In California, mortgage protection insurance is not mandated by law, but it is often required by mortgage lenders as a condition of the loan. This insurance can provide peace of mind for homeowners and their families, as it covers the outstanding balance of the loan in the event of the borrower's death. Private mortgage insurance (PMI), on the other hand, is designed to protect the lender if the borrower defaults on the loan. While PMI is not always necessary, federal law mandates that it be cancelled automatically when the mortgage balance reaches 78% of the home's purchase price or the halfway point of the loan term. Additionally, homeowners insurance, which is not legally required in California, may also be mandated by lenders to protect their financial interests. This insurance covers perils such as fire damage and smoke damage but often excludes earthquakes and floods, which may need to be purchased separately.

| Characteristics | Values |

|---|---|

| Is home insurance mandatory in California? | No, it is not legally required. |

| Is home insurance a contractual requirement for mortgages in California? | Yes, mortgage lenders typically require borrowers to maintain some level of home insurance coverage. |

| Average cost of home insurance in California | $1,380 per year (as of 2023), $1,480 per year (as of November 2024) |

| Mortgage protection insurance in California | Mortgage protection insurance (MPI) is available in California. It covers the outstanding balance of the loan in the event of the borrower's death. |

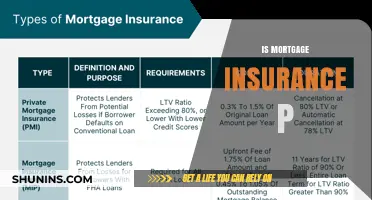

| Private mortgage insurance (PMI) in California | PMI is required for conventional loans. It protects the lender if the borrower defaults on the loan. |

| Mortgage insurance premium (MIP) in California | MIP is required for FHA loans from the Federal Housing Administration. It must be paid regardless of the down payment amount. |

Explore related products

![NMLS Study Guide: SAFE Mortgage Loan Originator Test Prep Secrets Book, Full-Length MLO Practice Exam, Detailed Answer Explanations: [2nd Edition]](https://m.media-amazon.com/images/I/71wuD4SQlSL._AC_UY218_.jpg)

What You'll Learn

- Home insurance isn't legally required in California, but mortgage lenders often demand it

- Mortgage protection insurance (MPI) safeguards your family from paying off a mortgage loan if you die

- Private mortgage insurance (PMI) protects lenders if you default on a loan

- Mortgage insurance premium (MIP) is paid for FHA loans

- Flood insurance may be mandatory for homeowners in flood-prone areas

![]()

Home insurance isn't legally required in California, but mortgage lenders often demand it

Home insurance isn't legally required in California. However, mortgage lenders often demand it as a contractual requirement for borrowers. This requirement is typically in place to protect the lender's financial interest in the property. So, while homeowners insurance may not be mandated by California law, it may be necessary to obtain it to comply with your mortgage agreement.

The average yearly cost of California homeowners insurance is $1,380, according to one source, while another source states the average to be $1,480 per year for $300,000 in dwelling coverage as of November 2024. The cost varies by location within the state, with some areas significantly higher than others. For example, homes in areas prone to natural disasters like wildfires or earthquakes will have higher premiums.

Mortgage protection insurance is a type of insurance that is commonly purchased in California. It ensures that if the breadwinner of a family passes away, the family can grieve without worrying about the cost of the house. The insurance covers the outstanding balance of the loan, and the death benefit is given directly to the creditor.

Private mortgage insurance (PMI) is another type of insurance that protects the lender if the borrower defaults on the loan. Federal law requires lenders to automatically cancel PMI when the loan balance drops to 78% of the home's purchase price or when the loan term reaches its halfway point, whichever comes first.

In summary, while home insurance isn't legally mandated in California, it is often required by mortgage lenders to protect their financial interests. The cost of insurance varies depending on location and the presence of natural disasters. Additionally, mortgage protection insurance and private mortgage insurance are common types of insurance that provide financial protection for homeowners and lenders in California.

Insuring Your New Home: When to Start

You may want to see also

Explore related products

![]()

Mortgage protection insurance (MPI) safeguards your family from paying off a mortgage loan if you die

In California, home insurance is not legally required. However, mortgage lenders often make it a contractual requirement for borrowers to maintain some level of home insurance coverage to protect their financial interest in the property. While this is not a legal mandate, it may be a necessity to comply with your mortgage agreement.

Mortgage protection insurance (MPI) is a type of insurance policy that safeguards your family from the burden of paying off a mortgage loan if you die or become disabled and unable to work. MPI is distinct from other types of insurance, such as private mortgage insurance (PMI) and mortgage insurance premiums (MIP), which protect the lender if you default on your loan. MPI provides peace of mind and security for you and your family, ensuring that your mortgage loan will be covered in the event of your death or disability.

MPI offers guaranteed acceptance, making it an attractive option for individuals who may have health issues or work in dangerous professions, as there are no medical exams or lab tests required for approval. It is important to note that MPI policies typically pay out directly to the lender to cover the remaining loan balance and interest charges, rather than providing a lump sum of cash to your family. This ensures that your loved ones won't have to worry about making mortgage payments during a difficult time.

The cost of MPI depends on factors such as the insurer, your age, the current balance of your mortgage, and the time left on your loan term. As you pay off your mortgage, the insurance payout decreases, but your premiums generally remain the same. MPI might be a good choice for those who cannot qualify for or afford traditional life insurance policies, as it can provide a sense of financial security for your family. However, it is important to consider the limitations of MPI, such as its lack of flexibility in covering only the mortgage loan, and compare it with other insurance options to determine the best fit for your needs.

