Health Savings Accounts (HSAs) are a popular tax-advantaged savings option for individuals with high-deductible health plans (HDHPs). However, there are certain eligibility requirements that must be met in order to qualify for an HSA. One common question is whether there is an income limit for having an HSA. The short answer is no; there is no income limit for HSA eligibility. As long as you have an HDHP and are not enrolled in Medicare, you can contribute to an HSA regardless of your income level. This makes HSAs an attractive option for people of all income brackets who want to save money on healthcare expenses.

Explore related products

What You'll Learn

- Eligibility Criteria: Understand the income thresholds set by IRS for HSA eligibility

- Contribution Limits: Explore the maximum annual contributions allowed for HSA accounts

- Tax Implications: Learn about the tax benefits and potential penalties related to HSA contributions

- Withdrawal Rules: Discover the conditions under which HSA funds can be withdrawn tax-free

- Comparison with Other Plans: Evaluate how HSAs differ from other health savings options like FSAs and HRAs

![]()

Eligibility Criteria: Understand the income thresholds set by IRS for HSA eligibility

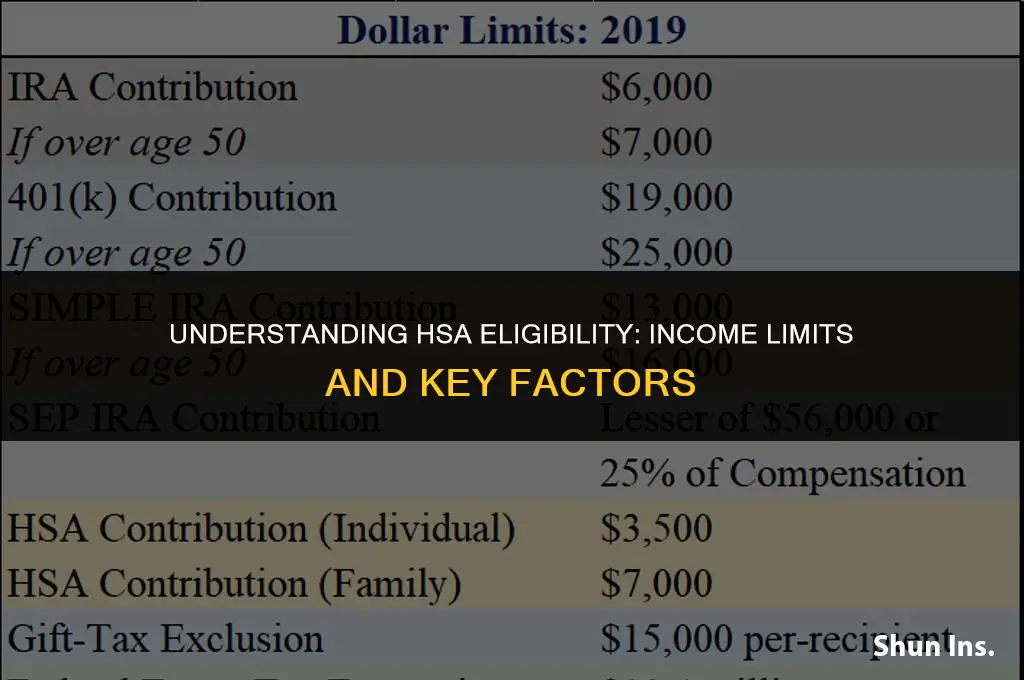

The Internal Revenue Service (IRS) sets specific income thresholds that determine eligibility for Health Savings Accounts (HSAs). These thresholds are adjusted annually to account for inflation and changes in the cost of living. For instance, in 2023, individuals with a gross income below $36,000 and families with a gross income below $72,000 are eligible to contribute to an HSA if they meet other criteria, such as having a high-deductible health plan (HDHP) and not being enrolled in Medicare.

It's crucial to understand these income limits because contributing to an HSA while ineligible can result in penalties. The IRS allows for a deduction of up to $3,600 for individuals and $7,200 for families (plus an additional $1,000 for those 55 and older) from taxable income, making HSAs a valuable tool for tax savings. However, exceeding the income limits can lead to the loss of these tax benefits and potential fines.

Moreover, the income thresholds are part of a broader set of eligibility criteria. In addition to income, individuals must also meet insurance and tax filing requirements. For example, they must be covered by an HDHP and not be claimed as a dependent on someone else's tax return. Understanding all these criteria is essential for maximizing the benefits of an HSA while avoiding potential pitfalls.

