When it comes to health insurance, one common question that arises is whether there's a rating system in place to evaluate the quality and performance of insurance providers. This is an important consideration for consumers who want to make informed decisions about their healthcare coverage. While there isn't a single, universally recognized rating system for health insurance companies, there are several organizations and agencies that provide ratings and reviews based on various criteria such as customer satisfaction, financial stability, and the comprehensiveness of coverage options. These ratings can be valuable tools for comparing different insurance plans and providers, helping individuals and families choose the best option for their needs and budget.

Explore related products

What You'll Learn

- Types of Health Insurance Ratings: Understand the different rating systems used by various agencies

- How Ratings Impact Premiums: Explore the relationship between insurance ratings and premium costs?

- Top-Rated Health Insurers: Identify the highest-rated health insurance companies according to recent data

- Factors Influencing Ratings: Learn about the criteria that rating agencies consider when evaluating insurers

- Consumer Reviews vs. Professional Ratings: Compare consumer satisfaction reviews with professional rating scores

![]()

Types of Health Insurance Ratings: Understand the different rating systems used by various agencies

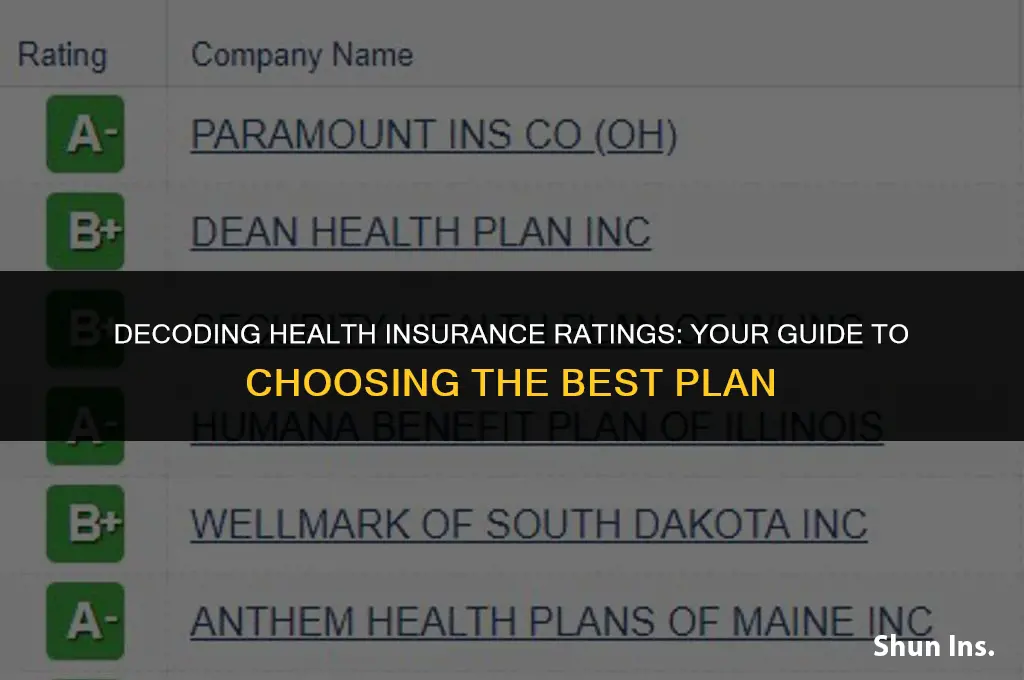

Health insurance ratings are a critical tool for consumers and businesses alike, providing an assessment of the financial stability and performance of insurance companies. These ratings are typically assigned by independent rating agencies, which evaluate insurers based on various criteria such as their ability to pay claims, financial strength, and overall management quality. Understanding the different rating systems used by these agencies can help policyholders make informed decisions about their health insurance coverage.

One of the most well-known rating agencies is A.M. Best, which uses a letter-grade system ranging from A++ to F to rate insurers. Another major player is Moody's, which employs a similar letter-grade system but also includes numerical ratings. Standard & Poor's (S&P) is another prominent rating agency that uses both letter grades and credit ratings to assess insurers' financial health. Each agency has its own unique methodology and criteria for assigning ratings, so it's important to understand the specific system used by the agency you're referencing.

In addition to these major agencies, there are also smaller, regional rating agencies that focus on specific geographic areas or types of insurance. For example, Weiss Ratings is a smaller agency that provides ratings for insurance companies, banks, and other financial institutions. It's important to note that not all rating agencies are created equal, and some may have a better reputation or track record than others.

