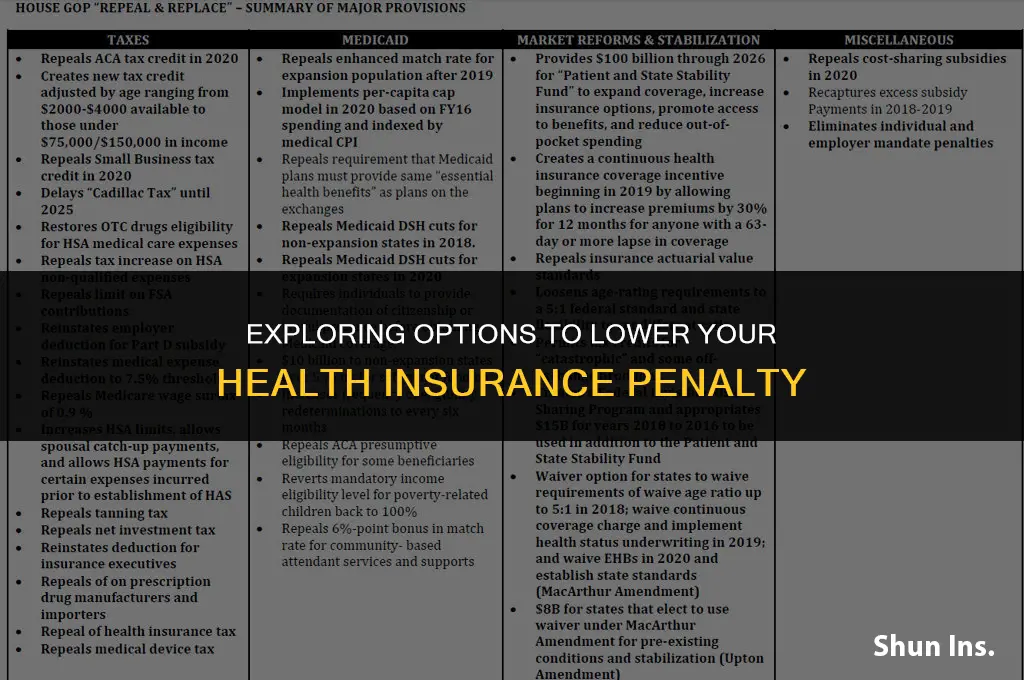

The question of whether there are ways to reduce health insurance penalties is a pertinent one, especially given the increasing costs of healthcare and the complexities of insurance policies. Health insurance penalties, often in the form of higher premiums or out-of-pocket expenses, can be a significant financial burden for individuals and families. This paragraph will explore some potential strategies and considerations for mitigating these penalties, including understanding the factors that influence premium costs, such as age, health status, and coverage level, as well as the importance of comparing different insurance plans and providers to find the most cost-effective option. Additionally, it will touch on the role of government subsidies and tax credits in making health insurance more affordable, and the potential benefits of maintaining continuous coverage to avoid penalties associated with gaps in insurance.

| Characteristics | Values |

|---|---|

| Type of Penalty | Financial penalty for not having health insurance |

| Penalty Amount | Varies by country and region; often a percentage of income |

| Purpose | To encourage individuals to maintain health insurance coverage |

| Applicability | Typically applies to individuals without employer-sponsored insurance or government-funded coverage |

| Frequency | Usually assessed annually during tax filing |

| Ways to Reduce | 1. Obtain health insurance coverage, 2. Qualify for exemptions (e.g., low income, religious beliefs), 3. Utilize tax credits or subsidies |

| Impact on Finances | Can significantly affect personal finances if not managed properly |

| Legal Requirements | Mandated by government laws and regulations |

| Effect on Health | Indirectly affects health by influencing access to healthcare services |

| Public Opinion | Often debated; some view it as necessary, others as an undue burden |

| Alternatives | Some countries offer universal healthcare, reducing the need for such penalties |

| Enforcement | Typically enforced through tax collection mechanisms |

| Historical Context | Evolved from efforts to increase healthcare accessibility and reduce uninsured rates |

| Current Trends | Increasing awareness and efforts to reduce the penalty through policy changes |

| Future Outlook | Potential for reform or adjustment based on public feedback and policy evaluations |

Explore related products

$12.99 $12.99

What You'll Learn

- Understanding the Penalty: Explanation of the health insurance penalty and its implications

- Exemptions: Conditions under which one might be exempt from the health insurance penalty

- Subsidies: Availability of subsidies to help reduce the cost of health insurance

- Tax Credits: Information on tax credits that can lower the health insurance penalty

- State-Specific Options: Variations in health insurance penalties and options by state

![]()

Understanding the Penalty: Explanation of the health insurance penalty and its implications

The health insurance penalty, often referred to as the individual mandate penalty, is a fee imposed on individuals who fail to maintain minimum essential health coverage as required by the Affordable Care Act (ACA). This penalty is designed to encourage people to have health insurance and to help offset the costs of uncompensated care. The penalty amount is calculated based on a percentage of your household income or a flat fee, whichever is greater. For example, in 2023, the penalty is 2.5% of your household income or $695 per adult and $347.50 per child, up to a maximum of $2,085 per family.

