The question of whether payments made for health insurance are taxable is a common concern for individuals and businesses alike. In many jurisdictions, health insurance premiums can be considered tax-deductible expenses, reducing the overall taxable income of the policyholder. However, the specific tax treatment of health insurance payments can vary depending on factors such as the type of insurance plan, the jurisdiction in which the policy is issued, and the individual's or business's tax situation. It is essential to consult with a tax professional or refer to the relevant tax laws and regulations to determine the tax implications of health insurance payments in a particular case.

| Characteristics | Values |

|---|---|

| Taxability | The payment made for health insurance is not taxable. |

| Applicability | This applies to payments made by individuals or employers for health insurance premiums. |

| Conditions | The health insurance plan must be a qualified plan under the Internal Revenue Code. |

| Limitations | There may be limitations on the amount of premiums that can be deducted or excluded from income. |

| Documentation | Proper documentation of the payments and the health insurance plan is required. |

| Reporting | The payments may need to be reported on tax forms, such as Form 1040 or Form W-2. |

| Exceptions | Certain exceptions may apply, such as for self-employed individuals or for payments made for non-qualified plans. |

| Amendments | The tax laws regarding health insurance payments may be subject to change or amendment. |

| Consultations | It is recommended to consult with a tax professional or the IRS for specific guidance on the taxability of health insurance payments. |

| References | For more information, refer to IRS publications and resources on health insurance and taxes. |

Explore related products

What You'll Learn

- General Rule: Payments for health insurance are typically not tax-deductible as personal expenses

- Exceptions: Certain circumstances, like self-employment or specific medical conditions, may allow for deductions

- Itemized Deductions: Health insurance premiums can be itemized if they exceed a certain percentage of income

- Tax Credits: Some individuals may qualify for tax credits to offset health insurance costs

- State Variations: State tax laws may differ, potentially allowing for deductions or credits not available federally

![]()

General Rule: Payments for health insurance are typically not tax-deductible as personal expenses

In the realm of tax deductions, health insurance payments often lead to confusion. The general rule is clear: payments for health insurance are typically not tax-deductible as personal expenses. This means that when you pay for your own health insurance, you cannot deduct these payments from your taxable income. The IRS considers health insurance premiums to be a personal expense, much like other personal expenses such as rent, utilities, or groceries, which are not deductible.

However, there are exceptions to this rule. For instance, if you are self-employed, you may be able to deduct your health insurance premiums as a business expense. This is because, as a self-employed individual, you are responsible for providing your own health insurance, and it is considered a necessary business expense. Additionally, if you itemize your deductions on Schedule A of your tax return, you may be able to deduct the portion of your medical expenses that exceeds 7.5% of your adjusted gross income, including health insurance premiums.

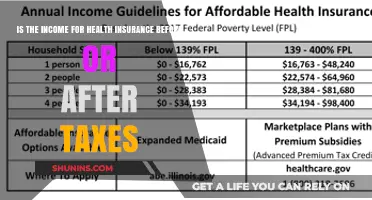

Another important consideration is the impact of the Affordable Care Act (ACA) on health insurance deductions. The ACA introduced a new deduction for health insurance premiums for individuals who purchase coverage through a health insurance exchange. This deduction is available to those whose income is between 100% and 400% of the federal poverty level. It is important to note that this deduction is only available for premiums paid for coverage through an exchange, not for coverage provided by an employer or purchased directly from an insurance company.

Furthermore, it is crucial to understand the difference between health insurance premiums and other types of health-related expenses. While premiums are generally not deductible, other medical expenses such as doctor visits, hospital bills, and prescription medications may be deductible if they meet certain criteria. It is important to keep track of all health-related expenses and consult with a tax professional to determine what can be deducted.

In conclusion, while the general rule is that health insurance payments are not tax-deductible as personal expenses, there are exceptions and nuances that can impact your tax situation. It is important to understand these rules and consult with a tax professional to ensure that you are taking advantage of all available deductions and credits.

