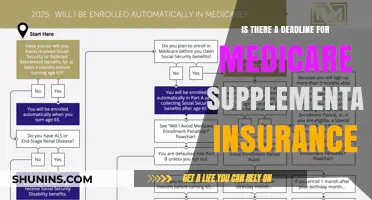

Medicare Supplement Insurance, also known as Medigap, is extra insurance you can purchase from a private company to help pay your share of costs in Original Medicare. Generally, you need Part A and Part B to buy a Medigap policy. With most Medicare Supplement plans, you can visit any doctor or facility that accepts Medicare assignment. However, in some states, insurance companies offer Medicare SELECT, a type of Medicare Supplement plan with a network of hospitals and doctors for non-emergency care. If you enroll in a SELECT plan, you may have to use in-network healthcare providers to receive full insurance benefits. To find a provider that accepts Medicare payments, you can use the Care Compare tool on Medicare.gov or contact your State Health Insurance Assistance Program (SHIP).

| Characteristics | Values |

|---|---|

| Medicare coverage options | Original Medicare, Medicare Advantage |

| Medicare Supplement Insurance | Medigap |

| Medigap policy requirements | Generally, you need Part A and Part B |

| Medigap policy coverage | Coverage when travelling outside the U.S., medically necessary doctor services, preventive services |

| Medigap policy exclusions | Long-term care, vision, dental, hearing aids, private-duty nursing, prescription drugs |

| Medicare Advantage Plans | Include Part D coverage |

| Medicare Supplement Insurance plans | Medicare SELECT |

| Medicare SELECT | A network of hospitals and doctors for non-emergency care |

| Medicare Supplement plans | Plan F, Plan High-Deductible F, and Plan G |

Explore related products

What You'll Learn

![]()

Medicare Supplement Insurance (Medigap)

Medicare Supplement Insurance, also known as Medigap, is extra insurance provided by private companies to help pay for out-of-pocket costs in Original Medicare (Parts A and B). Medigap policies are generally purchased by those who already have Original Medicare and want additional financial assistance for their share of costs. It is important to note that Medigap is not a replacement for Original Medicare but rather a supplement to it.

Medigap policies offer standardised benefits across insurance companies, with price being the primary differentiating factor between policies with the same letter sold by different insurers. These policies typically do not cover long-term care, vision, dental, hearing aids, private-duty nursing, or prescription drugs. However, some Medigap policies provide coverage for travel outside the U.S., which can be beneficial for individuals who frequently travel internationally.

To be eligible to purchase a Medigap policy, you typically need to have both Part A (Hospital Insurance) and Part B (Medical Insurance) of Original Medicare. Part B covers medically necessary doctor services, including outpatient services and certain inpatient hospital doctor services. It also covers most preventive services, with certain preventive services being available at no additional cost if your doctor accepts assignment.

When considering Medigap, it is important to note that, in many cases, you may be restricted to using doctors within the plan's network. This means that your choice of healthcare providers may be limited to those who are part of the Medigap insurer's approved list of healthcare professionals. However, with Original Medicare, you have the flexibility to see any doctor or hospital that accepts Medicare across the United States. Therefore, while Medigap can provide financial assistance, it may also restrict your choice of healthcare providers to some extent.

Teachers' Medical Insurance: What's Covered and What's Not

You may want to see also

Explore related products

![]()

Medicare SELECT

With a Medicare SELECT plan, you may need a referral from your primary care physician before seeking treatment from a specialist. Original Medicare and Medicare Supplement plans do not require referrals.

Health Insurance Denial: Can I Sue for Refused Medication?

You may want to see also

Explore related products

![]()

Doctors who don't accept assignment

Doctors who do not accept assignment are called non-participating providers. They do not accept Medicare's negotiated payments as payment in full for all Medicare services. Instead, they may accept Medicare reimbursement as partial payment, but they might not accept Medicare's approved reimbursement amount as the full payment for their services. They may accept the Medicare-approved amount for services on a case-by-case basis.

If your doctor doesn't accept assignment, you may have to pay the entire bill upfront and seek reimbursement for the portion that Medicare will pay. This could mean that you end up paying more for their services than you would if your doctor accepted assignment. This additional amount can be up to 15% above the amount paid to participating providers by Medicare, and you'll pay this extra fee in addition to your normal deductible and coinsurance.

Opt-out providers are another category of doctors who do not accept Medicare. These doctors may still be willing to see Medicare patients but will expect to be paid their full fee—not the smaller Medicare reimbursement amount. Medicare doesn't pay for any portion of the bills you receive from them.

You can find out if your doctors or other healthcare providers accept assignment or participate in Medicare. Most doctors, providers, and suppliers accept assignment, but it is always good to check. To find a provider that accepts Medicare payments, use the Care Compare tool on Medicare.gov. This tool gives you a list of professionals or group practices in the specialty and geographic area you specify, along with detailed profiles, maps, and driving directions.

Emergency Medical Evacuation Insurance: Is It Tax Deductible?

You may want to see also

Explore related products

![]()

Medicare Part B

Medically necessary services are services or supplies that meet accepted standards of medical practice to diagnose or treat a medical condition. This includes outpatient services and some inpatient hospital doctor services. Preventive services include healthcare to prevent illness (e.g. the flu) or detect it at an early stage when treatment is likely to work best.

If you have Part B, you pay 20% of the Medicare-approved amount for most services after you meet the Part B deductible. You pay nothing for certain preventive services if your doctor or other provider accepts assignment. If you have Part B and Medicare Supplement Insurance (Medigap) that pays your Part B coinsurance, your Medigap plan should cover the cost for insulin.

If you have Original Medicare and want to add drug coverage, you can join a separate Medicare drug plan. Medicare drug coverage is available to everyone with Medicare. Most Medicare Advantage Plans include Part D coverage. In most cases, you can't join a separate Medicare drug plan.

To find a provider that accepts Medicare payments, use the Care Compare tool on Medicare.gov. This tool allows you to specify a specialty and geographic area, and provides detailed profiles, maps, and driving directions.

Medical Insurance and Utility Bills: An Unexpected Comparison

You may want to see also

Explore related products

![]()

Medicare Advantage Plans

When you join a Medicare Advantage Plan, you may have to use doctors who are in the plan's network. This means that your choice of doctors may be limited to those who are contracted with the plan. It's important to review the plan's provider directory to see if your preferred doctors are included.

Before enrolling in a Medicare Advantage Plan, it's important to consider the potential impact on your existing coverage. In some cases, joining a Medicare Advantage Plan might cause you to lose your employer or union coverage, and this could also affect the coverage of your spouse and dependents. Additionally, Medicare Advantage Plans can disenroll you if you move outside the plan's service area or if the plan's contract with Medicare ends, so it's important to review your options regularly.

Medically Needy: Is It a Health Insurance Alternative?

You may want to see also

Frequently asked questions

Medicare Supplement Insurance, also known as Medigap, is extra insurance you can buy from a private company that helps pay your share of costs in Original Medicare.

With most types of Medicare Supplement Insurance plans, you can see the doctor of your choice. However, you may pay more if the doctor does not accept Medicare assignment.

To find a provider that accepts Medicare payments, use the Care Compare tool on Medicare.gov. This tool will give you a list of professionals or group practices in the specialty and geographic area you specify.