocket maximums, providing beneficiaries with greater financial predictability. Once the out-of-pocket limit is reached, the supplemental insurance plan covers all additional costs for covered services, which can be particularly beneficial for individuals with chronic conditions or those requiring frequent medical care.

Coverage for International Travel

A notable difference in coverage between Medigap and supplemental insurance is the inclusion of emergency care during international travel. Medigap plans, specifically Plans C through G, offer coverage for emergency medical care when traveling outside the United States, up to a certain lifetime limit. This benefit can provide peace of mind for beneficiaries who travel frequently. Supplemental insurance plans, however, rarely include international travel coverage. Most supplemental policies are designed to complement Medicare within the United States and do not extend benefits abroad. This distinction is critical for individuals who prioritize international travel and need coverage for emergency medical situations while overseas.

Coverage for Provider Networks

Finally, the flexibility in choosing healthcare providers differs between Medigap and supplemental insurance. Medigap plans allow beneficiaries to visit any doctor or hospital that accepts Medicare, providing a high degree of flexibility in choosing healthcare providers. There are no network restrictions, which can be particularly advantageous for individuals who require specialized care or prefer specific providers. Supplemental insurance, however, may require beneficiaries to use in-network providers to receive full coverage. These plans often operate within specific networks, and using out-of-network providers may result in higher out-of-pocket costs or limited coverage. This network restriction can be a significant factor for individuals who prioritize provider choice and flexibility in their healthcare coverage.

In summary, while both Medigap and supplemental insurance aim to enhance Medicare coverage, they differ significantly in terms of standardization, additional benefits, out-of-pocket maximums, international travel coverage, and provider network requirements. Understanding these key differences is essential for selecting the plan that best aligns with your healthcare needs and financial situation.

Becoming a Life Insurance Agent: New York Requirements

You may want to see also

Explore related products

![]()

Eligibility and Enrollment Rules

Medigap, also known as Medicare Supplement Insurance, is a type of supplemental insurance designed to cover certain out-of-pocket costs that Original Medicare (Part A and Part B) doesn’t fully pay. While Medigap and supplemental insurance are often used interchangeably, Medigap specifically refers to policies standardized by the federal government to complement Medicare. Understanding the eligibility and enrollment rules for Medigap is crucial for anyone considering this coverage.

Eligibility for Medigap is primarily tied to enrollment in both Medicare Part A and Part B. Individuals must be at least 65 years old or under 65 with certain disabilities or medical conditions to qualify for Medicare and, subsequently, Medigap. It’s important to note that Medigap policies are sold by private insurance companies, and eligibility does not depend on income or health status, except in certain circumstances. During the six-month Medigap Open Enrollment Period, which begins when you turn 65 and are enrolled in Part B, insurers cannot deny you coverage or charge more based on pre-existing conditions.

Enrollment rules for Medigap are strict and time-sensitive. The best time to enroll is during the Medigap Open Enrollment Period, as this is the only guaranteed issue period. Outside of this window, insurers may require medical underwriting, potentially leading to higher premiums or denial of coverage based on health conditions. Some states offer additional guaranteed issue rights, such as when an individual loses employer-based coverage or moves out of a plan’s service area. It’s essential to research state-specific rules, as they can vary significantly.

Individuals under 65 who qualify for Medicare due to disabilities or medical conditions may face challenges in obtaining Medigap coverage, as federal law does not require insurers to offer Medigap policies to this group. However, some states have laws mandating Medigap availability for younger Medicare beneficiaries. If you fall into this category, check your state’s regulations to understand your options.

Finally, it’s important to know that Medigap policies are individual, meaning they cover only one person. Married couples must each purchase their own policy. Additionally, Medigap cannot be paired with Medicare Advantage plans; if you have a Medicare Advantage plan, you must switch back to Original Medicare to enroll in Medigap. Understanding these eligibility and enrollment rules ensures you make informed decisions about supplementing your Medicare coverage.

Robo-Investors: Are Your Funds Insured?

