The Affordable Care Act (ACA), enacted in 2010 and expanded in 2014, has been instrumental in expanding access to affordable, comprehensive health insurance coverage for Americans, particularly those with low and moderate incomes. However, recent developments, including the impending expiration of enhanced premium subsidies and the absence of tax credits in the House Republican tax bill, have raised concerns about the future of ACA insurance. These changes are expected to make ACA marketplace insurance more expensive, potentially leading to a decrease in enrollment and leaving millions without insurance.

| Characteristics | Values |

|---|---|

| Enacted | 2010 |

| Expanded | 2014 |

| Goal | Expanding access to affordable, comprehensive health insurance coverage |

| Impact | Historic reductions in the nation's uninsured rate |

| Reforms | Ban on denying coverage based on pre-existing conditions; guaranteed issue; modified community rating; mandatory coverage of preventive health services |

| Current Status | Partial repeal proposals exist |

| Future | Uncertain, potential increase in insurance costs |

Explore related products

$36.33 $54.99

What You'll Learn

![]()

The impact of undoing the ACA on healthcare

The Affordable Care Act (ACA) was enacted in 2010 and expanded in 2014 to increase access to affordable, comprehensive health insurance coverage, especially for low- and middle-income Americans. The ACA has been largely successful in achieving historic reductions in the uninsured rate in the US. However, with the fate of the ACA hanging in the balance after the 2024 elections, it is important to understand the impact of undoing the ACA on healthcare.

Firstly, undoing the ACA would lead to a sharp rise in insurance premiums. The ACA introduced premium subsidies and tax credits, which made health insurance more affordable for millions of Americans. Without these benefits, insurance premiums will become significantly more expensive, affecting almost everyone who buys their own health insurance. This will likely cause healthy people to drop their coverage, destabilizing the private insurance market and leading to even higher costs.

Secondly, protections for people with pre-existing conditions will be weakened or eliminated. The ACA introduced reforms that banned insurers from denying coverage based on health status and required them to accept applicants regardless of pre-existing conditions. Without these protections, insurers will be allowed to charge higher rates or deny coverage outright to people with pre-existing health conditions. This could affect up to 52 million people with pre-existing conditions, who may struggle to access affordable healthcare.

Thirdly, community health centers serving low-income, uninsured, and rural populations will be severely impacted. The ACA expanded Medicaid, which allowed millions of previously uninsured people to gain coverage. However, if Medicaid expansion is dismantled, community health centers will face financial shocks and reduced access to vital comprehensive primary care, behavioral health, dental, and case management services. This will disproportionately affect communities of color and low-income communities, leading to increased healthcare disparities.

Lastly, undoing the ACA would have economic repercussions, including job losses and reduced economic output. The ACA established the Prevention and Public Health Fund, which provided federal funding for prevention initiatives and community health improvements. Repealing the ACA could cost an estimated 2.6 million healthcare jobs, and states' gross products could decrease by almost $1.5 trillion.

In conclusion, undoing the ACA would have far-reaching consequences on healthcare in the US. It would lead to increased insurance costs, reduced protections for people with pre-existing conditions, financial strain on community health centers, and job losses in the healthcare sector. These impacts would disproportionately affect low-income individuals, communities of color, and those with pre-existing health conditions, exacerbating existing healthcare inequities.

Unpaid Insurance: Debt Collection and Your Rights

You may want to see also

Explore related products

$64.95 $64.95

![]()

ACA's enhanced premium credits

The Affordable Care Act (ACA) has been successful in expanding access to affordable, comprehensive health insurance coverage, particularly for Americans with low and moderate incomes. The ACA's enhanced premium credits help make health insurance policies more affordable.

The enhanced premium tax credits (PTCs) were introduced as part of the American Rescue Plan Act of 2020 to ensure that Americans had access to affordable health insurance during the pandemic. These enhanced tax credits were extended through 2025 under the Inflation Reduction Act. The tax credits reduce the insurance premiums that enrollees pay based on their projected income for the year. The credits are paid directly to health insurers, who then lower the monthly amounts they charge.

