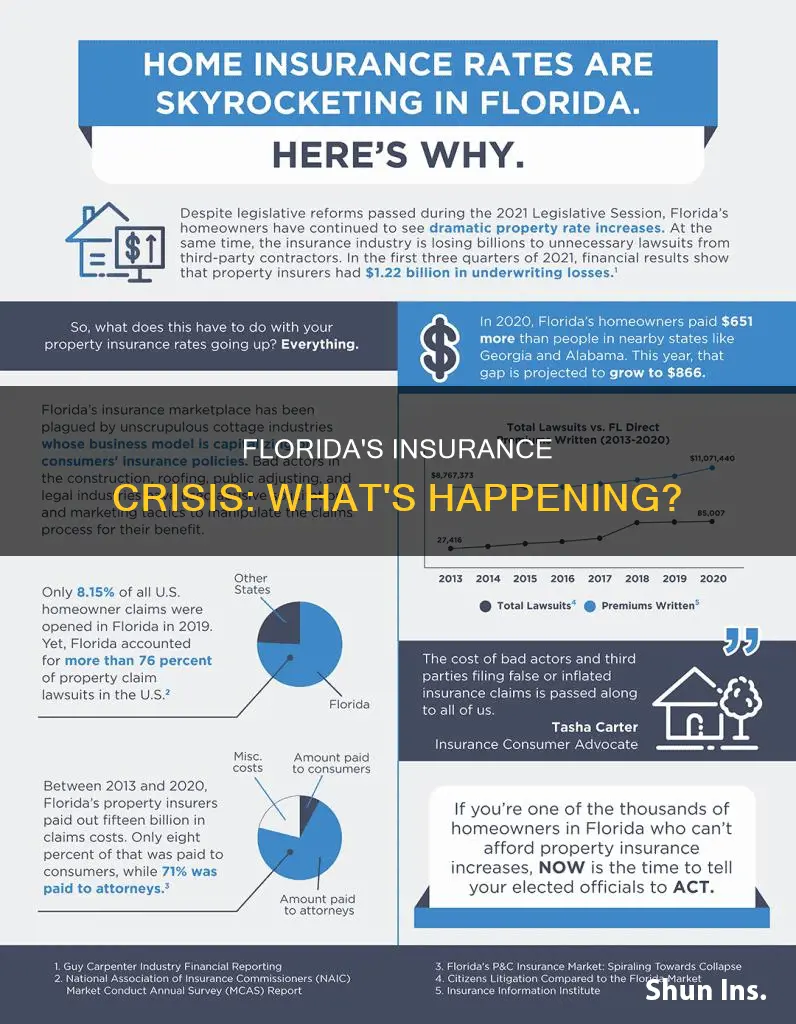

Florida's insurance market is in a state of crisis, with soaring premiums, fraudulent claims, and an increasing number of insurers pulling out of the state. The crisis has been attributed to a combination of factors, including the state's vulnerability to hurricanes and natural disasters, high litigation costs, and fraudulent roofing scams. The impact of this crisis is being felt by homeowners, with rising insurance rates and limited coverage options, and it is also affecting the housing market, as buyers and sellers struggle to secure insurance. While new legislation has been introduced to address the issues, it remains to be seen how soon the situation will improve.

| Characteristics | Values |

|---|---|

| Cause of the crisis | A combination of factors including hurricanes, storms, litigation abuse, fraud, and scams |

| Impact | Skyrocketing insurance premiums, insurance companies leaving the state, and limited coverage options for homeowners |

| Efforts to Address the Crisis | Senate Bill 2-A passed in December 2022 to reduce litigation abuse and assignment of benefits abuse; new companies entering the market |

| Current Status | The crisis appears to be easing, with rate reductions and new companies entering the market |

Explore related products

What You'll Learn

![]()

Litigation abuse and high costs

Florida's insurance crisis has been long-brewing and is the result of a combination of factors, including hurricanes, storms, and litigation abuse. The state's vulnerability to hurricanes and storms, due to its geographic location, has always made it a risky market for insurance companies. However, the current crisis is primarily driven by man-made factors, with litigation abuse and high costs being significant contributors.

