When considering whether Part B of Medicare is equivalent to your current insurance, it’s essential to compare coverage, costs, and benefits. Part B primarily covers outpatient services, doctor visits, preventive care, and medical supplies, while your present insurance may offer additional perks like vision, dental, or prescription drug coverage. Evaluate premiums, deductibles, and out-of-pocket expenses to determine which option aligns better with your healthcare needs and budget. Additionally, check if your current providers are in-network under Part B or your existing plan, as this can significantly impact accessibility and costs. Understanding these differences will help you make an informed decision about whether Part B meets your insurance requirements or if your current plan remains the better choice.

Explore related products

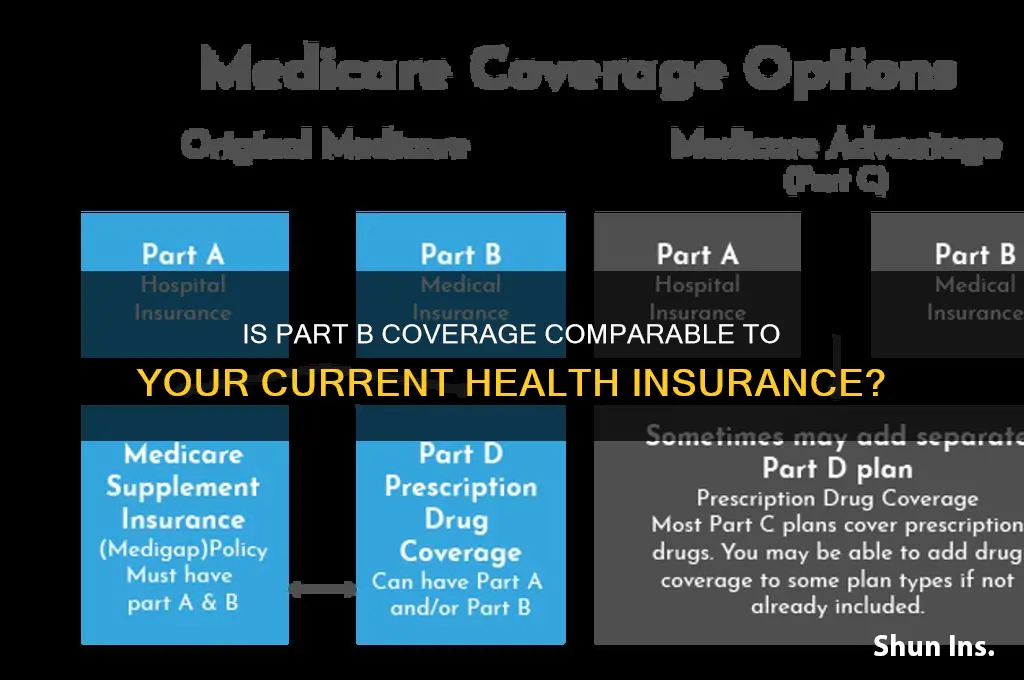

What You'll Learn

- Coverage Comparison: Analyze if Part B covers the same services as current insurance

- Cost Analysis: Compare premiums, deductibles, and out-of-pocket costs between Part B and current plan

- Provider Network: Check if Part B includes the same doctors and hospitals as current insurance

- Prescription Coverage: Evaluate if Part B covers medications equally to current plan

- Additional Benefits: Assess if Part B offers extra benefits not in current insurance

![]()

Coverage Comparison: Analyze if Part B covers the same services as current insurance

Part B of Medicare, often referred to as medical insurance, covers a specific set of services, including doctor visits, outpatient care, preventive services, and durable medical equipment. To determine if it mirrors your current insurance, start by listing all services covered under your present plan. Compare this list against Medicare’s Part B coverage guidelines, available on the official Medicare website. For instance, while Part B covers flu shots and diabetes screenings, it does not include long-term care or most dental services. Identify gaps or overlaps to assess equivalence.

