The question of whether there is a tax liability for domestic partner health insurance is an important one, especially given the evolving landscape of healthcare and tax laws. In many countries, health insurance provided to domestic partners may be subject to taxation, depending on the specific circumstances and the tax code in place. This tax liability can arise from the employer's contribution to the health insurance plan, the employee's contribution, or the total value of the health insurance coverage provided. Understanding the tax implications of domestic partner health insurance is crucial for both employers and employees to ensure compliance with tax regulations and to make informed decisions about health insurance coverage.

Explore related products

What You'll Learn

- Tax Code Provisions: Specific sections of the tax code addressing health insurance for domestic partners

- Employer-Provided Benefits: Rules for employer-sponsored health insurance plans covering domestic partners

- Individual Tax Implications: How domestic partners report health insurance premiums and benefits on individual tax returns

- State vs. Federal Regulations: Differences in state and federal tax laws regarding domestic partner health benefits

- Recent Legal Changes: Updates or amendments to tax laws affecting health insurance for domestic partners

![]()

Tax Code Provisions: Specific sections of the tax code addressing health insurance for domestic partners

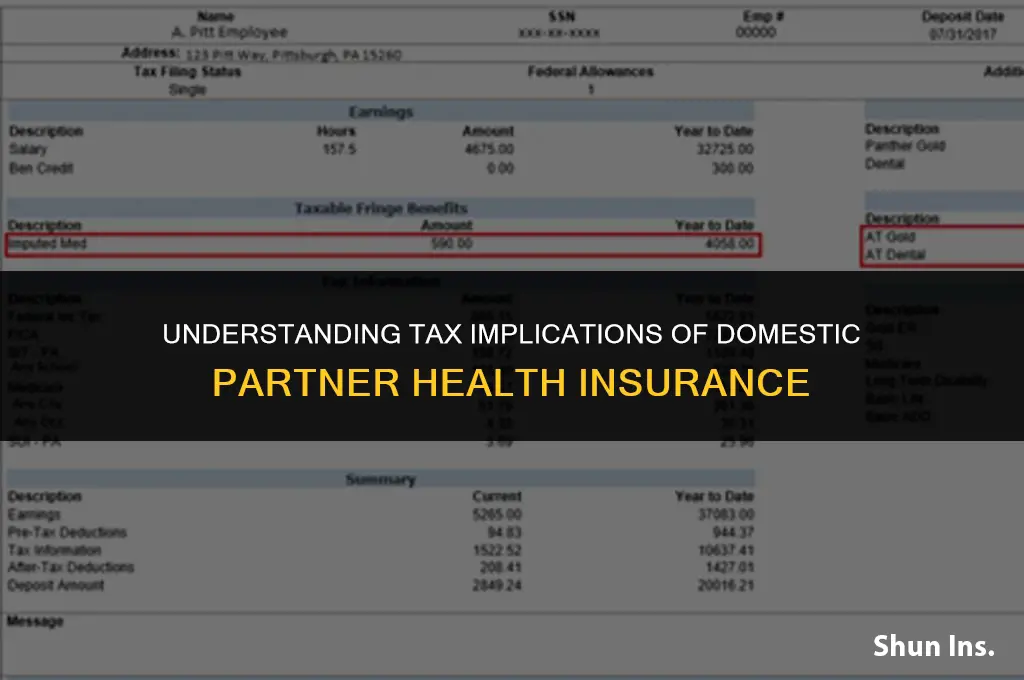

The tax code contains specific provisions that address health insurance for domestic partners. One key section is Internal Revenue Code (IRC) Section 106, which generally excludes employer-provided health insurance from an employee's gross income. This exclusion applies to health insurance provided to both spouses and domestic partners, as long as certain conditions are met.

Another important provision is IRC Section 6051, which requires employers to report the value of employer-provided health insurance on an employee's Form W-2. This reporting requirement applies to health insurance provided to domestic partners as well as spouses.

In addition to these general provisions, there are specific rules that apply to domestic partners. For example, IRC Section 104(a)(3) provides that amounts paid by an employer for health insurance for a domestic partner are not deductible as medical expenses by the employee. This is because such amounts are already excluded from the employee's gross income under IRC Section 106.

Furthermore, IRC Section 7701(a)(19) defines a domestic partner as an individual who is in a committed relationship with the employee and is recognized as such by the employer. This definition is important for determining who qualifies as a domestic partner for tax purposes.

Overall, these tax code provisions provide a framework for understanding the tax implications of employer-provided health insurance for domestic partners. While the general rules are similar to those that apply to spouses, there are some key differences that employers and employees should be aware of.

Can I Claim Myself as a Dependent for Health Insurance?

You may want to see also

Explore related products

![]()

Employer-Provided Benefits: Rules for employer-sponsored health insurance plans covering domestic partners

Employer-sponsored health insurance plans that cover domestic partners must adhere to specific rules and regulations. One key aspect is the tax implications for both the employer and the domestic partner. Generally, employer-provided health insurance is considered a tax-free benefit for the employee, but when it comes to domestic partners, the situation can be more complex.