When evaluating health insurance ratings, it's crucial to consider the agency's methodology, the specific rating criteria used, and the overall reputation of the agency. By understanding these factors, consumers can make more informed decisions about their health insurance coverage and ensure they're choosing a plan from a financially stable and reliable insurer.

Wake Forest Baptist: Accepted Health Insurance Plans

You may want to see also

Explore related products

![]()

How Ratings Impact Premiums: Explore the relationship between insurance ratings and premium costs

Insurance ratings play a crucial role in determining the cost of premiums. These ratings are typically assigned by independent agencies that evaluate an insurance company's financial strength, claims-paying ability, and overall performance. The higher the rating, the more likely the insurer is to offer competitive premiums. Conversely, lower ratings may indicate a higher risk for the insurer, leading to increased premium costs for policyholders.

The relationship between ratings and premiums is complex and multifaceted. For instance, a high rating may not always guarantee the lowest premiums, as other factors such as the type of coverage, the insured's risk profile, and market conditions also influence pricing. However, generally speaking, insurers with higher ratings tend to have more negotiating power and can offer more attractive rates to attract and retain customers.

Policyholders can benefit from understanding this relationship by shopping around for insurance providers with strong ratings. By choosing an insurer with a high rating, they may be able to secure better coverage at a lower cost. Additionally, maintaining a good credit score and a safe driving record can also help policyholders qualify for lower premiums, as these factors are often used by insurers to assess risk and determine pricing.

In conclusion, the relationship between insurance ratings and premium costs is an important consideration for policyholders. By understanding how ratings impact premiums, individuals can make informed decisions when selecting an insurance provider and may be able to secure better coverage at a more affordable price.

Does Health Insurance Cover Motocross Accidents? What Riders Need to Know

You may want to see also

Explore related products

![]()

Top-Rated Health Insurers: Identify the highest-rated health insurance companies according to recent data

Recent data from reputable sources such as the National Committee for Quality Assurance (NCQA) and consumer reviews highlight several top-rated health insurance companies. These insurers are recognized for their comprehensive coverage, customer satisfaction, and robust provider networks. Among the highest-rated are Blue Cross Blue Shield (BCBS), Kaiser Permanente, and UnitedHealthcare. BCBS is noted for its extensive network and high customer satisfaction scores, while Kaiser Permanente excels in preventive care and overall member experience. UnitedHealthcare stands out for its diverse plan offerings and strong financial stability.

To identify these top-rated insurers, one can refer to the latest ratings from organizations like the NCQA, which evaluates health plans based on various criteria including clinical quality, member satisfaction, and administrative performance. Additionally, consumer review platforms such as Yelp and Google Reviews provide valuable insights into policyholders' experiences with different insurers. By cross-referencing these sources, individuals can make informed decisions when selecting a health insurance provider.

When evaluating health insurance companies, it's essential to consider factors beyond just ratings. These include the specific coverage options available, the cost of premiums and out-of-pocket expenses, and the insurer's reputation for handling claims efficiently. Furthermore, individuals should assess whether the insurer offers additional benefits such as wellness programs, telemedicine services, and prescription drug coverage that align with their personal health needs.

In conclusion, while ratings from authoritative sources and consumer reviews can guide the selection process, it's crucial to conduct thorough research and compare multiple insurers to find the best fit. This involves reviewing detailed plan information, consulting with healthcare providers, and considering long-term financial implications. By taking a comprehensive approach, individuals can secure health insurance that not only meets their immediate needs but also provides lasting value and peace of mind.

Understanding Health Insurance Income: Pre-Tax or Post-Tax?

You may want to see also

Explore related products

![Best'S Key Ratings of All Licensed Joint-Stock Fire Insurance Companies 1912 [Leather Bound]](https://m.media-amazon.com/images/I/617DLHXyzlL._AC_UY218_.jpg)

![]()

Factors Influencing Ratings: Learn about the criteria that rating agencies consider when evaluating insurers

Rating agencies play a crucial role in the insurance industry by evaluating insurers' financial strength and ability to meet their obligations. When assessing health insurers, these agencies consider several key factors that influence the ratings assigned. Understanding these criteria can help consumers make informed decisions when choosing a health insurance provider.

