The Affordable Care Act (ACA), often referred to as Obamacare, remains in effect as of the latest updates, despite numerous challenges and attempts to repeal or replace it since its enactment in 2010. Signed into law by President Barack Obama, the ACA aimed to increase the quality and affordability of health insurance, lower the uninsured rate, and reduce the costs of healthcare for individuals and the government. Over the years, it has undergone various modifications, including key provisions upheld by the Supreme Court and adjustments made during different presidential administrations. While debates about its effectiveness and future persist, the ACA continues to play a significant role in shaping the U.S. healthcare system, providing coverage to millions of Americans through expanded Medicaid, health insurance marketplaces, and protections for individuals with pre-existing conditions.

| Characteristics | Values |

|---|---|

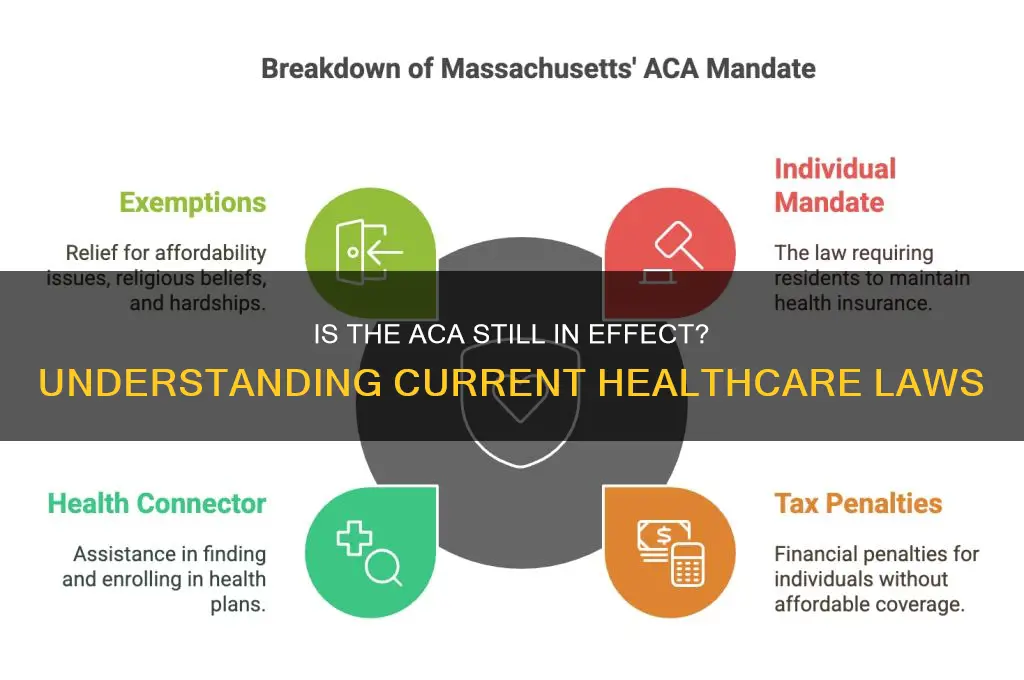

| Current Status | The Affordable Care Act (ACA) is still in effect as of October 2023. |

| Key Provisions | - Pre-existing conditions protections - Medicaid expansion - Health insurance marketplaces - Young adults staying on parents' plans until 26 - Essential health benefits mandate |

| Legal Challenges | Survived multiple Supreme Court challenges, including California v. Texas (2021). |

| Enrollment Trends | Record-high enrollment in 2023, with over 16 million people signing up. |

| Premium Subsidies | Enhanced subsidies extended through 2025 under the Inflation Reduction Act (IRA). |

| State Implementation | 40 states (including D.C.) have expanded Medicaid under the ACA. |

| Public Opinion | Majority support for the ACA, with approval ratings consistently above 50%. |

| Recent Updates | IRA (2022) strengthened ACA by lowering premiums and expanding eligibility. |

| Future Outlook | No imminent threats to repeal; bipartisan support for certain provisions. |

Explore related products

$36.33 $54.99

What You'll Learn

![]()

Current Status of ACA

The Affordable Care Act (ACA), often referred to as Obamacare, remains in effect as of the latest updates. Despite numerous challenges and attempts to repeal or replace it, the ACA continues to be a cornerstone of the U.S. healthcare system. The law’s core provisions, such as the prohibition on denying coverage for pre-existing conditions, the expansion of Medicaid, and the establishment of health insurance marketplaces, are still fully operational. These elements ensure that millions of Americans have access to affordable and comprehensive health insurance.

