The question of whether the health insurance penalty is prorated is an important one for individuals and families who may not have maintained continuous coverage throughout the year. In the context of the Affordable Care Act (ACA), the penalty for not having health insurance is calculated based on the number of months a person goes without coverage. This means that if someone only lacks coverage for part of the year, the penalty amount will be adjusted accordingly. Understanding how this proration works can help people better plan their finances and make informed decisions about their health insurance options.

Explore related products

What You'll Learn

- Definition of Proration: Understanding how penalties are calculated based on the duration of non-compliance

- Penalty Calculation: Insight into the formula used to determine the prorated penalty amount

- Qualifying Factors: Exploring conditions under which a penalty might be prorated

- Impact on Premiums: Analyzing how prorated penalties affect future insurance premium rates

- Legal and Policy Implications: Discussing the legal basis and policy considerations behind prorating health insurance penalties

![]()

Definition of Proration: Understanding how penalties are calculated based on the duration of non-compliance

Proration in the context of health insurance penalties refers to the method of calculating the penalty amount based on the duration of non-compliance with the insurance mandate. This approach ensures that the penalty is proportionate to the length of time an individual or entity has been without the required coverage. The concept of prorated penalties is designed to encourage compliance by imposing a financial consequence that increases the longer one remains uninsured.

To understand how prorated penalties work, it's essential to know the specific rules and regulations set forth by the governing body, such as the Internal Revenue Service (IRS) in the United States. Generally, the penalty is calculated on a monthly basis, and the total penalty for a year is the sum of the monthly penalties. For example, if an individual is uninsured for six months, they would be subject to six monthly penalties, which would be added together to determine the total penalty for that year.

The calculation of the monthly penalty often involves a percentage of the individual's income or a fixed dollar amount, whichever is greater. This ensures that the penalty is significant enough to deter non-compliance while also being fair and not overly burdensome. The specific percentage or dollar amount can vary depending on the jurisdiction and the year in question.

One important aspect of prorated penalties is that they can be applied retroactively. This means that if an individual or entity becomes compliant with the insurance mandate after a period of non-compliance, they may still be subject to penalties for the time they were uninsured. This retroactive application serves as an additional incentive to maintain continuous coverage and avoid gaps in insurance.

In conclusion, the prorated penalty system is a nuanced approach to enforcing health insurance mandates. By tying the penalty amount to the duration of non-compliance, it aims to strike a balance between encouraging compliance and ensuring fairness. Understanding how these penalties are calculated is crucial for individuals and entities to make informed decisions about their health insurance coverage and avoid unnecessary financial consequences.

How to Easily Check Your Health Insurance Status: A Quick Guide

You may want to see also

Explore related products

![]()

Penalty Calculation: Insight into the formula used to determine the prorated penalty amount

