Medicare Supplement Insurance, also known as Medigap, is extra insurance that can be purchased from a private health insurance company to help pay for out-of-pocket costs in Original Medicare (Parts A and B). Medigap policies are standardized, with 10 different types of plans offered in most states, named by letters: A-D, F, G, and K-N. The benefits of each lettered plan are the same across insurance companies, with price being the only differentiating factor. Medigap typically covers costs such as copayments, coinsurance, and deductibles, and some plans offer additional benefits like foreign travel emergency services. While Medigap does not have network limitations, enrolling in a Medicare Advantage Plan may restrict you to doctors within the plan's network.

| Characteristics | Values |

|---|---|

| What is Medicare Supplemental Insurance (Medigap)? | Extra insurance to help pay your share of out-of-pocket costs in Original Medicare |

| When can you buy it? | During your Medicare Supplement Open Enrollment period, which is a one-time, 6-month period starting the first month you have Medicare Part B and are 65 or older. |

| What does it cover? | Copayments, coinsurance, deductibles, and some services that Original Medicare doesn't cover, such as emergency medical care when travelling outside the US. |

| What doesn't it cover? | Dental care, vision care, hearing aids, medications, long-term care, private-duty nursing, and prescription drugs. |

| Where is it accepted? | Medigap coverage is generally available anywhere that Medicare is accepted, including outside the US. |

| How much does it cost? | The more comprehensive the coverage, the higher the premium. Premiums vary by insurance company and can change yearly. |

Explore related products

![LLC Beginner's Guide [All-in-1]: Everything on How to Start, Run, and Grow Your First Company Without Prior Experience. Includes Essential Tax Hacks, Critical Legal Strategies, and Expert Insights](https://m.media-amazon.com/images/I/61SXdyvdqKL._AC_UY218_.jpg)

What You'll Learn

![]()

Medigap policies and their benefits

Medicare Supplement Insurance, also known as Medigap, is an extra insurance policy that can be purchased from a private insurance company. It helps cover the out-of-pocket costs associated with Original Medicare (Parts A and B), such as premiums, deductibles, coinsurance, and copayments. These out-of-pocket costs are sometimes referred to as the "'gaps'" in Medicare coverage, and Medigap helps to pay for those gaps. It is important to note that Medigap is different from Medicare Advantage (Part C), which is an alternative way to receive Medicare benefits. Medigap can only be used with Original Medicare.