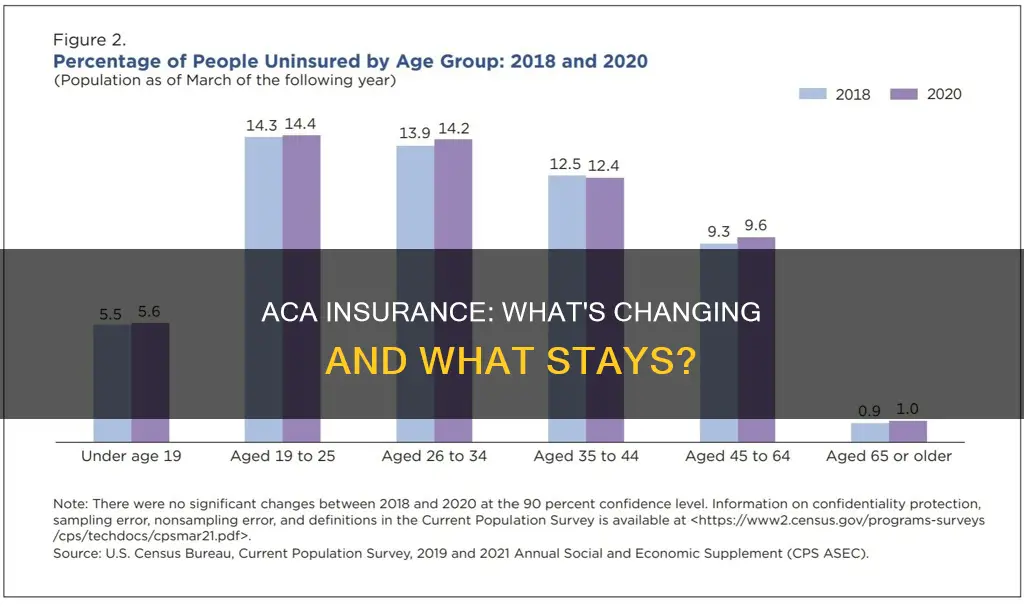

The enhanced subsidies have increased enrollment in ACA marketplace plans and reduced the number of uninsured people. They have helped increase enrollment in the marketplaces from 12 million in 2021 to a record 24.2 million in 2025. Ninety-three percent of marketplace enrollees rely on the premium tax credits to make their insurance premiums affordable.

The enhanced subsidies are set to expire at the end of 2025, and if they are not extended, marketplace enrollment is projected to drop from 22.8 million in 2025 to 18.9 million in 2026. The Congressional Budget Office estimates that 2.2 million consumers will lose their health insurance in 2026, with an average of 3.8 million people losing their coverage each year from 2026 to 2034.

The enhanced premium credits have provided additional subsidies to people who are already eligible for regular tax credits and have extended tax credits to people with higher incomes. They have eliminated the "subsidy cliff," which rendered people with incomes above the poverty level ineligible for subsidies.

The ACA's enhanced premium credits have helped make health insurance more affordable and accessible for millions of Americans. With the credits set to expire at the end of 2025, it remains to be seen whether Congress will take action to extend them and continue providing financial assistance to those in need of affordable health coverage.

IRS Targets Insurance Penalty: What You Need to Know

You may want to see also

Explore related products

![]()

ACA's Health Insurance Marketplace

The Affordable Care Act (ACA) was enacted in 2010 and expanded in 2014 with the primary goal of expanding access to affordable, comprehensive health insurance coverage, particularly for Americans with low and moderate incomes. The ACA has been largely successful in achieving historic reductions in the nation's uninsured rate.

The ACA's Health Insurance Marketplace offers a wide range of plans to choose from, providing coverage for medical, dental, and vision care. The ACA introduced several reforms to the private insurance market, including banning insurers from denying coverage to people with pre-existing health conditions, guaranteeing issue regardless of age, health status, or gender, and requiring plans to cover important preventive health services like cancer screenings at no additional cost to consumers.

To be eligible to enroll in health coverage through the ACA Marketplace, individuals must be U.S. citizens or nationals or be lawfully present. There is no income limit, and the ACA provides special patient protection, ensuring that insurers cannot refuse coverage based on sex or pre-existing conditions.

However, there have been concerns about the potential impact of undoing or modifying the ACA. The enhanced premium credits under the ACA, which help make health insurance policies more affordable, are set to expire at the end of 2025. The absence of an extension could lead to a significant increase in premiums and a reduction in enrollment, affecting millions of consumers.

The House Republican tax bill, for instance, did not include an extension of the ACA credits, leading to concerns about the affordability of marketplace health insurance. Experts anticipate that the lapse of credits and proposed changes could result in higher costs for most individuals purchasing their own health insurance and potentially leave millions uninsured.