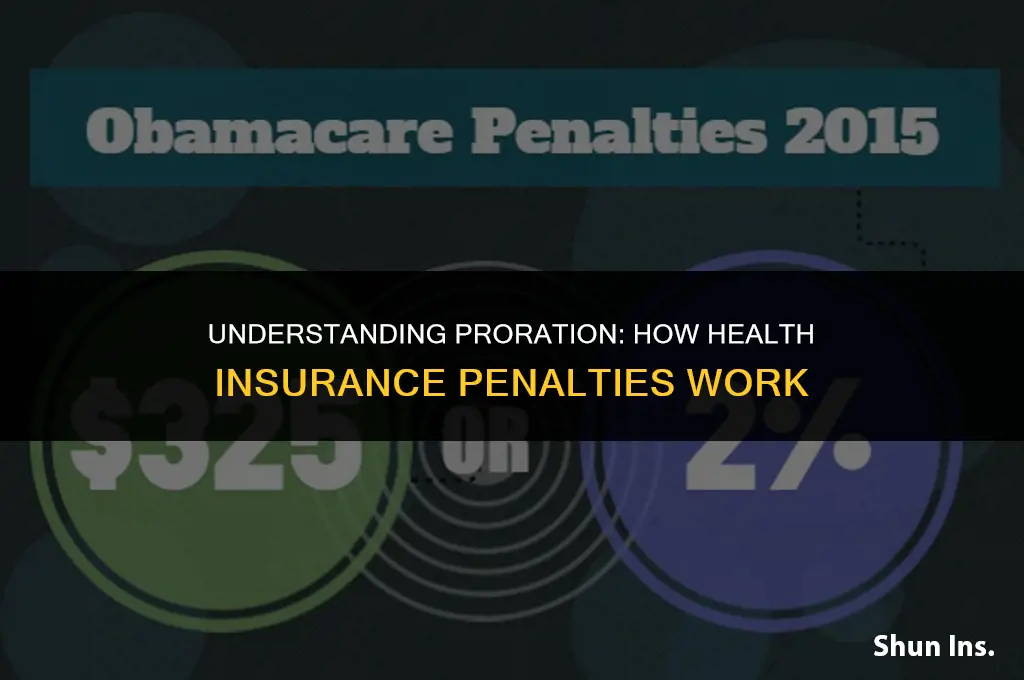

The prorated penalty amount for health insurance is calculated using a specific formula that takes into account the number of months an individual is without coverage. This formula is designed to ensure that the penalty is fair and proportional to the duration of the coverage gap. To calculate the prorated penalty, one must first determine the total penalty amount for a full year without coverage. This amount is then divided by 12 to find the monthly penalty. Finally, the monthly penalty is multiplied by the number of months the individual is without coverage to arrive at the prorated penalty amount.

For example, if the total penalty for a full year without coverage is $695, the monthly penalty would be $695 divided by 12, which equals $57.92. If an individual is without coverage for 5 months, the prorated penalty would be $57.92 multiplied by 5, resulting in a penalty of $289.60. This formula ensures that the penalty is proportional to the duration of the coverage gap, rather than imposing a flat fee regardless of the length of time without coverage.

It is important to note that the prorated penalty amount is only applicable to individuals who are required to have health insurance under the Affordable Care Act (ACA). Individuals who are exempt from the ACA's individual mandate, such as those who are covered by employer-sponsored insurance or Medicaid, are not subject to the prorated penalty calculation. Additionally, the prorated penalty amount is only applicable to individuals who are without coverage for part of the year. If an individual is without coverage for the entire year, they would be subject to the full penalty amount.

In conclusion, the prorated penalty calculation is a fair and proportional method for determining the penalty amount for individuals who are without health insurance coverage for part of the year. By taking into account the number of months without coverage, the formula ensures that the penalty is not overly burdensome for those who experience a brief coverage gap.

A Comprehensive Guide to Buying Health Insurance in Florida

You may want to see also

Explore related products

![]()

Qualifying Factors: Exploring conditions under which a penalty might be prorated

To determine if a health insurance penalty is prorated, one must consider several qualifying factors. These factors typically relate to the individual's circumstances and the specifics of their health insurance coverage. For instance, if an individual experiences a qualifying life event, such as a change in employment status, marriage, or the birth of a child, they may be eligible for a prorated penalty. This is because such events can impact their ability to maintain continuous health insurance coverage.

Another qualifying factor could be the individual's income level. In some cases, if an individual's income falls below a certain threshold, they may be exempt from the penalty altogether or have it prorated based on their ability to pay. This is often determined by the state or federal guidelines governing health insurance penalties.

Additionally, the type of health insurance plan an individual has can also affect whether the penalty is prorated. For example, if an individual is enrolled in a short-term health insurance plan, they may not be subject to the same penalty rules as those with long-term coverage. Similarly, individuals with grandfathered health insurance plans may have different penalty structures compared to those with newer plans.

It's also important to consider the timing of the penalty. If an individual is penalized for not having health insurance during a specific period, but they subsequently obtain coverage, the penalty may be prorated based on the duration of their uninsured period. This can vary depending on the state or federal regulations governing health insurance penalties.

In conclusion, the proration of a health insurance penalty depends on various qualifying factors, including life events, income level, type of health insurance plan, and timing of the penalty. Understanding these factors can help individuals navigate the complexities of health insurance penalties and potentially reduce their financial burden.

Will Insurance Companies Cover Professionals in High-Risk Occupations?

You may want to see also

Explore related products

![]()

Impact on Premiums: Analyzing how prorated penalties affect future insurance premium rates

The impact of prorated penalties on future insurance premium rates is a critical aspect to consider when discussing health insurance. Prorated penalties refer to the practice of adjusting the penalty amount based on the duration of the coverage gap. This means that if an individual fails to maintain continuous coverage, the penalty they face will be proportional to the length of time they were uninsured.

Analyzing this impact requires a deep dive into the mechanics of insurance premium calculations. Insurance companies use a variety of factors to determine premium rates, including the insured's age, health status, location, and claims history. Prorated penalties can influence these calculations by introducing an additional variable that reflects the insured's coverage continuity.

