When taking out a mortgage, it is important to understand the different costs that are included in your monthly payments. While some mortgages only include the principal and interest, others also cover property tax and homeowners insurance. These additional expenses are typically managed through an escrow account set up by the lender, which helps to cover local tax obligations and protect your property and assets against damage or loss. However, it is possible to opt out of an escrow account and pay property taxes and insurance separately, although this may require more proactive financial planning. Understanding the components of your mortgage payments can help you better manage your budget and avoid surprises in your monthly expenses.

| Characteristics | Values |

|---|---|

| Are property tax and homeowners insurance included in the mortgage? | Yes, property tax and homeowners insurance are included in the mortgage payments. |

| Who sets up the escrow account? | The escrow account is usually set up by the lender. |

| What is the purpose of the escrow account? | The escrow account is used to manage the payments for property taxes, insurance and other expenses. |

| Can the homeowner pay the property taxes separately? | Yes, the homeowner can choose to pay the property taxes separately, but they will need to budget for any tax increases and make the payments directly to the local tax authority. |

| Can the homeowner pay the homeowners insurance separately? | Yes, the homeowner can pay the homeowners insurance separately, either directly to the insurance company or through an escrow account. |

| Factors affecting homeowners insurance premiums | Home value, location, construction type, down payment amount, and mortgage type. |

Explore related products

$4.99 $14.99

$10.81 $17.99

What You'll Learn

- Property tax is included in most mortgage payments

- Homeowners insurance is included in mortgage payments if you have an escrow account

- Lenders establish escrow accounts to handle property tax and insurance payments

- Property taxes can be paid separately, but you must budget accordingly

- Homeowners insurance is essential financial protection, even after your mortgage is paid off

![]()

Property tax is included in most mortgage payments

When it comes to mortgages, it's important to understand what's included in your monthly payments to avoid surprises. Property tax is included in most mortgage payments, along with the principal, interest, and homeowners insurance. This is typically managed through an escrow account set up by your lender, which helps cover essential protections and local tax obligations.

The escrow account ensures that your property tax and insurance payments are made on time. It is essentially a savings account managed by your lender or mortgage servicer, where a portion of your monthly mortgage payment is set aside to cover these expenses. The lender then uses this money to pay the bills on your behalf when they are due. This can include annual or biannual expenses, such as property taxes and insurance.

While property tax is included in most mortgage payments, it's important to note that there may be variations depending on the type of mortgage and the location. Some lenders may also allow you to pay the taxes directly to the local tax authority without using an escrow account. In such cases, you would need to budget accordingly and make sure to meet the payment deadlines, which can vary by location.

Additionally, it's worth mentioning that homeowners insurance is often included in mortgage payments through an escrow account, which most lenders require. This insurance provides essential financial protection for your home, which is one of your biggest financial assets. Even after your mortgage is paid off, maintaining home insurance is crucial to protect against damage costs.

Understanding the components of your mortgage payment, such as the principal, interest, property taxes, and insurance, can help you better manage your budget and plan for any fluctuations in expenses. It is always a good idea to consult with a financial expert or your lender to understand the specifics of your mortgage and how escrow accounts may impact your payments.

Earthquake Insurance in BC: Worth the Cost?

You may want to see also

Explore related products

![Manitoba Lands for Sale by Crotty & Cross, Real Estate Brokers, Financial and Insurance Agents Funds Invested on First Mortgage Security, Rents Collected, Taxes Paid, and 1893 [Leather Bound]](https://m.media-amazon.com/images/I/617DLHXyzlL._AC_UY218_.jpg)

![]()

Homeowners insurance is included in mortgage payments if you have an escrow account

When you apply for a mortgage preapproval, you and your lender will estimate your monthly payment, including the principal and interest, and also the estimated monthly escrow payment. Escrow accounts are established by lenders to handle property tax and insurance payments, ensuring they are made on time. Homeowners insurance is included in your mortgage payments if you have an escrow account, as most lenders require. Your escrow account is where you send payments for your mortgage, property taxes, and insurance. It is essentially a savings account managed by your mortgage servicer, used to pay annual or biannual expenses like property taxes and insurance on your behalf.

If you pay property taxes separately, fluctuations do not affect your monthly mortgage payment. However, you will need to budget accordingly to cover any tax increases yourself, as you will be responsible for paying the full amount directly to your tax authority when due. This can require more proactive financial planning but provides greater control over the timing of your tax payments.

If you choose not to use an escrow account for property taxes and insurance, you will be responsible for making those payments directly to the relevant authorities. This means you will need to keep track of payment deadlines, which vary by location — some municipalities require annual payments, while others may bill semi-annually or quarterly. You may be able to opt out of an escrow account depending on the type of mortgage you have, the size of your down payment, and your equity.

