The question Is my prescription insurance just my health insurance? is a common one among individuals navigating the complexities of healthcare coverage. While both prescription insurance and health insurance are components of overall medical coverage, they serve distinct purposes and often come with different terms and conditions. Prescription insurance specifically covers the cost of medications prescribed by a healthcare provider, whereas health insurance encompasses a broader range of medical services, including doctor visits, hospital stays, and preventive care. Understanding the differences between these two types of insurance is crucial for making informed decisions about your healthcare and managing your medical expenses effectively.

Explore related products

What You'll Learn

- Understanding Prescription Insurance: Covers medication costs, may be part of or separate from health insurance

- Types of Prescription Insurance Plans: Includes employer-sponsored, individual, and government-funded options like Medicare Part D

- How Prescription Insurance Works: Deductibles, copays, and coverage tiers explained; how it interacts with health insurance?

- Common Prescription Insurance Providers: Overview of major companies offering prescription insurance, such as CVS Caremark and Express Scripts

- Tips for Choosing Prescription Insurance: Factors to consider, such as formulary, cost, and coverage, to select the best plan

![]()

Understanding Prescription Insurance: Covers medication costs, may be part of or separate from health insurance

Prescription insurance is a type of coverage that specifically addresses the cost of medications. It can be a standalone policy or integrated into a broader health insurance plan. The primary purpose of prescription insurance is to make medications more affordable for individuals, especially those with chronic conditions requiring long-term medication use.

One common misconception is that prescription insurance is the same as health insurance. While both types of insurance can cover medical expenses, prescription insurance focuses exclusively on medication costs. Health insurance, on the other hand, typically covers a wider range of medical services, including doctor visits, hospital stays, and diagnostic tests.

Prescription insurance plans can vary significantly in terms of coverage and cost. Some plans may cover only generic medications, while others may include brand-name drugs as well. The level of coverage can also depend on the specific medications needed and the individual's medical history.

When considering prescription insurance, it's important to understand the different types of plans available. Some common options include:

- Preferred Provider Organization (PPO): This type of plan allows individuals to choose their own pharmacy and doctor, but may require a copay or coinsurance for medications.

- Health Maintenance Organization (HMO): This plan typically requires individuals to use a specific network of pharmacies and doctors, but may offer lower out-of-pocket costs.

- Exclusive Provider Organization (EPO): Similar to an HMO, this plan requires the use of a specific network, but may offer more flexibility in terms of medication coverage.

To determine if prescription insurance is right for you, consider your medication needs and budget. If you take multiple medications or have high out-of-pocket costs, prescription insurance may be a valuable addition to your health coverage. However, if you rarely need medications or have a low deductible, you may not need separate prescription insurance.

In conclusion, prescription insurance is a specialized type of coverage designed to help individuals manage the cost of medications. While it can be a valuable tool for many, it's important to understand the different types of plans available and how they fit into your overall health insurance strategy.

Kroger Personal Accident Insurance: What You Need to Know

You may want to see also

Explore related products

![]()

Types of Prescription Insurance Plans: Includes employer-sponsored, individual, and government-funded options like Medicare Part D

Employer-sponsored prescription insurance plans are a common benefit offered by many companies as part of their overall health insurance packages. These plans typically cover a portion of the cost of prescription medications, with the employee responsible for a copay or coinsurance amount. The specifics of coverage, including the formulary (list of covered medications) and cost-sharing structure, can vary widely between employers and insurance providers.

Individual prescription insurance plans are purchased directly by consumers from private insurance companies. These plans are designed to cover prescription medication costs for individuals who do not have access to employer-sponsored coverage or who prefer to purchase their own insurance. Individual plans can offer varying levels of coverage, and consumers should carefully compare options to find a plan that meets their specific medication needs and budget.

Government-funded prescription insurance options, such as Medicare Part D, are available to certain populations, including seniors and individuals with disabilities. Medicare Part D is a prescription drug benefit program that subsidizes the cost of prescription medications for Medicare beneficiaries. These plans are offered by private insurance companies approved by Medicare, and beneficiaries can choose from a variety of plans based on their medication needs and preferred pharmacy networks.

When considering prescription insurance options, it's important to understand the differences between these types of plans and how they may impact your overall health insurance coverage. Employer-sponsored plans are often the most convenient option for those with access to them, as they are typically integrated with the employee's health insurance plan. Individual plans offer more flexibility but may come with higher premiums and out-of-pocket costs. Government-funded options like Medicare Part D provide essential coverage for vulnerable populations but have specific eligibility requirements and enrollment periods.

To make the most informed decision about prescription insurance, individuals should carefully review the details of each plan type, including coverage levels, costs, and any restrictions or limitations. Consulting with an insurance professional or utilizing online resources can help consumers navigate the complexities of prescription insurance and find the best option for their unique needs.