The IRS has specific guidelines regarding the tax treatment of employer-provided health insurance for domestic partners. If the domestic partner is considered a dependent under IRS rules, the benefit may be tax-free. However, if the domestic partner is not a dependent, the employer may need to report the value of the health insurance as taxable income to the employee. This can have significant implications for both the employer and the employee, as it may increase the employee's taxable income and potentially lead to higher tax liabilities.

To navigate these complexities, employers should carefully review the IRS guidelines and consult with a tax professional to ensure compliance. They should also communicate clearly with their employees about the tax implications of domestic partner health insurance coverage. Employees, on the other hand, should be aware of the potential tax consequences and plan accordingly.

In addition to tax implications, employers should also consider the legal requirements for domestic partner health insurance coverage. Some states have specific laws or regulations that govern the provision of health insurance to domestic partners. Employers should be aware of these laws and ensure that their health insurance plans comply with all applicable legal requirements.

Overall, employer-provided health insurance for domestic partners can be a valuable benefit, but it is important for both employers and employees to understand the tax and legal implications. By doing so, they can make informed decisions and avoid potential pitfalls.

Umbrella Insurance: Medical Malpractice Coverage Explained

You may want to see also

Explore related products

![]()

Individual Tax Implications: How domestic partners report health insurance premiums and benefits on individual tax returns

Domestic partners face unique challenges when it comes to reporting health insurance premiums and benefits on their individual tax returns. Unlike married couples, who can often consolidate their health insurance and tax filings, domestic partners must navigate a more complex landscape. This section will provide a detailed overview of the individual tax implications for domestic partners, focusing on how to accurately report health insurance premiums and benefits to avoid potential tax liabilities.

One of the key considerations for domestic partners is determining who can claim the health insurance premiums as a deduction. Generally, the individual who pays the premiums and is also the policyholder or subscriber is eligible to deduct these expenses. However, if both partners contribute to the premiums, they may need to allocate the deduction proportionally based on their contributions. It's important to keep accurate records of premium payments and to communicate with your tax preparer or accountant to ensure proper documentation and reporting.

Another important aspect to consider is the tax treatment of health insurance benefits received by domestic partners. If one partner receives health insurance coverage through their employer, the premiums paid by the employer are generally not taxable to the employee. However, if the other partner is covered under the same policy and is not an employee, the portion of the premiums paid by the employer on their behalf may be considered taxable income. This can be a complex area, and it's advisable to consult with a tax professional to understand the specific implications for your situation.

Domestic partners should also be aware of the potential tax implications of health savings accounts (HSAs) and flexible spending accounts (FSAs). Contributions to these accounts can provide tax benefits, but the rules can be different for domestic partners compared to married couples. For example, if one partner has an HSA or FSA through their employer, the other partner may not be eligible to contribute to the same account. Understanding these nuances can help domestic partners maximize their tax savings while avoiding potential penalties.

In conclusion, navigating the individual tax implications of health insurance for domestic partners requires careful attention to detail and an understanding of the complex rules and regulations. By keeping accurate records, communicating with tax professionals, and staying informed about the latest tax laws, domestic partners can minimize their tax liabilities and ensure compliance with IRS requirements.

Will Your Insurance Company Offer a Settlement? Key Factors Explained

You may want to see also

Explore related products

![]()

State vs. Federal Regulations: Differences in state and federal tax laws regarding domestic partner health benefits

The landscape of tax laws regarding domestic partner health benefits is complex and varies significantly between state and federal regulations. While federal law generally does not recognize domestic partnerships for tax purposes, many states have enacted their own laws to provide certain benefits and protections to domestic partners. This discrepancy can lead to confusion and potential tax liabilities for employers and employees alike.

Under federal law, health benefits provided to domestic partners are typically considered taxable income to the employee. This is because the Internal Revenue Service (IRS) does not recognize domestic partnerships as legal entities for tax purposes. As a result, employers may be required to report the value of these benefits on the employee's Form W-2, and the employee may need to pay taxes on this additional income.

In contrast, some states have enacted laws that provide tax benefits for domestic partners. For example, California, New York, and Massachusetts all have state tax laws that recognize domestic partnerships and provide certain tax benefits, such as the ability to file joint state tax returns and access to state health insurance programs. These state laws can create a patchwork of regulations that employers must navigate when providing health benefits to domestic partners.

Employers operating in multiple states may face additional challenges, as they must comply with the varying tax laws of each state. This can lead to complex administrative tasks and potential tax liabilities if not managed properly. To mitigate these risks, employers should consult with tax professionals and ensure that their benefit plans are designed to comply with both federal and state tax laws.

Employees who receive health benefits from their domestic partner's employer should also be aware of the potential tax implications. They may need to report these benefits as taxable income on their federal tax return, even if they are not subject to state tax. Additionally, employees should be aware of any state-specific tax benefits or protections that may be available to them.