Insurance Rates: The Benefits of Being 25 and Under

You may want to see also

Explore related products

![]()

ACA reforms to the private insurance market

The Affordable Care Act (ACA) has introduced a series of reforms to the private insurance market, with the goal of expanding access to affordable, comprehensive health insurance coverage. The ACA was enacted in 2010 and expanded in 2014, and has been largely successful in its primary goal, particularly among Americans with low and moderate incomes.

One of the key reforms introduced by the ACA is the ban on insurers denying coverage to people with pre-existing health conditions. This includes employer-based insurance and insurance purchased through the newly regulated nongroup insurance markets. The ACA also introduced guaranteed issue, meaning that health plans must accept applicants regardless of age, health status, gender, and other characteristics.

Another important reform is the modified community rating, which prevents insurers from varying rates based on health status. This is coupled with the requirement that plans cover important preventive health services, such as cancer screenings, at no cost to consumers.

The ACA has also made changes to the way private insurance is sold and operated, particularly for nongroup health insurance and fully insured plans sold to small employers. These changes have enhanced the accessibility, affordability, and adequacy of these markets.

The ACA has also provided income-related financial assistance for the purchase of comprehensive nongroup insurance, and created Marketplaces to provide consumers with information on their plan options and help them understand their choices. These Marketplaces have seen increased insurer participation, giving consumers more options.

While the ACA has been successful in expanding access to affordable health insurance, there have been ongoing attempts by Republican politicians to weaken or repeal the law. These efforts have included lawsuits and creating uncertainty that has adversely impacted enrollment and insurer participation while increasing premiums. The outcome of the 2024 presidential and congressional elections may have a significant impact on the future of the ACA.

Ohio: Uninsured Motorist Insurance — Mandatory or Optional?

You may want to see also

Explore related products

![]()

ACA's expansion of Medicaid

The Affordable Care Act (ACA) has been successful in expanding access to affordable, comprehensive health insurance coverage, particularly for Americans with low and moderate incomes. The ACA's expansion of Medicaid has been a key part of this success.

Medicaid is a public health insurance program, and under the ACA, more people have been able to enroll in it. The ACA has allowed this by expanding income eligibility standards, permitting states to offer coverage to adults with incomes up to 138% of the poverty level (about $20,780 annually for an individual or $35,630 for a family of three). This figure is $21,597 for an individual in 2025.

The ACA has also made income-based subsidies available for the purchase of non-group or individual market coverage through new insurance exchanges called marketplaces. These subsidies have helped make health insurance policies more affordable. For example, eligible applicants can use the credit to lower insurance premium costs upfront or claim the tax break when filing their tax returns. Lower-income people can pay nothing upfront, while higher-income people pay no more than 8.5% of their income on their premium.

The federal government has also played a significant role in funding the expansion of Medicaid under the ACA. From 2014 to 2016, the federal government paid 100% of the cost of expansion coverage, with this share gradually dropping to 90% for 2020 and each year thereafter. This means that the federal government currently pays 90% of states' expansion costs on a permanent basis, while states cover the remaining 10%. This has resulted in dramatic reductions in uninsured rates, with 40 states plus Washington, D.C., having adopted the expansion as of 2024.

However, there are concerns that proposed cuts to the ACA's Medicaid expansion could lead to significant coverage losses. One proposal is to eliminate the 90% federal matching rate and instead apply a state's regular matching rate, which could be as low as 50%. Such a cut would require states to increase their spending significantly to sustain the expansion or risk terminating their expansions, resulting in millions of low-income Americans losing their health coverage.

Cell Phone Insurance: Worth the Cost?

You may want to see also

Frequently asked questions

ACA stands for the Affordable Care Act, which was enacted in 2010 and expanded in 2014. The ACA's primary goal is to expand access to affordable, comprehensive health insurance coverage, particularly among Americans with low and moderate incomes.

The ACA has introduced a number of reforms to the private insurance market, including:

- A ban on insurers denying coverage based on pre-existing health conditions.

- Guaranteed issue, meaning health plans must accept applicants regardless of age, health status, gender, and other characteristics.

- Modified community rating, meaning insurers cannot vary rates based on health status.

- Important preventive health services, like cancer screenings, must be covered at no cost to consumers.

The ACA is currently still in place, however, there have been recent changes to the Act that may affect consumers' finances. The "One Big Beautiful Bill Act" passed by House Republicans does not include an extension of the insurance premium tax credits under the ACA, which are set to expire at the end of 2025. This will likely result in increased costs for those buying their own health insurance. It is estimated that 2.2 million consumers will lose their health insurance in 2026 if the enhanced premium subsidies are not extended.