Medical Malpractice Insurance: Clinic-Specific or Universal Coverage?

You may want to see also

Explore related products

$12.99 $12.99

![]()

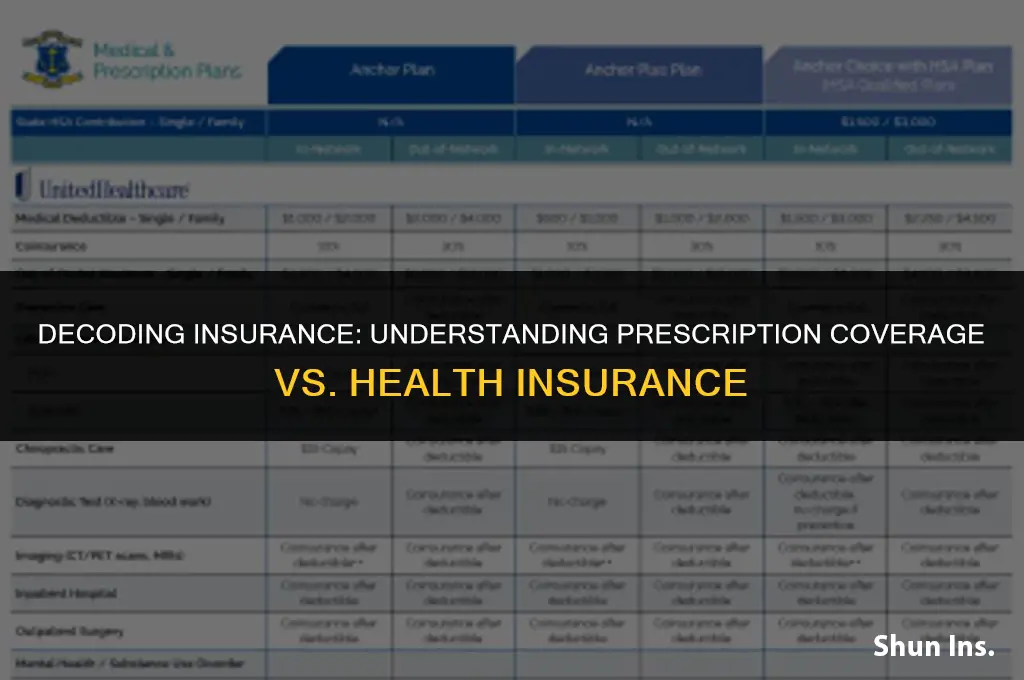

How Prescription Insurance Works: Deductibles, copays, and coverage tiers explained; how it interacts with health insurance

Prescription insurance is a specific type of coverage that is often part of a broader health insurance plan. It is designed to help cover the cost of prescription medications, which can be a significant expense for many individuals. While prescription insurance is typically included in health insurance plans, it is not always the case, and some people may opt for standalone prescription drug plans.

One of the key aspects of prescription insurance is understanding the different coverage tiers. These tiers are usually categorized as generic, brand-name, and specialty drugs. Each tier has a different level of coverage and cost-sharing. For example, generic drugs are usually the least expensive and have the lowest copay, while specialty drugs are the most expensive and may require a higher copay or coinsurance.

Deductibles and copays are also important components of prescription insurance. A deductible is the amount you must pay out-of-pocket before your insurance coverage begins. Copays are fixed amounts you pay for each prescription, regardless of the drug's cost. Coinsurance, on the other hand, is a percentage of the drug's cost that you are responsible for after meeting your deductible.

Prescription insurance interacts with health insurance in several ways. For instance, if you have a health insurance plan with a high deductible, you may need to pay more out-of-pocket for your prescriptions until you meet the deductible. Additionally, some health insurance plans may have a separate prescription drug deductible. It is also important to note that prescription insurance may not cover all medications, and some drugs may be excluded from coverage.

When choosing a health insurance plan, it is crucial to consider the prescription drug coverage options. If you take multiple medications or have a chronic condition that requires expensive treatments, you may want to opt for a plan with more comprehensive prescription drug coverage. On the other hand, if you rarely need prescriptions, you may be able to save money by choosing a plan with less robust coverage.

In conclusion, prescription insurance is a vital component of health insurance that helps cover the cost of medications. Understanding the different coverage tiers, deductibles, copays, and how prescription insurance interacts with health insurance can help you make informed decisions when choosing a plan that best suits your needs.