In conclusion, the differences between state and federal tax laws regarding domestic partner health benefits can create a complex and challenging environment for both employers and employees. Understanding these differences and taking appropriate steps to comply with the relevant tax laws is essential to avoid potential tax liabilities and ensure that all parties are properly protected.

Understanding Blue Plus Insurance: Medicaid or Medicare?

You may want to see also

Explore related products

![TurboTax Deluxe Desktop Edition 2025, Federal & State Tax Return [Win11/Mac14 Download]](https://m.media-amazon.com/images/I/71OcM906MLL._AC_UL320_.jpg)

$55.99 $79.99

![H&R Block Tax Software Deluxe + State 2025 Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/611uM-FzipL._AC_UL320_.jpg)

![TurboTax Premier Desktop Edition 2025, Federal & State Tax Return [Win11/Mac14 Download]](https://m.media-amazon.com/images/I/71ofxs16-9L._AC_UL320_.jpg)

$82.99 $114.99

![TurboTax Home & Business Desktop Edition 2025, Federal & State Tax Return [Win11/Mac14 Download]](https://m.media-amazon.com/images/I/71-jbdrZxVL._AC_UL320_.jpg)

![]()

Recent Legal Changes: Updates or amendments to tax laws affecting health insurance for domestic partners

Recent legal changes have significantly impacted the tax implications of health insurance for domestic partners. The Tax Cuts and Jobs Act of 2017, for instance, introduced substantial amendments to the tax code that affect how health insurance benefits are taxed for domestic partners. Prior to this act, the IRS considered health insurance premiums paid by an employer for a domestic partner as taxable income to the employee. However, the new law has altered this perspective, providing more favorable tax treatment in certain circumstances.

One key change is the elimination of the Affordable Care Act's individual mandate penalty. This penalty, which was imposed on individuals who failed to maintain minimum essential health coverage, was often a point of contention for domestic partners who were not legally married but still wished to obtain health insurance together. The removal of this penalty has made it easier for domestic partners to navigate the health insurance landscape without fear of additional tax liabilities.

Another important update is the clarification of the tax treatment of health savings accounts (HSAs) and flexible spending accounts (FSAs) for domestic partners. The IRS has issued guidance stating that domestic partners can contribute to HSAs and FSAs on a pre-tax basis, provided that they meet certain eligibility requirements. This change has made it more advantageous for domestic partners to utilize these tax-saving vehicles for their health care expenses.

Furthermore, some states have taken steps to provide additional tax relief for domestic partners. For example, California has enacted legislation that allows domestic partners to file state tax returns jointly, which can result in lower overall tax liability. Other states have implemented similar measures, recognizing the importance of providing equitable tax treatment for all families, regardless of marital status.

In conclusion, the recent legal changes have brought about significant updates to the tax laws affecting health insurance for domestic partners. These changes have generally aimed to provide more favorable tax treatment and greater flexibility for domestic partners in managing their health care expenses. As the legal landscape continues to evolve, it is crucial for domestic partners to stay informed about these developments and consult with a tax professional to ensure they are taking full advantage of the available tax benefits.

Weigand Properties Wichita KS: Unveiling Their Trusted Insurance Provider

You may want to see also

Frequently asked questions

Yes, there can be tax implications for domestic partner health insurance. If your employer provides health insurance for your domestic partner, the value of this benefit may be considered taxable income to you. This is because the IRS views health insurance premiums paid by an employer for an employee's domestic partner as a form of compensation.

The tax liability for domestic partner health insurance is typically calculated based on the fair market value of the health insurance premiums paid by your employer. This value is added to your taxable income and subject to federal, state, and local income taxes. You may need to provide documentation to your employer about your domestic partnership to ensure accurate tax reporting.

There are some exceptions and special rules to consider. For example, if you and your domestic partner are both covered under the same health insurance plan, the tax liability may be split between you. Additionally, some states have specific laws or regulations regarding domestic partner health insurance that may affect tax liability. It's important to consult with a tax professional or your employer's HR department to understand how these rules apply to your situation.

![TurboTax Deluxe Desktop Edition 2025, Federal Tax Return [Win11/Mac14 Download]](https://m.media-amazon.com/images/I/71pX8Fh2sNL._AC_UL320_.jpg)

![TurboTax Business Desktop Edition 2025, Federal Tax Return [Win11 Download]](https://m.media-amazon.com/images/I/71iKclcd6ML._AC_UL320_.jpg)

![H&R Block Tax Software Premium 2025 Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51dMIAMHkkL._AC_UL320_.jpg)

![H&R Block Tax Software Deluxe 2025 Win/Mac [PC/Mac Online Code]](https://m.media-amazon.com/images/I/51Mlng5FWYL._AC_UL320_.jpg)

![H&R Block Tax Software Premium & Business 2025 Win [PC Online code]](https://m.media-amazon.com/images/I/618kxmZlTGL._AC_UL320_.jpg)

![[OLD VERSION] TurboTax Deluxe 2024 Tax Software, Federal & State Tax Return [PC/MAC Download]](https://m.media-amazon.com/images/I/71UbHaUeeUL._AC_UL320_.jpg)