Does Short-Term Health Insurance Cover Pre-Existing Conditions in Florida?

You may want to see also

Explore related products

![]()

Exceptions: Certain circumstances, like self-employment or specific medical conditions, may allow for deductions

In the realm of tax deductions, the general rule is that premiums paid for health insurance are not deductible. However, there are exceptions to this rule that can provide relief to taxpayers under certain circumstances. One such exception applies to self-employed individuals. If you are self-employed, you may be able to deduct the cost of your health insurance premiums as a business expense. This deduction can be claimed on Schedule C of your tax return, which is used to report income and expenses from a sole proprietorship or single-member LLC.

Another exception to the nondeductibility of health insurance premiums is for individuals with specific medical conditions. If you have a medical condition that requires specialized care or treatment, you may be able to deduct the cost of your health insurance premiums as a medical expense. This deduction can be claimed on Schedule A of your tax return, which is used to report itemized deductions. However, it's important to note that the deduction for medical expenses is subject to a threshold, which means that only expenses that exceed a certain percentage of your adjusted gross income can be deducted.

In addition to these exceptions, there are other circumstances under which the cost of health insurance premiums may be deductible. For example, if you are a member of a health savings account (HSA) or a flexible spending account (FSA), you may be able to deduct the cost of your health insurance premiums as a contribution to these accounts. HSAs and FSAs are tax-advantaged accounts that allow you to save money for qualified medical expenses, including health insurance premiums.

It's important to keep in mind that the rules surrounding the deductibility of health insurance premiums can be complex and may change from year to year. As such, it's always a good idea to consult with a tax professional or refer to the latest tax laws and regulations to ensure that you are taking advantage of all available deductions. By understanding the exceptions to the nondeductibility of health insurance premiums, you can potentially save money on your taxes and make the most of your hard-earned income.

Does Blue Cross Blue Shield Cover Neuro-Ophthalmology Services?

You may want to see also

Explore related products

![]()

Itemized Deductions: Health insurance premiums can be itemized if they exceed a certain percentage of income

In the realm of tax deductions, health insurance premiums hold a unique position. Unlike other medical expenses, premiums can be itemized if they surpass a specific threshold relative to one's income. This provision offers a potential avenue for taxpayers to reduce their taxable income, thereby lowering their overall tax liability. However, it's crucial to understand the intricacies of this deduction to maximize its benefits.

To qualify for this deduction, taxpayers must first determine if their health insurance premiums exceed the designated percentage of their adjusted gross income (AGI). This percentage varies depending on the tax year and filing status. For instance, in recent years, the threshold has been set at 10% of AGI for most taxpayers. Those who are self-employed or have certain types of health coverage may be subject to different thresholds.

Once it's established that the premiums exceed the threshold, taxpayers can proceed to itemize these expenses on Schedule A of their tax return. It's important to note that only the portion of premiums that exceeds the threshold is deductible. For example, if a taxpayer's AGI is $50,000 and the threshold is 10%, they can only deduct premiums that exceed $5,000.

When calculating the deduction, taxpayers should also consider other medical expenses that may be eligible for itemization. The IRS allows taxpayers to deduct qualified medical expenses that exceed 7.5% of their AGI (as of recent tax years). By combining health insurance premiums with other eligible medical expenses, taxpayers may be able to reach the itemization threshold more easily.

To further optimize this deduction, taxpayers should be aware of the potential impact of other tax credits and deductions. For instance, those who are eligible for the Premium Tax Credit (PTC) may need to reconcile this credit with their itemized deduction for health insurance premiums. Additionally, taxpayers should consider the overall tax implications of itemizing versus taking the standard deduction, as itemizing may not always result in a greater tax benefit.

In conclusion, while the deduction for health insurance premiums can be a valuable tax-saving tool, it requires careful consideration and planning to maximize its benefits. Taxpayers should familiarize themselves with the relevant thresholds, calculate their eligible deduction accurately, and weigh the potential benefits against other tax considerations.