Litigation abuse in Florida has taken the form of fraudulent roofing claims and lawsuits. Roofing scams are prevalent, with contractors offering free inspections and claiming damage even when none exists. They convince homeowners to sign forms allowing them to file insurance claims, and if the insurance company denies the claim, the contractor sues without the homeowner's permission. This has resulted in a high volume of fraudulent lawsuits, driving up costs for insurance companies.

The impact of legal system abuse in Florida is significant. In 2021, six insurance carriers in the state became insolvent due to litigation abuse, with some "litigated to death," as described by Joe Petrelli, CEO of Demotech. The rise of third-party litigation funding and the increasing use of SEO and litigation platform software have also contributed to soaring litigation costs.

To address the crisis, Florida passed an insurance reform bill in December 2022, aiming to curb policyholder lawsuits and reduce the financial burden on insurance companies. The bill banned assignment of benefits forms for home insurance losses and eliminated the one-way attorney fee system. These changes are expected to reduce fraudulent lawsuits and slow down the mass volume of lawsuits filed against insurers.

The insurance crisis in Florida has had far-reaching consequences, affecting homeowners, the housing market, and businesses. Homeowners have faced skyrocketing insurance rates, difficulty obtaining coverage, and even sudden cancellations of their policies. The inability to secure insurance has disrupted real estate deals and impacted both buyers and sellers. Additionally, high insurance rates have made it challenging for companies to recruit and retain employees, influencing their decisions on where to operate.

The Hidden Dangers of Physical Hazards: Uncovering the Insurance Perspective

You may want to see also

Explore related products

![]()

Roofing scams

Florida's insurance crisis has been caused by a multitude of factors, including hurricanes, litigation, and roofing scams. The latter has been a significant contributor, with fraudulent roofing claims driving up the cost of insurance for homeowners.

The Assignment of Benefits (AoB) form is a common tool used by scammers. They pressure homeowners to sign this form, which allows the contractor to deal with the insurance company directly and file claims. Homeowners have been sued by these contractors when issues arise with the insurance company.

To avoid roofing scams, homeowners should be cautious of unsolicited offers for free inspections or repairs, especially after storms. It is important to contact your insurance company first to understand your policy and options. They can provide a list of reputable roofing companies. Additionally, be wary of contractors who insist on a "free roof" or claim that your roof needs to be fully replaced without exploring repair options.

The Florida Legislature has taken steps to address roofing scams, including eliminating the 25% rule, which mandated full roof replacement if damage exceeded 25%. Homeowners now have the choice to repair or replace their roofs. These legislative changes aim to protect residents and insurance companies from fraudulent activities.

Hurricane Shutters and Insurance Payouts: Does Preparation Impact Claims?

You may want to see also

Explore related products

![]()

Natural disasters

Florida's unique geography makes it susceptible to hurricanes and storms. The peninsula's thin shape means that even inland homes are not entirely shielded from hurricanes. Research from Colorado State University suggests that the current hurricane season is expected to be more severe than in the past. Florida has been hit by more hurricanes than any other state, and the damage they cause is often extensive. For example, Hurricane Ian in 2022 caused $112 billion in damage, making it the most expensive storm in Florida's history.

Hurricanes and other natural disasters, such as floods and fires, have led to billions of dollars in losses for insurance companies. As a result, insurance companies have been deterred from doing business in the state, with some choosing to leave or reduce their exposure. This has resulted in a decrease in the availability of coverage for homeowners and contributed to the insurance crisis in Florida.

The impact of natural disasters on the insurance market in Florida is significant. The combination of high claims costs and the risk of weather-related damage has made Florida a challenging market for insurance companies. As a result, insurance rates have risen sharply, and in some cases, homeowners have struggled to find affordable coverage. The crisis has also affected the housing market, as buyers and sellers face challenges when insurance is difficult to obtain or costly.

While natural disasters are a contributing factor to the insurance crisis in Florida, other factors, such as litigation abuse, assignment of benefits abuse, and roofing scams, also play a significant role. The high number of lawsuits and fraudulent claims have further strained the insurance industry, leading to increased premiums and reduced coverage options for homeowners.

Psychiatrists: Medical Specialists in Mental Health

You may want to see also

Explore related products

![]()

Insurers leaving the state

Florida's insurance crisis has been years in the making, with a combination of factors contributing to the current state of affairs. One of the most significant issues is the state's vulnerability to hurricanes and storms, which can cause widespread damage. Florida's geographical location makes it particularly susceptible to hurricanes, and with the state's large population, there are many homes at risk. In recent years, hurricanes have caused billions of dollars in damage, and the threat of future hurricanes has made insurers wary of doing business in the state.