Farmers Insurance and Mastiffs: A Policy Overview

You may want to see also

Explore related products

![]()

Private mortgage insurance (PMI) protects lenders if you default on a loan

In California, home insurance is not a legal requirement. However, mortgage lenders often require borrowers to maintain some level of home insurance coverage to protect their financial interests in the property. This is especially true in areas prone to natural disasters like wildfires, earthquakes, and floods.

Private mortgage insurance (PMI) is a type of insurance policy that protects the lender if a borrower defaults on a home loan. It is required when the borrower makes a down payment of less than 20% of the purchase price. In this case, the lender assumes additional risk by accepting a lower amount of upfront money, and PMI insures them against potential losses. The cost of PMI varies depending on the loan amount, down payment size, credit score, and other factors. It can be paid monthly along with the mortgage payment or as a one-time upfront premium. While PMI protects the lender, it can also help borrowers qualify for loans they might not otherwise be able to obtain.

It is important to note that PMI does not protect borrowers from foreclosure or negative impacts on their credit score if they fall behind on mortgage payments. Additionally, PMI is not permanent, and borrowers can request its cancellation once their mortgage balance reaches 80% of their home's value. Lenders are also required to cancel PMI when the mortgage balance drops to 78% of the original value or halfway through the loan term, whichever comes first.

While PMI is not tax-deductible on personal residences, it can provide peace of mind for lenders and help borrowers obtain financing for their homes. However, it is just one aspect of the overall cost of owning a home, and borrowers should carefully consider their options and consult with lenders to understand the specific requirements and costs associated with PMI.

Insurance Brokerage House: What's the Deal?

You may want to see also

Explore related products

![]()

Mortgage insurance premium (MIP) is paid for FHA loans

In California, home insurance is not legally required. However, mortgage lenders often make it a contractual requirement for borrowers to maintain some level of home insurance coverage to protect their financial interests in the property.

Mortgage insurance premium (MIP) is a type of mortgage insurance that is required for homeowners who take out loans backed by the Federal Housing Administration (FHA). FHA loans are considered higher-risk due to their low down payment and credit score requirements, so MIP protects lenders against borrower default. In most cases, you will pay MIP for the entire loan term.

MIP for an FHA loan is mandatory regardless of the amount you put down. It includes an upfront premium of 1.75% of the total loan amount, typically paid at closing, and annual premiums ranging from 0.15% to 0.75% of the loan amount. The annual premium depends on the loan amount, loan term, and down payment size.

FHA borrowers should be aware that MIP is an additional cost on top of their mortgage payments. While it may be a drawback, FHA loans offer generous benefits, especially for those with lower credit scores.

In California, there are other types of insurance to consider when obtaining a mortgage, such as earthquake and flood insurance, depending on the location of the property. Mortgage protection insurance is also available, providing peace of mind for your family by covering the outstanding balance of your loan in the event of your passing.

Farmers Insurance and LoJack Discounts: Unlocking the Benefits

You may want to see also

Explore related products

![]()

Flood insurance may be mandatory for homeowners in flood-prone areas

Home insurance is not legally required in California, and this includes flood insurance. However, flood insurance may be mandatory for some homeowners in flood-prone areas as a condition of their mortgage policies. This is because the lender has a financial interest in the property, and with a homeowners insurance policy in place, the lender is assured a payout in the event of a covered peril.

Standard homeowners' insurance does not cover flood damage. Flood insurance is a federal program administered by the Federal Emergency Management Agency (FEMA), which provides flood insurance protection to property owners, renters, and business owners in participating communities. California is known for its high risk of earthquakes and wildfires, and homes in areas prone to these natural disasters will have higher insurance premiums. Flooding is also a risk in some parts of the state, and while it may not be a legal requirement to have flood insurance, it could be a necessary addition to your homeowners insurance policy.

If you live in an area of California that is prone to flooding, it is important to assess your flood risk and determine if you need flood insurance. While it may not be a legal requirement, your mortgage lender may require you to have it to protect their financial interest in your property. You can purchase flood insurance through the National Flood Insurance Program (NFIP) or from private insurance companies through the Write Your Own (WYO) program.

It is worth noting that if you buy a house in a designated high-risk flood area and receive a mortgage loan from a federally regulated lender, the lender must, by law, require you to purchase and regularly renew flood insurance. This is to ensure that both you and the lender are protected in the event of a flood.

In addition to flood insurance, there are other types of insurance that may be mandatory for homeowners in California. For example, mortgage protection insurance (MPI) is a type of insurance that can protect your family from having to pay off a mortgage loan if you pass away. Private mortgage insurance (PMI) is another option, which protects the lender if you default on your loan. These types of insurance can provide peace of mind and financial protection for both homeowners and their families.

HPDE Insurance: Worth the Cost?

You may want to see also

Frequently asked questions

Mortgage protection insurance is not mandatory in California. However, mortgage lenders typically require you to carry homeowners insurance.

Mortgage protection insurance (MPI) is designed to pay off a mortgage in the case of the policyholder's death.

PMI protects the lender if the policyholder defaults on the loan.

The average cost of California homeowners insurance is $1,380 per year, although this varies by location within the state.