One of the most significant indicators of the ACA’s current status is its resilience through legal challenges. The Supreme Court has upheld the ACA in several key cases, most recently in *California v. Texas* (2021), where the Court ruled that the plaintiffs lacked standing to challenge the law’s individual mandate. While the individual mandate’s penalty was reduced to $0 in 2019, the Court’s decision solidified the ACA’s legal standing. This ruling reaffirmed that the ACA remains the law of the land, providing stability for both consumers and insurers.

The ACA’s marketplaces have also demonstrated continued strength and growth. Enrollment in ACA-compliant plans has reached record highs in recent years, with over 16 million Americans signing up for coverage during the 2023 open enrollment period. This increase is partly due to expanded subsidies under the American Rescue Plan Act (ARPA) of 2021, which made premiums more affordable for many individuals and families. These subsidies have been extended through 2025, further stabilizing the marketplaces and ensuring continued access to affordable coverage.

Medicaid expansion, another critical component of the ACA, has been adopted by 40 states and the District of Columbia, covering millions of low-income adults. While some states have yet to expand Medicaid, advocacy efforts continue to push for broader adoption. The ACA’s Medicaid expansion has been instrumental in reducing uninsured rates and improving access to care, particularly in states that have embraced it. Efforts to strengthen Medicaid and address gaps in coverage remain a focus for policymakers and healthcare advocates.

In summary, the ACA is still in effect and continues to play a vital role in the U.S. healthcare system. Its core provisions remain intact, and recent policy changes have further strengthened its impact. While challenges and debates persist, the ACA’s resilience and ongoing improvements underscore its importance in ensuring access to affordable, quality healthcare for millions of Americans. As the healthcare landscape evolves, the ACA remains a foundational element of efforts to expand coverage and protect consumers.

Colonial Penn Life Insurance: What You Need to Know

You may want to see also

Explore related products

![]()

Key Provisions Still Active

The Affordable Care Act (ACA), also known as Obamacare, remains in effect, and several of its key provisions continue to shape the U.S. healthcare landscape. One of the most significant provisions still active is the guaranteed issue and community rating requirements. These provisions ensure that insurance companies cannot deny coverage or charge higher premiums based on pre-existing conditions. This protection remains a cornerstone of the ACA, providing millions of Americans with access to affordable health insurance regardless of their health status. Individuals with chronic illnesses, such as diabetes or cancer, can still obtain coverage without fear of discrimination, a critical safeguard that continues to benefit countless families.

Another key provision still active is the expansion of Medicaid eligibility. While not all states have adopted the Medicaid expansion, those that have done so continue to provide coverage to low-income adults who were previously ineligible. This expansion has significantly reduced the uninsured rate in participating states, offering essential healthcare services to millions. The ACA’s Medicaid expansion remains a vital tool for addressing healthcare disparities and ensuring that vulnerable populations have access to necessary medical care.

The marketplace subsidies are also still in effect, providing financial assistance to individuals and families who purchase health insurance through the ACA marketplaces. These subsidies, formally known as Advanced Premium Tax Credits (APTC), help reduce monthly premiums and out-of-pocket costs for eligible enrollees. Recent enhancements under the American Rescue Plan and Inflation Reduction Act have further expanded these subsidies, making coverage more affordable for a broader range of income levels. This provision remains a critical component of the ACA’s efforts to make health insurance accessible to middle-class Americans.

Additionally, the young adult coverage provision remains active, allowing young adults to stay on their parents’ health insurance plans until age 26. This measure has been particularly beneficial for recent graduates and young workers who may not yet have access to employer-sponsored insurance. Since its implementation, millions of young adults have gained coverage through this provision, contributing to a significant reduction in the uninsured rate among this demographic.

Lastly, the essential health benefits (EHBs) requirement is still in place, ensuring that all ACA-compliant plans cover a comprehensive set of services, including hospitalization, prescription drugs, maternity care, and mental health services. This provision prevents insurers from offering skimpy plans that exclude critical care, providing consumers with more robust coverage options. The EHBs remain a fundamental aspect of the ACA’s commitment to improving the quality and scope of health insurance available to Americans.

In summary, while the ACA has faced political and legal challenges, its key provisions remain active and continue to play a vital role in expanding access to healthcare. From protections for pre-existing conditions to financial assistance and comprehensive coverage requirements, these provisions ensure that the ACA’s impact endures, benefiting millions of Americans nationwide.