You may want to see also

Explore related products

![]()

Cost Comparison: Premiums & Benefits

When comparing the costs and benefits of Medigap and supplemental insurance, it's essential to understand that Medigap is a specific type of supplemental insurance designed to work alongside Original Medicare (Part A and Part B). While all Medigap plans are supplemental insurance, not all supplemental insurance plans are Medigap. Medigap plans are standardized by the federal government, meaning Plan A in one state offers the same benefits as Plan A in another, though premiums can vary widely between insurance companies. In contrast, supplemental insurance plans outside the Medigap framework can vary significantly in coverage and cost, often tailored to specific needs like dental, vision, or critical illness coverage.

Premiums are a key factor in cost comparison. Medigap premiums are typically higher than those for other supplemental insurance plans because they cover a broader range of out-of-pocket costs associated with Medicare, such as copayments, coinsurance, and deductibles. The average monthly premium for a Medigap policy can range from $100 to $300, depending on the plan type, your age, location, and the insurance provider. Supplemental insurance plans, on the other hand, may have lower premiums, often starting as low as $20 to $50 per month, but they usually cover fewer services and may come with higher out-of-pocket costs when you need care.

Benefits play a crucial role in determining the value of these plans. Medigap plans offer comprehensive benefits that fill the gaps in Original Medicare, such as covering Part A and Part B deductibles, coinsurance, and even emergency care abroad. For instance, Medigap Plan G, one of the most popular plans, covers all these areas except the Part B deductible. Supplemental insurance plans, however, may offer benefits that Medicare and Medigap do not cover, such as routine dental, vision, or hearing care, or cash benefits for hospital stays. These additional benefits can be valuable but are often limited in scope compared to the comprehensive coverage of Medigap.

Another important consideration is out-of-pocket costs. With Medigap, once you pay your monthly premium, you generally have minimal to no out-of-pocket costs for services covered by Medicare. Supplemental insurance plans may require you to pay deductibles, copayments, or coinsurance, which can add up quickly if you require extensive medical care. For example, a supplemental plan might offer a daily cash benefit for hospital stays, but you’ll still be responsible for other expenses not covered by Medicare or the supplemental plan.

Finally, flexibility and choice differ between Medigap and other supplemental insurance plans. Medigap plans are standardized, making it easier to compare plans across providers based on cost and reputation. Supplemental insurance plans offer more flexibility in terms of coverage options but require careful review to ensure they meet your specific needs. When comparing costs, consider not only the premiums but also the potential out-of-pocket expenses and the overall value of the benefits provided. Choosing between Medigap and other supplemental insurance ultimately depends on your healthcare needs, budget, and how much financial risk you’re willing to assume.

Is Teladoc Free with Insurance? Understanding Your Coverage Options

You may want to see also

Explore related products

![]()

Which Plan Suits Your Needs?

