The question of whether insurance in America is inherently bad is a complex and multifaceted issue that sparks widespread debate. With skyrocketing premiums, high deductibles, and a fragmented system that often leaves individuals underinsured or uninsured, many argue that the U.S. insurance model prioritizes corporate profits over public health and financial security. Critics point to the lack of universal coverage, the administrative inefficiencies, and the disparities in access to care as evidence of systemic flaws. However, others contend that the American insurance system offers unparalleled choice and innovation, with private plans providing comprehensive benefits to those who can afford them. Ultimately, the perception of whether insurance in America is bad depends on individual experiences, socioeconomic status, and the broader context of healthcare policy and affordability.

Explore related products

What You'll Learn

![]()

High Premiums, Low Coverage

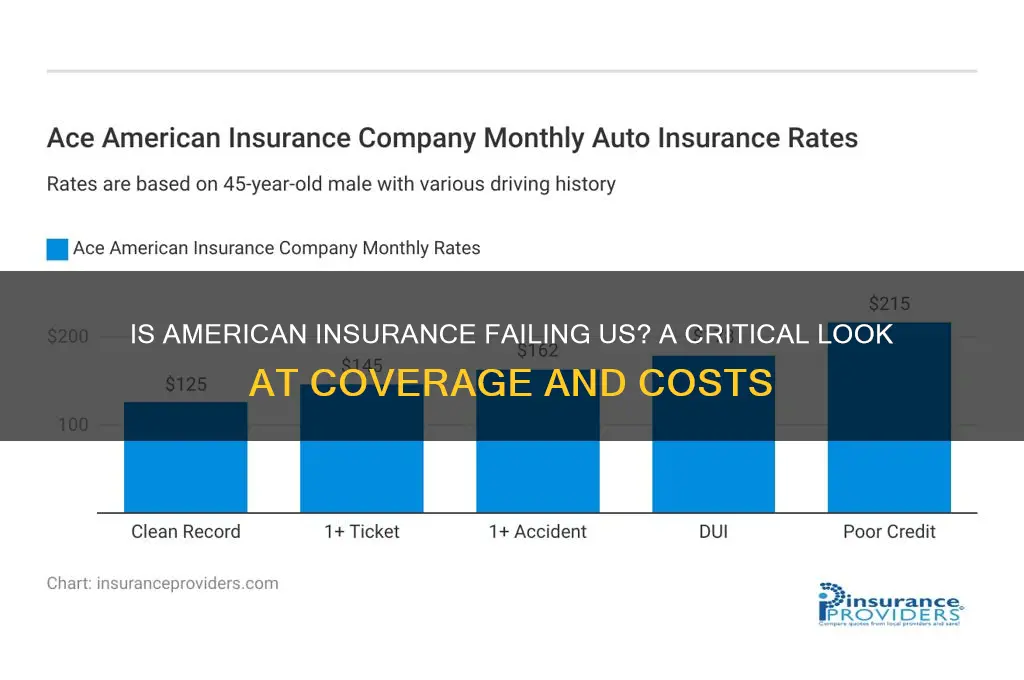

Americans pay more for health insurance than citizens of any other developed nation, yet often receive less in return. A 2022 study by the Commonwealth Fund found that the average annual premium for employer-sponsored family coverage in the U.S. exceeded $22,000, with employees shouldering nearly $6,000 of that cost. Compare this to countries like Germany or Canada, where government-funded systems provide comprehensive coverage at a fraction of the price. Despite these staggering costs, many U.S. plans come with high deductibles—often $1,000 or more—meaning individuals must pay thousands out-of-pocket before insurance even kicks in. This paradox of high premiums and low coverage leaves millions financially vulnerable, even when they’re "insured."