Homeowners insurance, along with other property-related costs, can significantly impact your monthly mortgage payment. When estimating these expenses, lenders often rely on average rates based on your area's ZIP code and nearby homes. However, your actual insurance cost depends on the specific policy you choose, including the level of coverage, deductible amount, and the insurance provider itself. If you bundle homeowners insurance with other policies, like auto insurance, you might qualify for a discount that lowers your overall cost.

Norwegian Cruise Insurance: Is It Worth the Cost?

You may want to see also

Explore related products

![]()

Lenders establish escrow accounts to handle property tax and insurance payments

When you apply for a mortgage, the lender will estimate your monthly escrow payment based on the typical costs for homes in the area. This estimate is used to determine your overall monthly mortgage payment. However, the actual costs for property taxes and insurance may vary depending on the specific home you choose and the policies you select.

It's important to note that the use of an escrow account is not mandatory for all mortgages. Some lenders may allow you to pay property taxes and insurance premiums directly to the tax authority and insurance company, respectively. Additionally, certain types of mortgages, such as conventional loans with a larger down payment, may qualify for an escrow waiver.

Homeowners should understand the components of their mortgage payment, including principal, interest, property taxes, and insurance. By managing their budget effectively and staying informed about local tax obligations and insurance options, homeowners can avoid surprises in their monthly expenses.

Overall, lenders establish escrow accounts as a common mechanism to handle property tax and insurance payments, providing convenience and peace of mind for homeowners.

Stewardship Reports: Insurance's Financial Health Check

You may want to see also

Explore related products

![]()