Gestational Diabetes: Life Insurance Complications and Considerations

You may want to see also

Explore related products

![]()

Recent Legal Challenges

The Affordable Care Act (ACA), often referred to as Obamacare, has faced numerous legal challenges since its inception in 2010. Despite these challenges, the ACA remains in effect, though recent legal battles have continued to test its constitutionality and scope. One of the most significant recent challenges came in the case of *California v. Texas* (2021), where the Supreme Court ruled 7-2 that the states challenging the ACA lacked standing to bring the case. The lawsuit argued that the ACA’s individual mandate, which was effectively eliminated by Congress in 2017 when the tax penalty was reduced to $0, rendered the entire law unconstitutional. However, the Court declined to strike down the ACA, preserving its provisions, including protections for pre-existing conditions, Medicaid expansion, and the health insurance marketplaces.

Another notable legal challenge emerged in 2022 with *Kelley v. Becerra*, where plaintiffs argued that the ACA’s cost-sharing reductions, which help lower-income individuals afford out-of-pocket costs, were unlawfully funded. While this case did not threaten the ACA’s core structure, it highlighted ongoing disputes over the law’s implementation and funding mechanisms. The Biden administration has defended these provisions, emphasizing their importance in maintaining affordable healthcare access for millions of Americans.

In addition to federal challenges, state-level lawsuits have targeted specific aspects of the ACA. For instance, some states have contested the ACA’s contraceptive mandate, claiming it violates religious freedoms. These cases, such as *Little Sisters of the Poor v. Pennsylvania* (2020), have led to adjustments in the mandate’s enforcement but have not undermined the ACA’s overall framework. The Supreme Court upheld the Trump administration’s rules allowing employers with religious or moral objections to opt out of providing contraceptive coverage, demonstrating the ongoing tension between ACA provisions and religious liberty claims.

Furthermore, the ACA’s Medicaid expansion has faced legal scrutiny in states that have resisted implementing it. While the Supreme Court ruled in *National Federation of Independent Business v. Sebelius* (2012) that states could not be coerced into expanding Medicaid, recent efforts by advocacy groups have pushed for expansion through ballot initiatives in holdout states. These initiatives reflect the ACA’s resilience and the continued push for broader healthcare access, despite legal and political opposition.

Overall, while the ACA has withstood major legal challenges, it remains a target for litigation, particularly around its funding, mandates, and implementation. The Biden administration has taken steps to strengthen the law, such as expanding enrollment periods and increasing subsidies under the American Rescue Plan. As legal battles persist, the ACA’s future will depend on judicial interpretations, legislative actions, and public support for its core goals of affordability and accessibility in healthcare.

Join New York Life Insurance: A Guide to Applying

You may want to see also

Explore related products

![]()

Impact on Health Insurance

The Affordable Care Act (ACA), often referred to as Obamacare, remains in effect as of the latest updates, and its impact on health insurance continues to be significant. One of the most notable effects is the expansion of health insurance coverage to millions of Americans. The ACA introduced key provisions such as the Medicaid expansion, which allowed states to extend eligibility to more low-income individuals and families. This has resulted in a substantial reduction in the uninsured rate, ensuring that more people have access to essential health services. For health insurance providers, this expansion means a larger pool of insured individuals, which can help spread risk and stabilize premiums over time.

Another critical impact of the ACA on health insurance is the establishment of health insurance marketplaces. These marketplaces provide a platform for individuals and small businesses to compare and purchase health insurance plans. The ACA mandates that all plans offered through these marketplaces must cover essential health benefits, including preventive care, prescription drugs, and mental health services. This standardization has improved the quality of health insurance plans available to consumers, ensuring that they receive comprehensive coverage. Additionally, the availability of subsidies and tax credits for eligible individuals has made health insurance more affordable, further increasing enrollment rates.

The ACA has also introduced consumer protections that have reshaped the health insurance landscape. Insurers are now prohibited from denying coverage or charging higher premiums based on pre-existing conditions, a practice that previously left many individuals without access to affordable insurance. This provision has been particularly beneficial for those with chronic illnesses or prior health issues. Furthermore, the ACA requires insurers to allow young adults to remain on their parents’ health insurance plans until the age of 26, which has increased coverage among young adults and provided them with greater financial security during their early careers.

For health insurance companies, the ACA has necessitated adjustments in how they operate and structure their plans. The law’s emphasis on preventive care and wellness programs has encouraged insurers to invest in initiatives that promote long-term health, potentially reducing overall healthcare costs. However, the ACA’s regulations and mandates have also introduced administrative challenges and compliance costs for insurers. Balancing these requirements while maintaining profitability has been a key focus for the industry. Despite these challenges, the ACA has fostered a more competitive and consumer-friendly health insurance market.