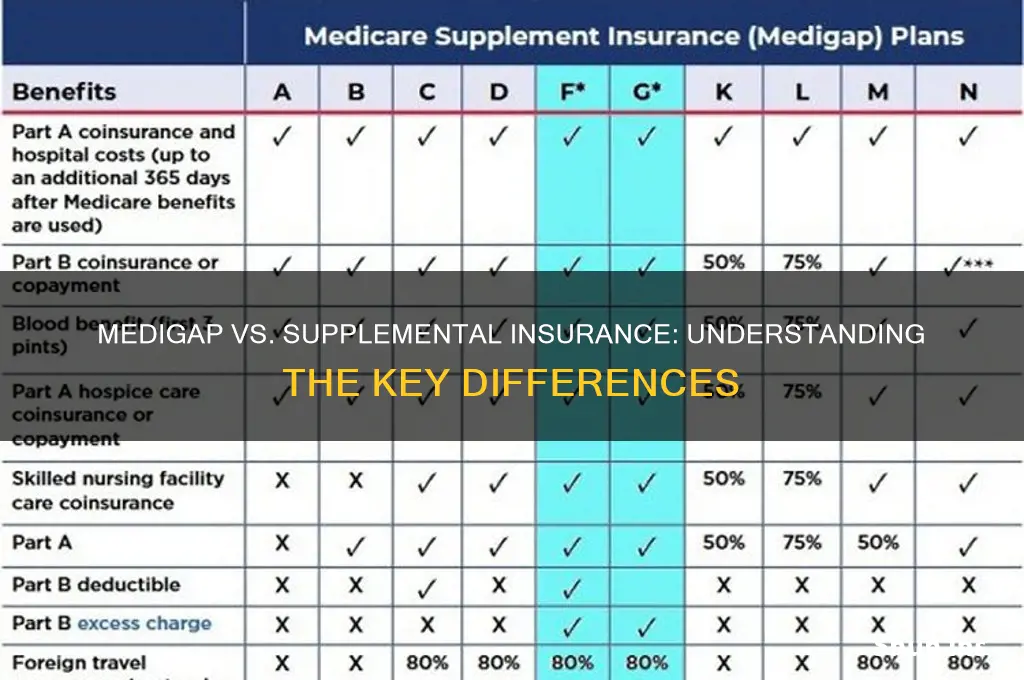

When deciding which plan suits your needs in the context of Medigap and supplemental insurance, it’s essential to understand that Medigap is indeed a type of supplemental insurance specifically designed to work alongside Original Medicare (Part A and Part B). Medigap policies, also known as Medicare Supplement Insurance, help cover out-of-pocket costs like copayments, deductibles, and coinsurance that Original Medicare doesn’t fully cover. The first step in choosing the right plan is to assess your healthcare needs and budget, as Medigap plans are standardized and labeled with letters (A, B, C, D, F, G, K, L, M, N) in most states, each offering different levels of coverage.

Plan G is currently one of the most popular Medigap options because it covers nearly all out-of-pocket costs, including the Part A deductible, hospice care coinsurance, and excess charges. It’s a strong choice if you want comprehensive coverage and predictability in healthcare expenses. Plan N is another cost-effective option, offering similar benefits to Plan G but with lower premiums. However, it requires you to pay small copayments for doctor visits and emergency room visits unless you’re admitted. If you’re comfortable with these minor out-of-pocket costs, Plan N can save you money in the long run.

For those on a tighter budget, Plan K and Plan L offer partial coverage of Medicare’s out-of-pocket costs, but they come with out-of-pocket limits to protect you from excessive expenses. These plans are less comprehensive but can be suitable if you don’t anticipate frequent medical needs. Plan F, while no longer available to new Medicare enrollees as of 2020, remains an option for those who enrolled in Medicare before that date. It’s the most comprehensive plan, covering all gaps in Original Medicare, including the Part B deductible.

When determining which plan suits your needs, consider factors like your health status, frequency of doctor visits, prescription drug needs, and travel habits. For example, if you travel often, a plan that covers emergency care abroad, like Plan C, D, F, G, M, or N, might be ideal. Additionally, if you have significant prescription drug needs, you may want to pair your Medigap plan with a standalone Medicare Part D prescription drug plan, as Medigap policies do not include prescription coverage.

Finally, compare premiums and insurers carefully, as the benefits of each Medigap plan are standardized, but the costs can vary widely between providers. Use tools like the Medicare Plan Finder to explore options in your area. Remember, the goal is to find a plan that balances coverage and cost, ensuring you’re protected without overspending. By evaluating your specific needs and understanding the differences between plans, you can confidently choose the Medigap policy that best suits your healthcare and financial situation.

Life Insurance Dividends: Taxable or Not?

You may want to see also

Frequently asked questions

Yes, Medigap is a type of supplemental insurance specifically designed to cover gaps in Original Medicare, such as copayments, deductibles, and coinsurance.

No, Medigap policies are only meant to supplement Original Medicare (Part A and Part B) and cannot be used with Medicare Advantage plans, employer-sponsored plans, or other types of health insurance.

Medigap plans are standardized and labeled with letters (A, B, C, D, etc.), but the coverage varies by plan. For example, Plan F offers the most comprehensive coverage, while Plan A covers the basics.

It depends on your needs. Medicare covers many healthcare costs, but Medigap can help pay for out-of-pocket expenses like deductibles and copayments, providing additional financial protection.

Yes, you can switch, but timing is crucial. The best time to enroll in Medigap is during your 6-month Medigap Open Enrollment Period, which starts when you turn 65 and enroll in Medicare Part B. Outside this period, you may face medical underwriting or higher premiums.