Mortgage insurance is an added expense for borrowers who make a down payment of less than 20% on a home. It protects the lender in the event that the borrower defaults on the loan. There are several types of mortgage insurance, including private mortgage insurance (PMI), borrower-paid mortgage insurance (BPMI), lender-paid mortgage insurance (LPMI), and single-premium mortgage insurance (SPMI). The cost of mortgage insurance can be paid monthly, annually, or in a lump sum, depending on the type of insurance and the terms of the loan. So, while mortgage insurance is not typically paid annually, there are certain circumstances where it may be.

| Characteristics | Values |

|---|---|

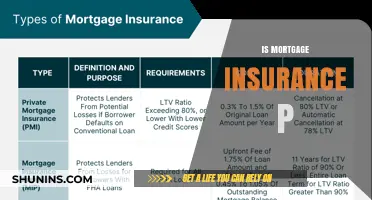

| Who does mortgage insurance protect? | The lender |

| Who pays for mortgage insurance? | The borrower |

| When is mortgage insurance paid? | Monthly, annually, upfront or in a lump sum |

| How much does mortgage insurance cost? | Between 0.5% and 1.5% of the original loan amount each year |

| Can mortgage insurance be cancelled? | Yes, under certain circumstances |

Explore related products

What You'll Learn

![]()

Private mortgage insurance (PMI)

PMI is arranged by the lender and provided by private insurance companies. It protects the lender in the event that the borrower stops making payments on their loan. PMI does not protect the borrower, and foreclosure may still occur if the borrower falls behind on payments.

PMI can be paid in a few different ways. Sometimes, you pay PMI with a one-time upfront premium at closing. This might be bundled with the rest of the loan amount. Sometimes, you pay with both upfront and monthly premiums. You can request to cancel PMI when your mortgage balance reaches 80% of your home's value, or when it reaches 78% of your home's original value, or when you are halfway through your loan term, whichever comes first.

You can avoid paying PMI by making a 20% down payment on a home.

Home Insurance: What Counts as Accidental Damage?

You may want to see also

Explore related products

![]()

Lender-paid mortgage insurance

LPMI is often considered when a borrower is unable to make a down payment of at least 20% on a home. In such cases, some form of mortgage insurance is usually required to protect the lender in case the borrower defaults on the loan. While LPMI does not increase monthly payments as much as PMI, it may cost more over the life of the loan. LPMI also cannot be cancelled like PMI can; it stays with the mortgage unless the borrower refinances or pays off the loan.

The decision to choose LPMI over PMI depends on several factors, including the borrower's credit score, down payment amount, and loan term. For example, if a borrower has excellent credit, they may pay a quarter-point more in interest for LPMI, whereas PMI would add a larger amount to their monthly payments. In this case, LPMI may be preferable in both the short and long term. However, if a borrower can get rid of PMI sooner than scheduled, such as by prepaying their mortgage or increasing their home's value, LPMI may become the more expensive option.

It is important to note that LPMI is not a free option, despite the lender technically paying for the insurance. Borrowers pay for LPMI indirectly through the higher interest rate on their loan, which may cost more in the long run. Therefore, it is recommended to compare several lenders to find the most suitable option for one's financial situation.

Insurance Code: Finding It in a Police Report

You may want to see also

Explore related products

![]()

Single-premium mortgage insurance

- Can afford a large payment at closing.

- Are expecting an inheritance or a large sum of money that they plan to use to pay off the loan in full.

- Believe they might refinance or pay off the loan within a few years of closing.

- Want to lower their monthly mortgage payments.

The advantages of single-premium mortgage insurance include:

- A lower monthly mortgage payment, which can make it easier to qualify for a mortgage.

- A lower debt-to-income ratio.

- Potential cost savings over the life of the loan.

However, single-premium mortgage insurance may not be suitable for everyone. For example, those who cannot afford a large upfront payment or those who plan to sell their home in a few years may find other options more favourable.

Indiana Farmers Insurance: Understanding the Reach and Service Network

You may want to see also

Explore related products

![]()

FHA mortgage insurance

Mortgage insurance is an added expense for borrowers who buy or refinance a home with a down payment under 20%. It protects the lender in the event that the borrower defaults on their payments. Typically, borrowers making a down payment of less than 20% of the purchase price of the home need to pay for mortgage insurance.

FHA loans are a good option for first-time homebuyers and those who have not saved much for their down payments. The FHA has a maximum loan amount that it will insure, known as the FHA lending limit. FHA mortgage insurance lowers the risk to the lender, allowing borrowers to qualify for loans they might not otherwise be able to get.

Usaa Private Mortgage Insurance: What's the Cost?

You may want to see also

Explore related products

![]()

USDA mortgage insurance

Mortgage insurance is usually paid monthly, though there are instances where a borrower can pay an upfront, lump-sum amount for the entire year. This type of insurance lowers the risk to the lender of making a loan, allowing borrowers to qualify for a loan that they might not otherwise be able to get. Typically, borrowers making a down payment of less than 20% of the purchase price of the home need to pay for mortgage insurance.

USDA loans are zero-down-payment loans for rural home buyers. They are a type of mortgage backed by the US Department of Agriculture, designed for people who want to live outside urban areas. USDA loans do not require private mortgage insurance (PMI), but they do have what is called a guarantee fee, which functions like mortgage insurance. This guarantee fee is paid in two parts: an upfront guarantee fee of 1% of the loan amount, and an annual fee of 0.35% of the average outstanding loan balance for the year, which is divided into monthly installments and included in the borrower's mortgage payment. The annual fee is paid for the life of the loan.

TurboTax ID Theft Insurance: Is It Worth the Cost?

You may want to see also

Frequently asked questions

Mortgage insurance protects the lender in the event that the borrower defaults on the loan. It also helps the borrower qualify for a loan they might not otherwise be able to get.

The cost of mortgage insurance depends on the type of loan and down payment size, the interest rate on the loan, and the borrower's credit score. Typically, the higher the credit score, the lower the insurance cost.

Mortgage insurance is usually paid monthly, along with the mortgage payment. However, some lenders allow borrowers to pay a larger upfront fee that covers part of the overall insurance costs, reducing the monthly payments.

Yes, in most cases, you can cancel your mortgage insurance once you've paid off more than 20% of the full loan amount.