In addition to the risk of hurricanes, Florida has also been plagued by insurance fraud and litigation abuse. The state has a history of high levels of litigation, with a disproportionate number of insurance lawsuits filed in Florida compared to other states. Many of these lawsuits are fraudulent, driven by roofing scams that take advantage of unsuspecting homeowners. These scams involve contractors offering free inspections and claiming damage even when there is none, only to sue the insurance company when they refuse to pay for unnecessary repairs. The combination of expensive claims, fraud, and lawsuits has placed a huge financial burden on insurance companies, leading some to leave the state or go out of business altogether.

The impact of the insurance crisis on Florida homeowners has been significant. As insurance companies pull out of the state or raise their rates, homeowners are facing higher premiums and limited coverage options. In some cases, homeowners have even had their policies abruptly canceled, leaving them vulnerable and struggling to find new coverage. The crisis has also affected the housing market, as buyers and sellers are impacted by the difficulty of securing affordable insurance.

In response to the crisis, Florida's government has taken steps to address the issues. In December 2022, the State Senate passed Bill 2-A, which introduced reforms aimed at reducing litigation abuse and assignment of benefits abuse. The bill included provisions to eliminate one-way attorney fees and ban assignment of benefit forms for home insurance losses. These changes are expected to reduce the financial pressure on insurance companies and hopefully lure them back to the state. However, it will take time to see the full impact of these legislative reforms.

While the insurance crisis in Florida is complex and deep-rooted, there are signs that the situation is starting to improve. New legislation is impacting rates, and the entry of new companies into the market is increasing competition and easing the crisis. Homeowners are encouraged to explore their options and carefully consider their coverage choices to navigate the challenging insurance landscape in Florida.

American Integrity Insurance: Florida Exodus Explained

You may want to see also

Explore related products

![]()

Impact on the housing market

Florida's insurance crisis has had a significant impact on the housing market. The crisis has resulted in rising insurance rates, with some homeowners facing unaffordable premiums. This has made it challenging for homeowners to find affordable coverage, and in some cases, insurance companies have pulled out of the state or stopped renewing policies in high-risk areas, leaving homeowners with limited options. As a result, buyers and sellers are impacted as insurance is typically required to complete a home sale.

The difficulties in obtaining insurance have caused deals to fall through, as Bill Baldwin, owner of Boulevard Realty in Houston, has observed. Insurance companies may make demanding requirements at the last minute, such as requesting new roofs or tree removal, which can be challenging or impossible to meet, ultimately causing the sale to collapse.

The insurance crisis has also affected the commercial real estate market. Higher premiums and commercial property casualty rates have increased the cost of doing business, making it challenging for companies to recruit and retain employees.

Furthermore, the crisis has led to a rise in state-backed insurance programs, such as Citizens Insurance, which offers coverage to those who cannot obtain private insurance. However, while these programs provide a safety net, they may have limited coverage, and their premiums may not always be affordable.

The root causes of the insurance crisis, such as litigation abuse and assignment of benefits abuse, are being addressed through legislative reforms like Senate Bill 2-A. These reforms aim to reduce fraudulent lawsuits and stabilize the market, which could positively impact the housing market by making insurance more accessible and affordable. However, it will take time for the effects of these legislative changes to be fully realized.

Gynecologists: Insurance-Covered Specialists?

You may want to see also

Frequently asked questions

The insurance crisis in Florida is caused by a combination of factors, including hurricanes and storms, litigation, fraud, and lawsuits.

Floridians face rising insurance rates, limited coverage, and in some cases, non-renewal or cancellation of their insurance policies. The crisis is also affecting the housing market, as insurance is required to complete a home sale.

In December 2022, the Florida State Senate passed Bill 2-A, which aims to reduce litigation abuse and assignment of benefits abuse, as well as ban assignment of benefit forms and eliminate one-way attorney fee systems.

Floridians facing skyrocketing rates or non-renewal of their policies can explore other insurance providers, as having more options often leads to better rates. Citizens Insurance is a state-backed option, but their coverage may be limited.