Decoding NIB: Understanding What This Health Insurance Acronym Means

You may want to see also

Explore related products

![]()

Tax Credits: Some individuals may qualify for tax credits to offset health insurance costs

Tax credits can be a valuable tool for individuals looking to offset the costs of health insurance. These credits are typically available to those who meet certain income and eligibility requirements, and they can help make health insurance more affordable for those who might otherwise struggle to pay for it.

One of the most well-known tax credits for health insurance is the Premium Tax Credit, which is available through the Affordable Care Act (ACA) marketplace. This credit can help lower the monthly premium cost for individuals and families who purchase health insurance through the marketplace. The amount of the credit is based on income and the cost of health insurance in the area where the individual lives.

Another tax credit that can help with health insurance costs is the Health Savings Account (HSA) tax credit. This credit is available to individuals who have an HSA and who make contributions to it. The credit can help offset the cost of health insurance premiums, as well as other qualified medical expenses.

It's important to note that tax credits for health insurance can change over time, and it's essential to stay up-to-date on the latest information. For example, the ACA marketplace tax credits were expanded in 2021 to provide more assistance to individuals and families. Additionally, some states offer their own tax credits for health insurance, so it's important to check with your state's tax department to see if you qualify for any additional credits.

In conclusion, tax credits can be a helpful way to make health insurance more affordable for individuals and families. By understanding the different types of tax credits available and staying informed about changes to these credits, you can take advantage of these valuable tools to help lower your health insurance costs.

The Rise and Fall of 80s Health Insurance Plans: A Retrospective

You may want to see also

Explore related products

![]()

State Variations: State tax laws may differ, potentially allowing for deductions or credits not available federally

State tax laws exhibit significant diversity, which can impact the taxability of health insurance payments. While federal tax regulations provide a broad framework, individual states have the autonomy to enact their own tax statutes, potentially offering deductions or credits that are not available at the federal level. This variation can lead to complex tax scenarios for individuals and businesses alike.

For instance, some states may allow for the deduction of health insurance premiums from state taxable income, reducing the overall tax burden for residents. Others might offer tax credits for specific types of health insurance plans or for individuals who meet certain criteria, such as low-income thresholds or age requirements. These state-specific provisions can significantly influence the net cost of health insurance for taxpayers.

To navigate these variations effectively, it is crucial for taxpayers to be aware of their state's tax laws regarding health insurance payments. Consulting with a tax professional or utilizing state-specific tax resources can help individuals and businesses optimize their tax strategy and ensure compliance with both federal and state regulations. By understanding and leveraging these state variations, taxpayers may be able to minimize their tax liability and maximize their financial well-being.

In conclusion, the diversity in state tax laws regarding health insurance payments underscores the importance of staying informed about local tax regulations. By doing so, taxpayers can make informed decisions and potentially benefit from deductions or credits that are not available at the federal level. This knowledge can be a valuable asset in managing one's financial affairs and ensuring tax compliance.

Does Private Health Insurance Cover CT Scans? What You Need to Know

You may want to see also

Frequently asked questions

Generally, health insurance premiums paid by an individual are not tax-deductible. However, if you are self-employed, you may be able to deduct the cost of health insurance premiums on your tax return.

There are a few exceptions to this rule. For example, if you are self-employed, you may be able to deduct the cost of health insurance premiums on your tax return. Additionally, if you are enrolled in a Health Savings Account (HSA) or a Flexible Spending Account (FSA), you may be able to deduct the cost of health insurance premiums.

The Affordable Care Act (ACA) does not change the taxability of health insurance payments. However, it does provide for premium tax credits to help make health insurance more affordable for some individuals.

Health insurance payments are generally not considered a business expense. However, if you are self-employed, you may be able to deduct the cost of health insurance premiums on your tax return as a business expense.

Yes, if you are enrolled in a Health Savings Account (HSA) or a Flexible Spending Account (FSA), you may be able to deduct the cost of health insurance premiums. However, it is important to note that there are limits to the amount you can deduct, and you should consult with a tax professional to determine your eligibility.