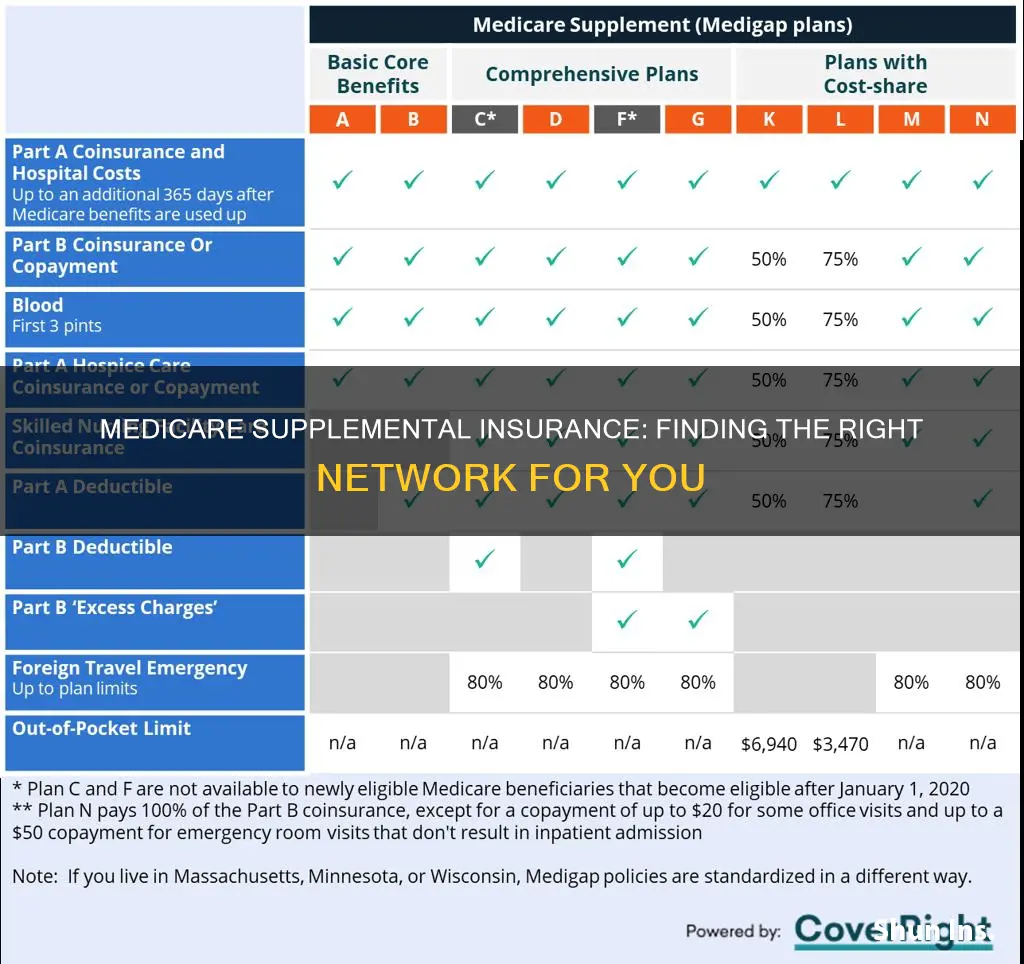

There are 10 different types of Medigap plans offered in most states, and they are named by letters: A-D, F, G, and K-N. The benefits offered by each lettered plan are standardized, meaning that the same basic benefits are provided no matter which insurance company sells the policy or where you live. The price is the only difference between plans with the same letter sold by different companies. Some Medigap policies also offer coverage for additional benefits that are not covered by Original Medicare, such as certain vision, hearing, and dental services. Additionally, some Medigap policies offer coverage when travelling outside the United States.

It is important to note that Medigap policies generally do not cover long-term care, such as care in a nursing home, vision, dental, hearing aids, private-duty nursing, or prescription drugs. Individuals under the age of 65 may face difficulties in purchasing a Medigap policy or may have to pay higher prices. The ideal time to buy a Medigap policy is during the Medigap Open Enrollment Period, which is a six-month window that starts when an individual first enrols in Medicare Part B and is 65 or older. During this period, individuals can enrol in any Medigap policy available in their state, and insurance companies cannot deny coverage due to pre-existing health conditions. After this period, purchasing a Medigap policy may become more challenging or expensive.

Accident Insurance: What Counts as an Accident?

You may want to see also

Explore related products

![]()

Medigap and foreign travel

Medicare Supplement Insurance, also known as Medigap, is an extra insurance policy that can be purchased from a private company. It helps to cover out-of-pocket costs for services covered by Original Medicare (Part A and Part B). Medigap policies are standardised, with 10 different types of plans offered in most states, named by letters like Plan G or Plan K. The benefits offered by each lettered plan are the same across insurance companies, with price being the only differentiating factor.

Medigap plans can be beneficial for those who travel frequently, as some policies provide coverage for foreign travel emergency care. This coverage typically includes emergency health care services received outside of the United States during the first 60 days of a trip. However, it's important to note that Medigap plans usually cover only 80% of billed charges for medically necessary emergency care, and there may be a deductible amount that must be paid first. Additionally, Medigap's foreign travel emergency coverage has a lifetime limit of $50,000.

For those considering foreign travel, it is essential to carefully review the specific details of their Medigap plan. While some plans may provide coverage for emergency health care services abroad, it is limited, and there may be deductibles, copayments, and coinsurance requirements. It is also worth noting that Medicare generally does not cover medical services outside of the United States and its territories, except in rare circumstances. Therefore, travellers are advised to research their options and consider purchasing travel insurance, which can provide coverage for emergency medical care and medical evacuation in foreign countries.

Medigap plans C, D, F, G, M, and N are known to cover emergency healthcare while travelling outside of the country. However, it is important to note that plans C and F are no longer available to new Medicare beneficiaries; only those eligible for Medicare before 2020 can enrol in these plans. As of 2022, some private Medicare Advantage plans also offer coverage for foreign travel emergency care, but the details of this coverage may vary. Travellers can use the Medicare Plan Finder to explore the specific options available in their area.

Supplemental Medical Insurance: Fluctuating Rates Twice Yearly

You may want to see also

Explore related products

![Medicare and Social Security: [5 in 1] Maximize Your Retirement Benefits, Secure Medical Coverage and Quality Healthcare | Proven Strategies to Protect Your Financial Future Avoiding Costly Mistakes](https://m.media-amazon.com/images/I/71sRJGiWeQL._AC_UL320_.jpg)

![]()

Medicare Supplement Insurance plans

Medicare Supplement Insurance, also known as Medigap, is an additional insurance policy that can be purchased from a private health insurance company. It helps cover the out-of-pocket costs associated with Original Medicare (Parts A and B), such as coinsurance, copayments, and deductibles. Generally, individuals must already have Original Medicare, be over 65, and in some states prove disability or End-Stage Renal Disease to be eligible for a Medigap policy.

There are 10 types of Medigap plans offered in most states, named by letters: A-D, F, G, and K-N. The benefits offered by each lettered plan are standardised and remain the same across different insurance companies. The price is the only differentiating factor between policies with the same letter sold by different companies. Plans A through G generally provide benefits at higher premiums with limited out-of-pocket costs compared to Plans K through N. Plans K through N are cost-sharing plans offering similar benefits at lower premiums but with higher out-of-pocket expenses.

Some Medigap policies also cover extra benefits that Original Medicare does not, such as certain vision, hearing, and dental services. Additionally, some policies offer coverage when travelling outside the US. However, long-term care, such as nursing home stays, private-duty nursing, and prescription drugs, are typically not covered by Medigap policies.