Consider the frequency and extent of coverage for shared services. For example, Part B covers 80% of the Medicare-approved amount for doctor visits after you meet the annual deductible, which was $226 in 2023. If your current insurance covers 100% of doctor visits with no deductible, Part B would not be equal in this aspect. Similarly, Part B covers physical therapy only when deemed medically necessary, whereas your current plan might offer a set number of sessions annually. Analyzing these nuances ensures an accurate comparison.

Preventive services are a critical area to examine. Part B includes screenings like mammograms (every 12 months for women over 40) and colorectal cancer tests (every 24 months for those over 50). Compare these to your current plan’s preventive offerings. For instance, if your insurance covers additional screenings not included in Part B, such as genetic testing or annual full-body skin exams, Part B would fall short. Prioritize services based on your health needs to determine if Part B aligns with your expectations.

Finally, evaluate out-of-pocket costs, as they significantly impact coverage equality. Part B requires a monthly premium, typically $164.90 in 2023, and a 20% coinsurance for most services. If your current plan has lower premiums or no coinsurance, Part B may not be financially equivalent. Use Medicare’s Plan Finder tool to estimate total costs under Part B versus your current plan. This practical step ensures you’re not just comparing services but also the financial burden of each option.

Does Publix Accept CMS Insurance? Coverage and Payment Options Explained

You may want to see also

Explore related products

![]()

Cost Analysis: Compare premiums, deductibles, and out-of-pocket costs between Part B and current plan

Step 1: Dissect Your Current Plan’s Costs

Begin by mapping out the financial anatomy of your existing insurance. Note the monthly premium, annual deductible, and out-of-pocket maximum. For instance, if your plan charges $350 monthly with a $2,000 deductible and a $6,000 out-of-pocket cap, these are your baseline metrics. Include copays for specialist visits (e.g., $50 per visit) or prescription drug coverage (e.g., 20% coinsurance after deductible). If you’re over 65 or have a chronic condition requiring frequent care, these details become critical for comparison.

Step 2: Decode Medicare Part B’s Financial Structure

Medicare Part B operates on a standardized framework, but costs vary by income. In 2023, the standard monthly premium is $164.90, with a $226 annual deductible. However, beneficiaries earning above $97,000 (single) or $194,000 (married) face IRMAA surcharges, pushing premiums up to $560.40 monthly. Out-of-pocket costs are uncapped unless paired with a Medigap plan. For example, a routine outpatient procedure costing $1,500 would mean you pay $226 (deductible) plus 20% of the remaining $1,274 ($255), totaling $481.

Caution: Hidden Variables That Skew Comparisons

Direct cost comparisons can mislead without accounting for coverage gaps. Part B covers preventive services (e.g., flu shots, diabetes screenings) with no copay, while private plans may charge $25–$50 per visit. Conversely, Part B lacks prescription drug coverage, requiring a separate Part D plan. If your current plan includes drug coverage with a $40 monthly premium and $5 copays for tier-1 drugs, factor this into your Part B alternative (Part D plans average $30–$70 monthly).

Scenario Analysis: When Does Part B Outperform?

For a 67-year-old with moderate healthcare needs, Part B paired with a Medigap Plan G ($150–$300 monthly) could save money. Example: Annual costs for Part B + Medigap (~$3,180) vs. private insurance ($4,200 premium + $2,000 deductible) favor Part B if out-of-pocket expenses exceed $3,020. However, a healthy 65-year-old with low utilization might find a private plan’s $1,500 deductible and $300 monthly premium more cost-effective.

Takeaway: Tailor the Comparison to Your Healthcare Profile

To decide if Part B equals your current insurance, project annual costs based on your health status. Use Medicare’s Plan Finder tool to estimate Part B + Part D + Medigap expenses against your current plan. For instance, if you visit a specialist quarterly ($50 copay each under private insurance vs. 20% coinsurance under Part B), calculate which option minimizes total spend. Remember: Part B’s predictability (fixed deductible, no networks) may offset higher premiums for those with complex care needs.