Consider the case of a 45-year-old teacher in Texas who pays $400 monthly for a mid-tier plan. After a sudden appendectomy, she’s hit with a $3,000 deductible and 20% coinsurance on the remaining $15,000 bill. Her total out-of-pocket cost? Over $6,000—more than her annual mortgage payment. Stories like hers are common, illustrating how high premiums don’t guarantee financial protection. Even worse, nearly 30% of insured Americans are underinsured, meaning their coverage is so limited they avoid care due to cost. This system fails its core purpose: to shield individuals from catastrophic expenses.

To navigate this minefield, consumers must scrutinize plan details beyond the premium. First, calculate your expected annual healthcare costs, including prescriptions and specialist visits. Compare this to the plan’s deductible, copays, and out-of-pocket maximum. For example, if you take a $100/month medication, a plan with low premiums but high drug copays may cost more in the long run. Second, leverage Health Savings Accounts (HSAs) if your plan is high-deductible; contributions are tax-deductible and grow tax-free. Finally, don’t overlook preventive care—most plans cover it fully, reducing future costs. These steps won’t fix the system, but they can mitigate its flaws.

The root of this issue lies in the fragmented, profit-driven nature of U.S. insurance. Unlike single-payer systems, where governments negotiate prices, American insurers operate in a patchwork market with little oversight. This allows providers to charge exorbitant rates for services, which insurers pass on to consumers. For instance, an MRI costs $1,400 in the U.S. but just $300 in France. Until systemic reforms address these price disparities and prioritize coverage over profit, Americans will continue paying more for less. The takeaway? High premiums don’t equate to high value—and consumers must advocate fiercely for their own financial health.

Does Umbrella Insurance Make Sense? Pros, Cons, and Coverage Explained

You may want to see also

Explore related products

![]()

Denied Claims and Loopholes

One of the most frustrating experiences for policyholders is having an insurance claim denied. Denied claims often stem from vague policy language, exclusions buried in fine print, or disputes over medical necessity. For instance, a health insurance provider might reject a claim for a prescribed medication, citing it as "experimental" despite FDA approval. Similarly, homeowners’ insurance policies frequently exclude damage from natural disasters like floods or earthquakes, leaving policyholders financially vulnerable. Understanding these loopholes is the first step in navigating the complex landscape of insurance claims.

To avoid falling victim to denied claims, policyholders must scrutinize their policies for ambiguous terms and hidden exclusions. For example, some life insurance policies exclude payouts for deaths resulting from "high-risk activities," a term that can be broadly interpreted to include anything from skydiving to certain sports. Similarly, auto insurance policies may deny claims if the driver was using the vehicle for business purposes, even if the policyholder was unaware of this restriction. A proactive approach involves reviewing policies annually, asking clarifying questions, and documenting all communications with insurers.

When a claim is denied, policyholders should not accept the decision at face value. Instead, they should request a detailed explanation in writing, outlining the specific policy provision that led to the denial. For medical claims, obtaining a letter of medical necessity from a healthcare provider can strengthen an appeal. In property claims, hiring an independent adjuster to assess damages can provide a second opinion that counters the insurer’s findings. Persistence is key; many denied claims are overturned during the appeals process, especially when policyholders present compelling evidence.

Comparing insurance policies across providers can also reveal disparities in coverage and potential loopholes. For example, some health insurance plans cap coverage for mental health treatment at a lower rate than physical health, while others exclude pre-existing conditions for the first year of coverage. Homeowners’ insurance policies may offer replacement cost coverage for personal belongings, but only if the policyholder maintains an inventory of their possessions. By comparing these details, consumers can choose policies that minimize the risk of denied claims and maximize protection.

Ultimately, the prevalence of denied claims and loopholes underscores the need for regulatory reform and greater transparency in the insurance industry. Policymakers must mandate clearer policy language and stricter oversight to prevent insurers from exploiting technicalities. Until then, policyholders must remain vigilant, educating themselves on their rights and advocating for fair treatment. By understanding the intricacies of denied claims and loopholes, individuals can better protect themselves from financial hardship and ensure their insurance serves its intended purpose.