Medigap policies can be purchased during the "Medigap Open Enrollment" period, which lasts for 6 months and begins the first month an individual has Medicare Part B and is 65 or older. During this time, insurance companies cannot deny coverage due to pre-existing health conditions. After this period, purchasing a Medigap policy may be more difficult or expensive.

Health Insurance: Medical Records or Confidential Information?

You may want to see also

Explore related products

![]()

Medicare Advantage and Prescription Drug Plans

There are two main ways to get Medicare coverage: Original Medicare and Medicare Advantage. Original Medicare does not offer drug coverage, so you may need to consider a Medicare Advantage plan or a standalone prescription drug plan.

Medicare Advantage Plans

Medicare Advantage is an alternative to Original Medicare for your health and drug coverage. In many cases, you can only use doctors who are in the plan's network. Medicare Advantage Plans may also be bundled with Medicare prescription drug coverage, known as MAPD.

Prescription Drug Plans

Medicare prescription drug coverage is also known as Part D. Part D is private insurance that covers most prescription drugs. You can add a standalone Part D plan, also called a PDP, to Original Medicare or a Medicare Advantage plan without drug coverage. Part D plans generally don't cover drugs prescribed for anorexia, weight loss or gain, fertility, erectile dysfunction, cosmetic purposes, or hair growth.

Standalone Part D plans charge a monthly premium and may also have an annual deductible, copays, and coinsurance. When you fill a prescription for a covered drug, you will usually need to pay a copayment (a set amount) or coinsurance (a percentage). Your costs may be lower if you qualify for the Extra Help program.

Medicare Supplement Insurance (Medigap)

Medigap is extra insurance you can buy from a private company to help pay your share of out-of-pocket costs in Original Medicare. Medigap policies do not generally cover prescription drugs, but some offer coverage when you travel outside the U.S.

Get Medical Insurance in Virginia: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Medicare Supplement Insurance and Original Medicare

Medicare Supplement Insurance, also known as Medigap, is extra insurance that can be purchased from a private health insurance company. This insurance helps pay for out-of-pocket costs in Original Medicare. Original Medicare, also known as fee-for-service Medicare, is a program that offers health coverage for seniors and disabled individuals. It is available to everyone 65 or older and those with specific disabilities or end-stage renal disease. Original Medicare is administered by the federal government and provides coverage for a wide range of health services, including hospital stays, doctor visits, and more.

Medigap policies help cover the gaps in Original Medicare by paying for some of the out-of-pocket costs, such as copayments, coinsurance, and deductibles. Generally, you need to have both Part A (hospital insurance) and Part B (medical insurance) of Original Medicare to buy a Medigap policy. Medigap policies are standardized, meaning that policies with the same letter offer the same basic benefits regardless of the insurance company or location. However, the price may vary between insurance companies offering the same policy.

There are 10 different types of Medigap plans offered in most states, labelled from A-D, F, G, and K-N. Some Medigap policies also offer additional benefits not covered by Original Medicare, such as coverage when travelling outside the US. It is important to note that Medigap policies typically do not cover long-term care, vision, dental, hearing aids, private nursing, or prescription drugs. Additionally, if you are under 65, you may face challenges in purchasing a Medigap policy or may have to pay higher premiums.

When considering Medicare options, individuals have a choice between Original Medicare and Medicare Advantage. Medicare Advantage Plans are offered by private companies that contract with Medicare to provide Part A and Part B benefits. These plans often include additional benefits that Original Medicare does not cover, such as prescription drug coverage. However, with Original Medicare, individuals have the freedom to choose any doctor or hospital that accepts Medicare, anywhere in the United States, without being restricted to a specific network.

Insurance: Accidents, Tickets, and When They're Forgotten

You may want to see also

Frequently asked questions

Medicare Supplement Insurance, also known as Medigap, is extra insurance that helps pay your share of out-of-pocket costs in Original Medicare (Parts A and B).

Medicare Supplement Insurance covers copayments, coinsurance, and deductibles. Some policies also cover emergency medical care when travelling outside the US and foreign travel emergency services.

Medicare Supplement Insurance is not required, but it can help cover out-of-pocket costs that Original Medicare doesn't pay for, such as about 20% in out-of-pocket expenses not paid by Medicare Part B for doctor and outpatient medical expenses.

You can buy Medicare Supplement Insurance from a private insurance company. You generally need to have Original Medicare (Parts A and B) before you can buy a Medigap policy.

The best time to enroll is during your Medicare Supplement Open Enrollment period, which starts when you turn 65 and enroll in Medicare Part B. During this time, your acceptance is guaranteed, and you can enroll in any Medigap policy.

![The Medicare Bible for Beginners: [3 in 1] Unlock Medical Benefits and Quality Healthcare | Super Easy Insider Strategies to Navigate Medicare While Avoiding Costly Mistakes](https://m.media-amazon.com/images/I/71tm-tSiWnL._AC_UL320_.jpg)