Understanding GL Insurance: Coverage, Benefits, and Why It's Essential

You may want to see also

Explore related products

$29.41 $110

![]()

Provider Network: Check if Part B includes the same doctors and hospitals as current insurance

One critical aspect of evaluating whether Part B is equal to your present insurance is scrutinizing the provider network. Your current plan likely includes a specific list of doctors, specialists, and hospitals that you’re accustomed to. Part B, as part of Medicare, operates differently—it allows you to visit any healthcare provider who accepts Medicare. However, this doesn’t automatically mean your existing providers are included. For instance, if your current insurance is through a managed care plan like an HMO, your network is tightly controlled, whereas Part B offers more flexibility but requires verification. Start by cross-referencing your current provider list with Medicare’s database to ensure continuity of care.

To effectively compare networks, follow these steps: 1) Obtain a list of your current in-network providers, including primary care physicians, specialists, and hospitals. 2) Access Medicare’s “Physician Compare” tool (available on Medicare.gov) to check if these providers accept Medicare assignment. 3) Contact your providers directly to confirm their participation in Medicare, as some may accept Medicare but limit the number of Medicare patients they see. 4) Review Part B’s coverage rules for out-of-network care, which is generally not covered unless in an emergency. This process ensures you’re not caught off guard by unexpected out-of-pocket costs or disruptions in care.

A common misconception is that Part B automatically mirrors your current network. In reality, Medicare’s network is broader but not identical. For example, if your current insurance includes access to a prestigious academic medical center, that facility may accept Medicare, but specific departments or physicians might not. Similarly, rural residents may find fewer specialists in their area under Part B compared to their current plan. Analyzing these discrepancies requires a detailed side-by-side comparison, focusing on providers you rely on most, such as oncologists, cardiologists, or mental health professionals.

From a practical standpoint, transitioning to Part B without verifying the provider network can lead to significant inconvenience and expense. For instance, if your trusted rheumatologist doesn’t accept Medicare, you’ll either need to pay out-of-pocket or find a new specialist. To mitigate this, consider supplementing Part B with a Medigap plan, which may offer additional flexibility in choosing providers. Alternatively, if maintaining your current network is non-negotiable, explore Medicare Advantage plans, which often include provider networks similar to private insurance. The key is aligning Part B’s network with your healthcare needs, not assuming equivalence.

In conclusion, the provider network is a make-or-break factor in determining if Part B equals your present insurance. While Part B offers the advantage of widespread acceptance, it’s not a carbon copy of your current plan’s network. Proactive research, direct communication with providers, and strategic planning—such as pairing Part B with supplemental coverage—can bridge gaps and ensure seamless care. Treat this step as essential, not optional, in your transition to Medicare.

Progressive's Flo: Unveiling the Wealth Behind the Iconic Insurance Mascot

You may want to see also

Explore related products

$14.99 $14.95

![]()

Prescription Coverage: Evaluate if Part B covers medications equally to current plan

Part B of Medicare primarily covers medically necessary services and preventive care, but it does not typically include prescription drug coverage. This is a critical distinction when evaluating whether Part B is equal to your current insurance plan. If your present plan includes comprehensive prescription coverage, you’ll need to carefully assess how Part B aligns with your medication needs. For instance, Part B may cover certain drugs administered in a clinical setting, such as chemotherapy or injectable medications like insulin for diabetes, but it does not cover most oral or self-administered prescriptions. Understanding this limitation is the first step in determining if Part B meets your medication requirements.

To evaluate whether Part B covers medications equally to your current plan, start by listing all the prescriptions you take regularly. Note their dosages, frequencies, and whether they are self-administered or require a healthcare provider. For example, if you take a daily 20 mg dose of atorvastatin for cholesterol, Part B will not cover this, as it is an oral medication. However, if you require a monthly injection of a biologic drug like adalimumab for rheumatoid arthritis, Part B might cover it under its durable medical equipment or physician-administered drug benefits. Comparing this list to Part B’s coverage criteria will highlight gaps or overlaps.