Depreciating Prepaid Insurance: A Step-by-Step Accounting Guide for Businesses

You may want to see also

Explore related products

$17.75

![]()

Profit Over Patient Care

The U.S. healthcare system spends nearly twice as much per capita as other high-income nations, yet ranks poorly in health outcomes. This disparity isn’t accidental—it’s systemic. Insurance companies, as key players, often prioritize profit margins over patient well-being, creating a cycle where administrative costs balloon while coverage shrinks. For instance, a 2020 study found that 30% of U.S. healthcare spending goes toward billing and insurance-related costs, compared to 3-5% in countries with single-payer systems. This inefficiency isn’t just a financial burden; it’s a moral one, as patients are forced to navigate a labyrinth of denials, delays, and out-of-pocket expenses.

Consider the case of insulin pricing. In the U.S., a vial of insulin can cost upwards of $300, despite production costs estimated at less than $10. For the 7.4 million Americans reliant on insulin, this profiteering is a matter of life and death. Insurance companies often negotiate high list prices with pharmaceutical firms, then pass the cost onto patients through high deductibles and copays. Meanwhile, in Canada, the same vial costs around $30. This isn’t a failure of the market—it’s a feature of a system designed to maximize revenue, not health.

To break this cycle, patients must become advocates for their own care. Start by scrutinizing your insurance plan’s drug formulary—the list of covered medications. If a critical drug is excluded or priced prohibitively, appeal the decision using the insurer’s internal process. Document all communication, and if denied, escalate to your state’s insurance commissioner. For those on insulin, consider switching to older, cheaper formulations like NPH or Regular insulin, which are just as effective for many patients. Always consult your doctor before making changes, but don’t let insurers dictate your treatment options.

The profit-driven model also harms preventive care, a cornerstone of long-term health. Insurers often limit coverage for screenings, mental health services, and chronic disease management, arguing these measures don’t yield immediate returns. Yet, untreated conditions like hypertension or depression can lead to costly complications. For example, managing hypertension with medications like lisinopril (which costs pennies per pill) can prevent strokes and heart attacks, saving thousands in emergency care. Patients should push for comprehensive coverage by joining advocacy groups like the National Alliance on Mental Illness or the American Diabetes Association, which lobby for policy changes and provide resources to challenge insurer decisions.

Ultimately, the "Profit Over Patient Care" paradigm won’t change without systemic reform. Until then, patients must navigate the system with vigilance and persistence. Use tools like Healthcare.gov to compare plans, and don’t assume higher premiums mean better coverage. Look for plans with low out-of-pocket maximums and robust preventive care benefits. When denied coverage, appeal aggressively—insurers often reverse decisions when faced with informed, persistent consumers. The system may be broken, but individual actions can mitigate its worst excesses.

Filing a Complaint Against Liberty Mutual Insurance: A Step-by-Step Guide

You may want to see also

Explore related products

$9.99 $14.49

![]()

Lack of Universal Healthcare

The United States stands alone among developed nations in lacking a universal healthcare system, leaving millions uninsured or underinsured. This gap isn’t just a policy quirk—it’s a systemic failure with tangible consequences. For instance, a 2022 Commonwealth Fund study found that 11% of working-age adults in the U.S. were uninsured, compared to less than 1% in countries like Germany and the UK. Without universal coverage, access to care becomes a privilege tied to employment or income, not a guaranteed right. This disparity doesn’t just affect the poor; middle-class families often face crippling out-of-pocket costs, even with insurance, due to high deductibles and copays.

Consider the practical implications: a 45-year-old with diabetes in the U.S. might spend $5,000 annually on insulin, while their Canadian counterpart pays a fraction of that under a single-payer system. This isn’t merely about cost—it’s about health outcomes. Uninsured individuals are less likely to seek preventive care, leading to untreated conditions that worsen over time. For example, a study in *Health Affairs* found that uninsured adults are 25% more likely to die prematurely than those with coverage. Universal healthcare isn’t just a moral imperative; it’s a proven strategy for reducing mortality and improving public health.