One of the primary factors influencing ratings is the insurer's financial stability. Rating agencies analyze the company's capital adequacy, liquidity, and investment portfolio to determine its ability to pay claims and meet financial obligations. Insurers with strong financial reserves and a diversified investment strategy are more likely to receive higher ratings.

Another important factor is the insurer's operational efficiency and effectiveness. Rating agencies evaluate the company's underwriting practices, claims handling processes, and customer service quality. Insurers that demonstrate efficient operations, accurate underwriting, and prompt claims processing are viewed favorably by rating agencies.

Risk management practices are also closely scrutinized. Rating agencies assess the insurer's ability to identify, mitigate, and manage various risks, including underwriting risks, investment risks, and operational risks. Insurers that implement robust risk management strategies and maintain a strong risk governance framework are more likely to receive positive ratings.

Additionally, rating agencies consider the insurer's market position and competitive landscape. Factors such as market share, growth prospects, and competitive advantages are taken into account. Insurers with a strong market presence and a clear competitive strategy are often viewed as more stable and reliable.

Lastly, regulatory compliance and governance are critical factors influencing ratings. Rating agencies evaluate the insurer's adherence to regulatory requirements, corporate governance practices, and transparency in financial reporting. Insurers that maintain high standards of compliance and governance are more likely to receive favorable ratings.

In conclusion, rating agencies consider a range of factors when evaluating health insurers, including financial stability, operational efficiency, risk management practices, market position, and regulatory compliance. By understanding these criteria, consumers can make more informed decisions when selecting a health insurance provider.

Summit Medical Group: Insurance Coverage and Acceptance Details

You may want to see also

Explore related products

![]()

Consumer Reviews vs. Professional Ratings: Compare consumer satisfaction reviews with professional rating scores

Consumer reviews and professional ratings serve as two distinct lenses through which individuals can evaluate health insurance options. Consumer reviews, typically found on online platforms and forums, offer firsthand accounts of policyholders' experiences with their insurance providers. These reviews can provide valuable insights into the customer service quality, claims processing efficiency, and overall satisfaction of current or former policyholders. However, it's essential to approach these reviews with a critical eye, as they may be influenced by individual biases or isolated incidents.

On the other hand, professional ratings are issued by established rating agencies such as A.M. Best, Moody's, and Standard & Poor's. These agencies assess insurance companies based on their financial stability, ability to meet policyholder obligations, and overall business practices. Professional ratings are often presented on a letter-grade scale, with higher grades indicating greater financial strength and reliability. While these ratings can be a useful indicator of an insurer's credibility, they may not directly reflect the day-to-day experiences of policyholders.

When comparing consumer reviews with professional ratings, it's important to consider the different perspectives each offers. Consumer reviews can provide a more nuanced understanding of the policyholder experience, highlighting specific strengths and weaknesses of an insurance provider. In contrast, professional ratings offer a broader assessment of an insurer's financial health and long-term viability. By examining both consumer reviews and professional ratings, individuals can gain a more comprehensive understanding of their health insurance options and make more informed decisions.

One potential pitfall to avoid is relying too heavily on either consumer reviews or professional ratings in isolation. While consumer reviews can be illuminating, they may not always be representative of the overall policyholder experience. Similarly, professional ratings can provide a useful snapshot of an insurer's financial stability, but they may not capture the nuances of customer service or claims processing. By considering both types of information in tandem, individuals can mitigate the risks associated with relying on a single source of evaluation.

Ultimately, the most effective approach to evaluating health insurance options is to combine consumer reviews and professional ratings with other sources of information, such as policy details, premium costs, and coverage options. By taking a multifaceted approach, individuals can make more informed decisions that align with their unique needs and priorities.

Who Represents Me? Finding Legal Help Against Insurance Companies

You may want to see also

Frequently asked questions

Yes, there are several rating systems for health insurance providers. These ratings are typically based on factors such as customer satisfaction, claims processing, and the financial stability of the insurance company.

You can find health insurance ratings through various sources, including consumer advocacy groups, insurance regulatory agencies, and independent rating organizations. Some popular sources include the Better Business Bureau, A.M. Best, and Moody's.

When choosing a health insurance provider based on ratings, consider the following factors: the overall rating of the company, the rating for customer service, the ease of claims processing, and the financial stability of the provider. Additionally, look for any complaints or reviews from current or past policyholders to get a more comprehensive understanding of the company's performance.