A practical tip is to review the Medicare Part B formulary, which outlines the specific drugs covered under its limited prescription benefits. Additionally, consider enrolling in a standalone Part D prescription drug plan or a Medicare Advantage plan with prescription coverage to supplement Part B. For seniors over 65 or individuals with disabilities, this step is crucial, as relying solely on Part B for medications could lead to significant out-of-pocket costs. For example, a 90-day supply of a brand-name drug not covered by Part B could cost hundreds of dollars without supplemental coverage.

Finally, consult with a Medicare advisor or pharmacist to analyze your current plan’s prescription coverage against Part B’s limitations. They can help you identify potential cost savings or coverage gaps. For instance, if your current plan covers 80% of your medication costs after a $50 copay, compare this to the out-of-pocket expenses you’d incur under Part B and a supplemental plan. By taking a methodical approach, you can ensure that your prescription needs are adequately met, whether through Part B, additional coverage, or a combination of both.

Is Americo Insurance a Pyramid Scheme? Uncovering the Truth

You may want to see also

Explore related products

![]()

Additional Benefits: Assess if Part B offers extra benefits not in current insurance

Part B of Medicare often includes benefits that extend beyond what private insurance plans cover, making it a valuable supplement for certain individuals. For instance, Part B covers outpatient mental health services, including therapy sessions and psychiatric evaluations, which may be limited or require high copays under private plans. Additionally, Part B provides coverage for durable medical equipment (DME), such as wheelchairs or oxygen supplies, often with minimal out-of-pocket costs compared to private insurance, where such items might be partially covered or subject to strict pre-authorization requirements.

To assess whether Part B offers additional benefits, start by comparing its coverage to your current plan’s exclusions and limitations. For example, Part B covers preventive services like flu shots, diabetes screenings, and cardiovascular screenings at no cost, whereas private plans might charge a copay or coinsurance. If your current insurance caps the number of physical therapy sessions per year, Part B may offer more flexibility, as it covers medically necessary outpatient therapy without arbitrary limits. However, be cautious: Part B does not cover long-term care, dental care, or vision care, so ensure these gaps align with your needs.

A persuasive argument for Part B lies in its coverage of clinical research studies, a benefit rarely found in private insurance. If you’re considering participation in a trial for a chronic condition, Part B can cover routine costs associated with the study, reducing financial barriers to accessing cutting-edge treatments. Similarly, Part B includes coverage for certain medications administered in a doctor’s office, such as chemotherapy or intravenous antibiotics, which private plans might exclude or cover under a separate pharmacy benefit with higher costs.

Practically, evaluate your healthcare usage patterns to determine if Part B’s additional benefits outweigh the costs. For seniors aged 65 and older or individuals with disabilities, Part B’s comprehensive outpatient coverage can be a safeguard against unexpected medical expenses. However, if you rarely use outpatient services and prefer lower monthly premiums, your current insurance might suffice. To maximize value, consider pairing Part B with a Medigap policy to cover deductibles and coinsurance, ensuring a more predictable cost structure.

In conclusion, Part B’s additional benefits, such as expanded mental health services, DME coverage, and preventive care, can fill gaps in private insurance. By systematically comparing coverage areas and aligning them with your health needs, you can make an informed decision about whether Part B enhances your current insurance or duplicates it. Always review the specifics of both plans, including exclusions and out-of-pocket costs, to ensure you’re not paying for redundant coverage.

Can Insurance Brokers Access Your Driving Record? What You Need to Know

You may want to see also

Frequently asked questions

No, Part B (Medicare) primarily covers outpatient services, doctor visits, and preventive care, while your present insurance may offer broader coverage, including inpatient care, prescription drugs, and additional benefits.

It depends. Part B can work alongside your current insurance, but it may not fully replace it, especially if your current plan includes benefits not covered by Medicare.

Not necessarily. Part B has its own premiums, deductibles, and copayments, which may differ from your current insurance costs.

Part B coverage depends on whether your providers accept Medicare. Your current insurance may have a different network of providers.

No, Part B does not cover most prescription drugs. For drug coverage, you would need a separate Part D plan or a Medicare Advantage plan with drug benefits.