Traveling Abroad? What You Need to Know About Health Insurance Coverage

You may want to see also

Explore related products

![]()

Common Prescription Insurance Providers: Overview of major companies offering prescription insurance, such as CVS Caremark and Express Scripts

CVS Caremark and Express Scripts are two of the largest prescription insurance providers in the United States. They manage prescription drug benefits for millions of Americans, offering a range of services from pharmacy benefit management to specialty pharmacy care. CVS Caremark, for instance, operates one of the largest retail pharmacy chains in the country and has a significant presence in the mail-order pharmacy market through its Caremark Pharmacy Services segment. Express Scripts, on the other hand, focuses primarily on pharmacy benefit management and has a strong reputation for its cost-containment strategies and innovative technology solutions.

Both companies play a critical role in the healthcare system by negotiating prices with drug manufacturers, managing formularies, and providing patient education and support. They also offer tools and resources to help members manage their medications and make informed decisions about their healthcare. For example, CVS Caremark's MinuteClinics provide convenient access to healthcare services, while Express Scripts' mobile app allows members to easily manage their prescriptions and track their medication adherence.

When it comes to choosing a prescription insurance provider, it's essential to consider factors such as the breadth of the provider's network, the range of services offered, and the provider's reputation for customer service and innovation. CVS Caremark and Express Scripts are just two examples of the many companies that offer prescription insurance, and each has its own unique strengths and weaknesses. By understanding the different options available, individuals can make more informed decisions about their healthcare coverage and ensure they have access to the medications and services they need.

In conclusion, CVS Caremark and Express Scripts are major players in the prescription insurance market, offering a range of services and tools to help members manage their healthcare. When choosing a prescription insurance provider, it's important to consider factors such as network breadth, service offerings, and customer reputation to ensure you have access to the best possible care.

Can Both Spouses Have Health Insurance? Exploring Joint Coverage Options

You may want to see also

Explore related products

![]()

Tips for Choosing Prescription Insurance: Factors to consider, such as formulary, cost, and coverage, to select the best plan

When selecting prescription insurance, it's crucial to understand the formulary, which is the list of medications covered by the plan. Not all medications are covered equally, and some may not be covered at all. Review the formulary to ensure that the medications you need are included and that they are categorized in a way that minimizes your out-of-pocket costs. Pay attention to the tiers or levels of coverage, as medications in lower tiers typically have lower copays or coinsurance.

Cost is another significant factor to consider. While premiums are important, they are not the only cost to evaluate. Deductibles, copays, coinsurance, and out-of-pocket maximums can all impact your overall expenses. Compare the total costs of different plans by considering both the premium and the expected out-of-pocket costs based on your medication needs. Additionally, some plans may offer cost-saving features such as mail-order pharmacies or discounts for generic medications, which can help reduce your expenses.

Coverage is not just about the medications included but also about the services and support provided by the insurance company. Look for plans that offer additional resources such as medication therapy management, which can help you better understand and manage your medications. Some plans may also provide access to telehealth services or have partnerships with pharmacies that offer convenient refill options.

When evaluating prescription insurance plans, it's essential to consider your specific needs and circumstances. For example, if you have a chronic condition that requires ongoing medication, you may want to prioritize plans with lower copays for long-term prescriptions. On the other hand, if you only need occasional medications, a plan with a lower premium and higher copays might be more cost-effective.

Finally, don't overlook the importance of customer service and ease of use. A plan with excellent coverage and low costs may not be worth it if the insurance company is difficult to work with or if the claims process is overly complicated. Look for plans with a user-friendly website, mobile app, or customer service representatives who are easy to reach and helpful.

By carefully considering these factors, you can select a prescription insurance plan that best meets your needs and helps you manage your medication costs effectively.

Blue Cross Blue Shield: Medicare Supplement Insurance?

You may want to see also

Frequently asked questions

Prescription insurance is a type of health insurance that specifically covers the cost of prescription medications. While it is a component of health insurance, it is not the same as your overall health insurance plan, which typically includes coverage for doctor visits, hospital stays, and other medical services.

It depends on your health insurance plan. Some health insurance plans include prescription coverage as part of their benefits, while others may require you to purchase a separate prescription insurance plan. Review your plan details to determine if prescription coverage is included or if you need to enroll in a separate plan.

Prescription insurance works by covering a portion of the cost of your prescription medications. You typically pay a copay or coinsurance for each prescription, and the insurance company pays the remaining amount. The specifics of how your prescription insurance works will depend on your plan, including the medications covered, the cost-sharing structure, and any deductibles or limits.

Most prescription insurance plans have a network of participating pharmacies where you can use your insurance. Using a pharmacy within your plan's network will typically result in lower out-of-pocket costs. However, some plans may allow you to use your insurance at non-network pharmacies, although you may pay more for your prescriptions. Check your plan details to determine which pharmacies are in-network and how using out-of-network pharmacies may affect your coverage.