To navigate these rules effectively, it's advisable to consult with a tax professional or use IRS resources to ensure compliance. The IRS provides detailed guidance on HSA eligibility, including worksheets and examples, to help taxpayers determine if they qualify. By staying informed about the income thresholds and other eligibility requirements, individuals can make the most of HSAs as a tool for managing healthcare costs and saving for the future.

Life Insurance for Internationals: Top Companies Offering Global Coverage

You may want to see also

Explore related products

![]()

Contribution Limits: Explore the maximum annual contributions allowed for HSA accounts

For the 2023 tax year, the IRS has set the maximum annual contribution limit for HSA accounts at $3,850 for individuals and $7,750 for families. These limits apply regardless of income level, meaning that high-income earners can contribute the same amount as those with lower incomes. However, it's important to note that these contributions are subject to change each year, so it's essential to stay updated on the current limits.

One unique aspect of HSA contribution limits is that they are not affected by the income of the account holder. This means that individuals can contribute the maximum amount allowed, regardless of their salary or tax bracket. This is in contrast to other tax-advantaged accounts, such as 401(k)s or IRAs, which have contribution limits based on income.

Another important consideration is that HSA contribution limits are separate from the limits on other types of health savings accounts, such as FSAs or HRAs. This means that individuals can contribute to an HSA in addition to other health savings accounts, potentially allowing them to save more for healthcare expenses.

When it comes to maximizing HSA contributions, it's important to consider the overall healthcare needs of the individual or family. Those with higher healthcare expenses may benefit from contributing the maximum amount allowed, while those with lower expenses may not need to contribute as much. Additionally, it's important to consider the tax implications of HSA contributions, as they can reduce taxable income and potentially lower tax liability.

In conclusion, understanding the contribution limits for HSA accounts is essential for individuals looking to maximize their healthcare savings. By staying updated on the current limits and considering their overall healthcare needs and tax situation, individuals can make informed decisions about how much to contribute to their HSA accounts.

Does Notre Dame Health Insurance Cover Viagra? A Comprehensive Guide

You may want to see also

Explore related products

$0.99 $3.95

![The Medicare Bible for Beginners: [3 in 1] Unlock Medical Benefits and Quality Healthcare | Super Easy Insider Strategies to Navigate Medicare While Avoiding Costly Mistakes](https://m.media-amazon.com/images/I/61wrmwXah3L._AC_UL320_.jpg)

![]()

Tax Implications: Learn about the tax benefits and potential penalties related to HSA contributions

HSA contributions offer significant tax advantages, making them an attractive option for savvy savers. One of the primary benefits is the ability to contribute pre-tax dollars, reducing your taxable income for the year. This can lead to substantial savings, especially for those in higher tax brackets. Additionally, HSA funds grow tax-free, allowing your savings to compound more quickly than in a traditional savings account.

However, it's essential to understand the potential penalties associated with HSA contributions. If you withdraw funds for non-qualified expenses before age 65, you'll face a 20% penalty on top of the taxes owed. This penalty is designed to discourage early withdrawals and ensure that HSA funds are used for their intended purpose – covering healthcare costs.

To maximize the tax benefits of your HSA, it's crucial to contribute the maximum allowed amount each year. For 2023, the contribution limit is $3,850 for individuals and $7,750 for families. If you're 55 or older, you can make an additional "catch-up" contribution of $1,000. By contributing the maximum amount, you can take full advantage of the tax savings and grow your HSA balance more quickly.

When it comes to reporting HSA contributions on your taxes, you'll need to file Form 8889 with your tax return. This form details your HSA contributions, distributions, and any penalties owed. It's essential to keep accurate records of your HSA transactions throughout the year to ensure you can complete this form correctly.

In summary, HSA contributions offer valuable tax benefits, but it's essential to understand the potential penalties and contribution limits to maximize your savings. By following these guidelines and keeping accurate records, you can make the most of your HSA and enjoy significant tax advantages.

Choosing the Right Life Insurance Company: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Withdrawal Rules: Discover the conditions under which HSA funds can be withdrawn tax-free

To withdraw funds from a Health Savings Account (HSA) tax-free, you must meet specific conditions set by the IRS. First and foremost, the funds must be used for qualified medical expenses. These include costs for medical care, dental care, vision care, and prescription drugs, among others. It's important to note that not all medical expenses qualify; for instance, health insurance premiums typically do not qualify unless you are self-employed.