One potential effect of prorated penalties is that they may incentivize individuals to maintain continuous coverage, thereby reducing the likelihood of coverage gaps and associated penalties. This could lead to a more stable insurance pool, as individuals are less likely to drop coverage and then seek to reinstate it later. As a result, insurance companies may be able to offer lower premium rates to policyholders who demonstrate a history of continuous coverage.

On the other hand, prorated penalties could also have the opposite effect. If the penalty for a coverage gap is perceived as too high, individuals may be deterred from seeking coverage at all, leading to a decrease in the overall insurance pool. This could result in higher premium rates for those who do maintain coverage, as the insurance company seeks to recoup the costs associated with the reduced pool size.

To mitigate these potential impacts, it is essential for policymakers and insurance companies to carefully consider the design and implementation of prorated penalty systems. This may involve conducting thorough analyses of the potential effects on premium rates, as well as engaging in public education campaigns to ensure that individuals understand the implications of coverage gaps and associated penalties.

In conclusion, the impact of prorated penalties on future insurance premium rates is a complex issue that requires careful consideration. By understanding the mechanics of premium calculations and the potential effects of prorated penalties, policymakers and insurance companies can work together to design systems that promote continuous coverage and stable insurance pools, ultimately benefiting both insurers and insureds alike.

Applying for Medicaid: A Step-by-Step Guide to Getting Covered

You may want to see also

Explore related products

![]()

Legal and Policy Implications: Discussing the legal basis and policy considerations behind prorating health insurance penalties

The legal basis for prorating health insurance penalties often stems from the Affordable Care Act (ACA), which mandates that individuals maintain minimum essential coverage throughout the year. However, recognizing that life circumstances can change, the ACA allows for certain exceptions and adjustments. Prorating penalties is one such adjustment, designed to ensure that the penalty reflects the actual duration of non-compliance. This approach is rooted in the principle of fairness, aiming to avoid imposing unduly harsh penalties on individuals who only briefly fall short of the coverage requirement.

Policy considerations behind prorating penalties include the need to balance enforcement of the coverage mandate with flexibility for policyholders. By prorating penalties, policymakers can encourage individuals to seek coverage as soon as possible after a lapse, rather than facing a full year's penalty for a brief period of non-compliance. This can lead to better health outcomes and more equitable treatment of policyholders. Additionally, prorating penalties can help to address concerns about the affordability of health insurance, as it reduces the financial burden on individuals who may be struggling to maintain coverage.

Implementing prorated penalties requires careful consideration of various factors, such as the method of calculation, the timing of penalty imposition, and the communication of prorated penalties to policyholders. Insurers must develop clear and transparent processes for determining prorated penalties, taking into account the specific circumstances of each case. This may involve coordinating with healthcare providers and other stakeholders to ensure accurate tracking of coverage periods. Furthermore, insurers must effectively communicate prorated penalties to policyholders, explaining how the penalty was calculated and what steps they can take to avoid future penalties.

In practice, prorating penalties can have significant implications for both insurers and policyholders. For insurers, prorated penalties may result in lower revenue from penalties, but they can also lead to increased administrative costs associated with tracking and calculating prorated amounts. For policyholders, prorated penalties can provide financial relief, but they may also create confusion and complexity in understanding their coverage obligations. To mitigate these challenges, insurers and policymakers must work together to develop clear guidelines and educational materials that explain the prorated penalty system in an accessible and straightforward manner.

Ultimately, the legal and policy implications of prorating health insurance penalties revolve around the need to balance the enforcement of coverage mandates with fairness and flexibility for policyholders. By carefully considering the legal basis and policy considerations behind prorated penalties, insurers and policymakers can develop effective strategies that promote better health outcomes and more equitable treatment of individuals.

Does Health Insurance Cover Ultrasounds? What You Need to Know

You may want to see also

Frequently asked questions

"Prorated" in the context of health insurance penalties means that the penalty amount is adjusted proportionally based on the length of time you were without coverage during the year.

If the health insurance penalty is prorated, it is calculated based on the number of months you were without coverage. The penalty amount is divided by 12 (the number of months in a year) and then multiplied by the number of months you were uninsured.

The prorated penalty typically applies to individual health insurance plans and not to employer-sponsored plans. However, it's essential to check the specific terms of your plan or consult with a healthcare professional to confirm.

If you have a gap in coverage during the year and the penalty is prorated, you will only be penalized for the months you were without coverage. The penalty will be calculated based on the length of the gap.

Yes, if you have a prorated plan and maintain coverage for most of the year, you can avoid or minimize the health insurance penalty. The penalty will only apply to the months you were without coverage, so the longer you maintain coverage, the lower the penalty will be.