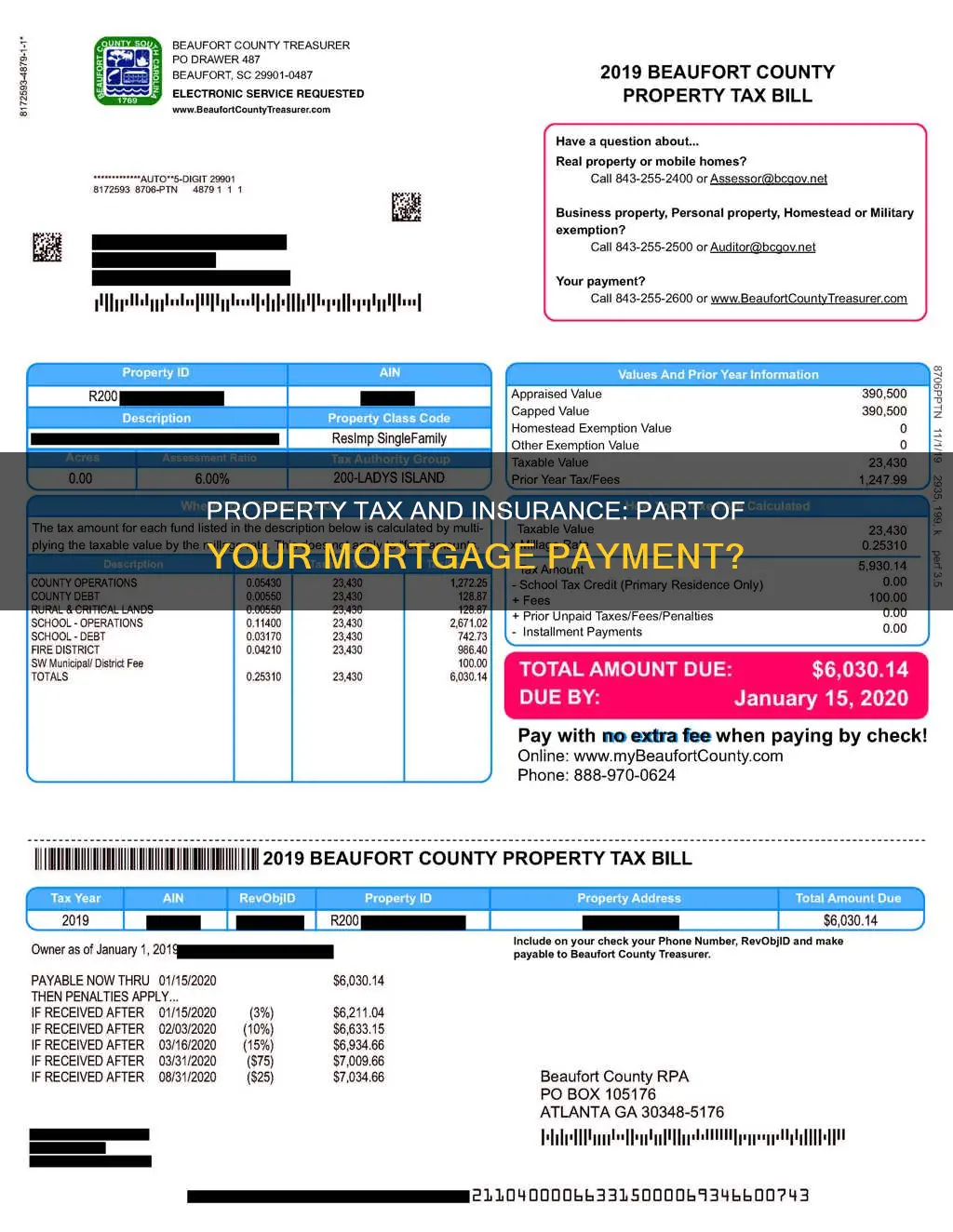

Property taxes can be paid separately, but you must budget accordingly

When it comes to property taxes, it's important to understand that they are typically included in your mortgage payments. However, you do have the option to pay them separately. This decision can have implications for your overall financial planning, so it's essential to carefully consider your choices.

If you choose to pay property taxes separately, you will need to budget accordingly to ensure you can cover any increases in taxes over time. This approach provides you with greater control over the timing of your tax payments. By opting out of an escrow account, you take on the responsibility of making direct payments to the local tax authority. This means staying on top of payment deadlines, which can vary depending on your location. Some areas may require annual payments, while others might bill on a semi-annual or quarterly basis.

The advantage of paying property taxes separately is that fluctuations in tax rates won't directly impact your monthly mortgage payments. However, it's crucial to plan for these payments diligently. Missing payments can lead to late fees or, in severe cases, a lien against your property. To avoid such issues, some homeowners set aside funds in a dedicated savings account to cover these tax obligations.

On the other hand, if you choose to include property taxes in your mortgage payments, your lender will typically set up an escrow account. This account ensures that a portion of your monthly mortgage payment goes towards covering your property taxes. The lender then pays the taxes on your behalf when they are due. This option simplifies your financial responsibilities and helps you avoid the risk of missed payments.

Additionally, it's worth noting that homeowners insurance is another critical component of your overall housing expenses. While it may be included in your mortgage payments through an escrow account, you can also choose to pay it separately. Homeowners insurance protects your property and assets against damage or loss, so it's essential to maintain coverage even after your mortgage is paid off.

In conclusion, property taxes can be paid separately from your mortgage, but it requires careful budgeting and financial planning. By understanding your options and staying informed about your tax obligations, you can make informed decisions that align with your financial goals and ensure the protection of your assets.

How Car Plate Changes Affect Your Insurance

You may want to see also

Explore related products

![]()

Homeowners insurance is essential financial protection, even after your mortgage is paid off

When it comes to homeownership, it's important to understand the costs involved beyond the monthly mortgage payment. While property taxes and homeowners insurance can be included in your mortgage payment, they are not technically part of the mortgage itself. These additional expenses are typically managed through an escrow account set up by your lender. However, it's worth noting that homeowners insurance, or home insurance, is separate from the mortgage loan agreement.

Homeowners insurance is essential financial protection for your home and belongings. Even after your mortgage is paid off, it is advisable to maintain a homeowners insurance policy to safeguard against financial risks. This type of insurance covers the structure of your home and helps pay for repairs or rebuilding in the event of disasters, such as fires, storms, or break-ins. Most policies also extend to detached structures on the property, like sheds or guest houses. Without homeowners insurance, you would be solely responsible for covering these potentially significant costs.

Additionally, homeowners insurance provides liability protection in the event of an injury or property damage lawsuit. This aspect of the policy is crucial, as it protects you from financial loss in the case of unforeseen legal issues. While mortgage insurance protects the lender in case of default on loan payments, homeowners insurance offers direct financial protection to you as the homeowner. This distinction is important to understand, as it highlights how homeowners insurance safeguards your financial interests specifically.

The cost of homeowners insurance depends on the level of coverage, deductible amount, and the chosen insurance provider. It's worth noting that bundling homeowners insurance with other policies, such as auto insurance, can often result in discounts that lower your overall insurance costs. When considering homeowners insurance, it's essential to shop around and compare policies to find the right level of coverage at a price that fits within your budget.

In summary, homeowners insurance provides essential financial protection for your home, belongings, and liability concerns. Even after paying off your mortgage, maintaining a homeowners insurance policy is a prudent decision to safeguard your financial well-being and ensure you're covered in the event of disasters or legal issues. By understanding the importance of homeowners insurance, you can confidently manage your budget and protect your assets.

Mold Remediation: Is Insurance Claim Worth the Hassle?

You may want to see also

Frequently asked questions

Property tax is included in most mortgage payments. However, you can also pay property taxes separately, in which case fluctuations in property tax won't affect your monthly mortgage payments.

Homeowners insurance is typically included in mortgage payments if you have an escrow account, as most lenders require. However, you can also pay your homeowners insurance directly to the insurance company.

An escrow account is a savings account managed by your lender that sets aside money for property tax and insurance payments.

Your lender will set up the escrow account to collect funds for property taxes and insurance, and then pay these bills when they're due.