Another key condition is that you must be enrolled in a high-deductible health plan (HDHP) and not be enrolled in Medicare. If you are enrolled in Medicare, you can no longer contribute to your HSA, but you can still withdraw funds tax-free for qualified medical expenses. Additionally, you cannot be claimed as a dependent on someone else's tax return.

The process of withdrawing funds tax-free involves keeping detailed records of your medical expenses. You will need to provide documentation that substantiates the medical nature of the expense and the amount paid. This can include receipts, invoices, and statements from healthcare providers. It's crucial to maintain these records, as the IRS may request them during an audit.

One common mistake to avoid is withdrawing more funds than you have spent on qualified medical expenses. If you do this, the excess amount will be considered taxable income. To prevent this, keep track of your medical expenses and only withdraw the amount you have spent.

Finally, it's worth noting that there are no income limits for having an HSA or for withdrawing funds tax-free. However, if your income changes, it may affect your eligibility to contribute to an HSA. For example, if your income decreases, you may become eligible for Medicaid, which would disqualify you from contributing to an HSA. Conversely, if your income increases, you may no longer be eligible to contribute to an HSA if you are no longer enrolled in an HDHP.

In summary, to withdraw HSA funds tax-free, you must use them for qualified medical expenses, be enrolled in an HDHP, not be enrolled in Medicare, not be claimed as a dependent, and maintain detailed records of your medical expenses. Remember to only withdraw the amount you have spent on qualified expenses to avoid taxable income.

Does Harding Northland Insurance in Washburn, Iowa Offer Health Plans?

You may want to see also

Explore related products

![]()

Comparison with Other Plans: Evaluate how HSAs differ from other health savings options like FSAs and HRAs

Health Savings Accounts (HSAs) are a popular choice for individuals looking to save money on healthcare costs, but they're not the only option available. Flexible Spending Accounts (FSAs) and Health Reimbursement Arrangements (HRAs) are two other health savings options that individuals may consider. While all three options offer tax advantages, there are key differences between them that can impact an individual's decision.

One of the main differences between HSAs, FSAs, and HRAs is the way they are funded. HSAs are funded by the individual, while FSAs are typically funded through payroll deductions and HRAs are funded by the employer. This difference in funding can impact the tax benefits and the flexibility of the accounts. HSAs offer more flexibility in terms of how the funds can be used, as they can be rolled over from year to year and used for qualified medical expenses at any time. FSAs and HRAs, on the other hand, have more restrictions on how the funds can be used and typically have a "use it or lose it" policy, meaning that any unused funds at the end of the year are forfeited.

Another key difference between these health savings options is the eligibility requirements. HSAs are available to individuals who have a high-deductible health plan (HDHP) and are not enrolled in Medicare. FSAs are available to individuals who are employed and have access to a FSA through their employer. HRAs are also employer-sponsored and are typically available to individuals who have a high-deductible health plan.

When comparing HSAs, FSAs, and HRAs, it's important to consider the contribution limits, tax benefits, and flexibility of each option. HSAs offer the highest contribution limits and the most flexibility, but they require individuals to have a high-deductible health plan. FSAs and HRAs offer lower contribution limits and more restrictions on how the funds can be used, but they may be a better option for individuals who do not have access to a high-deductible health plan or who are looking for an employer-sponsored option.

In conclusion, while HSAs, FSAs, and HRAs all offer tax advantages and can help individuals save money on healthcare costs, they have key differences that can impact an individual's decision. By understanding the funding, eligibility requirements, and flexibility of each option, individuals can make an informed decision about which health savings option is right for them.

Which Virginia Doctors Accept Medicaid Insurance?

You may want to see also

Frequently asked questions

No, there is no income limit for having HSA health insurance. HSAs are available to anyone who has a high-deductible health plan (HDHP) and is not enrolled in Medicare.

Yes, you can contribute to an HSA even if your spouse has a different health plan. However, your spouse's plan must also be an HDHP for you to be eligible to contribute to your own HSA.

Your HSA funds are yours to keep, even if you change jobs or lose your health insurance. You can use the funds for qualified medical expenses at any time, and they will continue to grow tax-free as long as they remain in the HSA.