Lastly, the ACA’s impact on health insurance extends to the overall affordability and accessibility of coverage. The law’s cost-sharing reductions and premium tax credits have made health insurance more attainable for low- and middle-income individuals and families. This financial assistance has been crucial in offsetting the rising costs of healthcare and ensuring that insurance remains within reach for a broader population. As the ACA continues to be in effect, its provisions will likely remain a cornerstone of the U.S. health insurance system, influencing both policy and practice for years to come.

Understanding ICHRA Insurance: Benefits, Eligibility, and How It Works

You may want to see also

Explore related products

$15.38 $26.99

![]()

Future of ACA Reforms

The Affordable Care Act (ACA), often referred to as Obamacare, remains in effect as of the latest updates, despite numerous challenges and attempts to repeal or replace it. Its continued existence underscores its importance in the U.S. healthcare system, providing coverage to millions of Americans through expanded Medicaid, health insurance marketplaces, and consumer protections like prohibiting denial of coverage for pre-existing conditions. However, the future of ACA reforms is a critical topic, as policymakers, stakeholders, and advocates seek to address its limitations and adapt it to evolving healthcare needs. The Biden administration has taken steps to strengthen the ACA, such as increasing subsidies for marketplace plans and reopening enrollment periods, but long-term reforms are necessary to ensure its sustainability and effectiveness.

One key area for future ACA reforms is addressing affordability and accessibility. While the ACA has significantly reduced the uninsured rate, many individuals and families still struggle with high premiums, deductibles, and out-of-pocket costs. Policymakers could explore expanding subsidies further, particularly for middle-income households that fall above the current eligibility thresholds. Additionally, introducing a public option—a government-backed health insurance plan—could increase competition in the marketplace and drive down costs. Such reforms would require bipartisan cooperation or strategic use of budget reconciliation, given the current political landscape, but they are essential to making healthcare truly affordable for all.

Another critical aspect of future ACA reforms is strengthening Medicaid expansion. While the ACA originally envisioned all states expanding Medicaid, several states have yet to do so, leaving millions of low-income individuals in the "coverage gap" without access to affordable insurance. Federal incentives, such as increased matching funds or waivers for innovative state programs, could encourage holdout states to expand Medicaid. Furthermore, addressing disparities in healthcare access and outcomes, particularly for marginalized communities, must be a priority. Reforms could include targeted investments in community health centers, cultural competency training for providers, and data collection to monitor and address inequities.

The future of ACA reforms must also focus on improving the stability and functionality of the health insurance marketplaces. Despite their success in providing coverage options, the marketplaces face challenges like insurer exits in certain regions and limited plan choices. Policymakers could implement measures such as reinsurance programs to stabilize premiums, encourage more insurers to participate, and enhance consumer assistance programs to help individuals navigate their options. Additionally, addressing surprise medical billing and prescription drug costs, which remain significant concerns for many Americans, could be integrated into broader ACA reforms to provide more comprehensive relief.

Finally, the long-term sustainability of the ACA depends on its ability to adapt to changing healthcare trends and technologies. Telehealth, for example, gained prominence during the COVID-19 pandemic and has the potential to improve access to care, particularly in rural areas. Permanently expanding telehealth coverage under the ACA could be a forward-looking reform. Similarly, investing in preventive care and chronic disease management could reduce overall healthcare costs and improve outcomes. By embracing innovation and focusing on prevention, the ACA can remain a cornerstone of the U.S. healthcare system for years to come.

In conclusion, the future of ACA reforms is multifaceted and requires a proactive approach to address affordability, accessibility, equity, and sustainability. While the ACA remains in effect and continues to provide critical protections, its long-term success hinges on strategic reforms that build on its strengths and address its shortcomings. By prioritizing these areas, policymakers can ensure that the ACA evolves to meet the needs of a diverse and changing population, ultimately fulfilling its promise of affordable, quality healthcare for all Americans.

Annuities and Whole Life Insurance: What's the Difference?

You may want to see also

Frequently asked questions

Yes, the ACA, also known as Obamacare, is still in effect. Despite various challenges and attempts to repeal it, the law remains active and continues to regulate health insurance markets and provide coverage options for millions of Americans.

No, the ACA has not been repealed or replaced. While some provisions have been modified or removed, such as the individual mandate penalty being reduced to $0 in 2019, the core structure of the law remains intact.

Yes, ACA-compliant health insurance plans are still available for purchase through HealthCare.gov or state-based marketplaces. Open enrollment periods occur annually, and special enrollment periods may apply for those with qualifying life events.