Critics argue that universal healthcare would strain the economy, but evidence suggests otherwise. Countries with single-payer systems, like Norway and Sweden, spend less per capita on healthcare than the U.S. while achieving better outcomes. The U.S. could adopt a hybrid model, such as a public option, to ease the transition. For instance, allowing individuals to buy into Medicare at age 50 could provide affordable coverage for those in the gig economy or small businesses. This approach wouldn’t eliminate private insurance but would ensure a safety net for all.

Implementing universal healthcare requires addressing political and logistical hurdles. Policymakers must navigate partisan divides, industry lobbying, and public skepticism. A phased rollout, starting with expansions to Medicaid and Medicare, could build momentum. Employers, too, have a role: offering opt-in public plans alongside private insurance could ease the transition. For individuals, staying informed and advocating for change is crucial. Join grassroots campaigns, contact representatives, and support candidates prioritizing healthcare reform. The path to universal coverage is complex, but the alternative—a fractured system leaving millions behind—is unsustainable.

Insurance and Economics: Understanding Risk Management's Role in Financial Systems

You may want to see also

Explore related products

$19.99 $25.99

![]()

Inadequate Mental Health Support

Mental health coverage in American insurance plans often falls short, leaving individuals struggling to access necessary care. Many plans impose strict limits on therapy sessions, typically capping coverage at 20 visits per year, despite clinical guidelines recommending weekly sessions for conditions like depression or anxiety. This disparity forces patients to choose between paying out-of-pocket for continued care or discontinuing treatment prematurely, exacerbating their mental health challenges.

Consider the case of a 32-year-old diagnosed with generalized anxiety disorder. Their insurance covers only 10 therapy sessions annually, but their therapist recommends 52 sessions for effective management. Without additional financial resources, this individual faces a treatment gap of 42 weeks, during which symptoms may worsen. Such limitations highlight how insurance inadequacies directly contribute to the mental health crisis in America.

To navigate these challenges, individuals should scrutinize their insurance policies for mental health coverage specifics. Look for terms like "parity" to ensure mental health benefits are equal to physical health benefits, as mandated by the Mental Health Parity and Addiction Equity Act. Additionally, explore supplemental insurance options or sliding-scale clinics that offer reduced fees based on income. Advocacy is also key—contacting state insurance commissioners or legislators can push for policy reforms that prioritize comprehensive mental health coverage.

Comparatively, countries like Germany and the UK integrate mental health services into their public health systems, ensuring broader access without financial barriers. In contrast, the U.S. system often treats mental health as an afterthought, with insurers prioritizing profit over patient well-being. This approach not only harms individuals but also strains societal resources, as untreated mental health issues contribute to higher healthcare costs, reduced productivity, and increased reliance on emergency services.

Ultimately, inadequate mental health support in American insurance is a systemic issue requiring collective action. By demanding transparency, exploring alternative resources, and advocating for policy changes, individuals can mitigate the impact of these shortcomings. Until insurers and policymakers prioritize mental health parity, the burden will remain on those already struggling—a reality that underscores the urgency for reform.

Does SimpliSafe Qualify for Insurance Discounts? What You Need to Know

You may want to see also

Frequently asked questions

Healthcare insurance in America is often criticized for its high costs, limited coverage, and complexity compared to systems in other developed countries. While it offers advanced medical care, many Americans struggle with affordability and access, leading to perceptions of it being "bad."

Many Americans lack adequate insurance due to high premiums, deductibles, and out-of-pocket costs, especially for those without employer-sponsored plans. Additionally, gaps in coverage, such as for pre-existing conditions or low-income individuals, contribute to the issue.

Yes, efforts like the Affordable Care Act (ACA) have expanded coverage and protections, but challenges remain. Ongoing debates focus on reducing costs, improving access, and exploring alternatives like a single-payer system to address systemic issues.