Understanding the implications of this penalty is crucial for making informed decisions about your health coverage. If you're uninsured, you may be subject to this penalty when you file your federal income tax return. The penalty can be particularly significant for higher-income individuals, as it is based on a percentage of income. Moreover, the penalty can increase over time if you remain uninsured, making it increasingly costly.

There are certain exemptions to the health insurance penalty. For instance, if you have a hardship exemption approved by the marketplace or if you are a member of a federally recognized tribe, you may not have to pay the penalty. Additionally, if you are incarcerated, you are exempt from the penalty. It's important to note that these exemptions are specific and require documentation to prove eligibility.

To avoid the penalty, it's essential to have minimum essential health coverage. This can include employer-sponsored health insurance, individual health insurance purchased through the marketplace, Medicaid, Medicare, or other qualifying plans. If you're unsure about your coverage options or how to enroll, you can seek assistance from a health insurance navigator or visit the official health insurance marketplace website.

In conclusion, understanding the health insurance penalty and its implications is key to making informed decisions about your health coverage. By being aware of the potential costs and exemptions, you can take steps to ensure that you have the necessary coverage to avoid the penalty and protect your financial well-being.

Accessing Healthcare Without Insurance: Your Practical Guide

You may want to see also

Explore related products

![]()

Exemptions: Conditions under which one might be exempt from the health insurance penalty

Certain individuals may be exempt from the health insurance penalty under specific conditions. For instance, if you are uninsured for less than three months in a year, you may qualify for a short-term exemption. This exemption is designed to accommodate life transitions, such as job changes or moving to a new state, where there might be a temporary lapse in coverage.

Another exemption applies to individuals who cannot afford health insurance due to financial hardship. This is determined by calculating the cost of the cheapest available plan and comparing it to your income. If the premium exceeds a certain percentage of your income, you may be eligible for an exemption. This ensures that the penalty does not disproportionately affect low-income individuals who genuinely cannot afford coverage.

Additionally, there are exemptions for certain groups, such as members of recognized religious organizations that oppose health insurance, or individuals who are not citizens or lawful residents of the United States. These exemptions are based on specific criteria and require documentation to support the claim.

It's important to note that exemptions are not automatic and must be applied for through the appropriate channels, typically when filing your tax return. The process involves submitting a form detailing your circumstances and providing any necessary supporting documentation. If approved, the exemption will be applied retroactively, and you will not be subject to the penalty for the period in question.

Understanding these exemptions can help individuals navigate the complexities of the health insurance system and avoid unnecessary penalties. It's crucial to stay informed about the specific conditions and requirements for each exemption to ensure compliance and take advantage of any available relief.

Will Insurance Cover Branded Titles? Understanding Your Policy's Fine Print

You may want to see also

Explore related products

![]()

Subsidies: Availability of subsidies to help reduce the cost of health insurance

Subsidies are a crucial aspect of making health insurance more affordable for many individuals and families. These financial aids are designed to help reduce the monthly premiums and out-of-pocket costs associated with health coverage. Depending on the country and specific health insurance system, subsidies may be available to those who meet certain income criteria, have specific health conditions, or fall into particular demographic groups.

In the United States, for example, the Affordable Care Act (ACA) provides subsidies to eligible individuals who purchase health insurance through the ACA marketplaces. These subsidies, known as premium tax credits, are based on income and can significantly lower the cost of health insurance for those who qualify. Additionally, some states offer their own subsidies or have expanded Medicaid programs to provide more affordable health coverage options.

To determine if you are eligible for health insurance subsidies, it is essential to research the specific requirements and application processes in your country or region. This may involve consulting government websites, contacting local health insurance providers, or seeking assistance from a healthcare navigator or insurance broker. By understanding the available subsidies and how to access them, you can make more informed decisions about your health insurance options and potentially reduce your overall healthcare costs.

It is also important to note that subsidies may have limitations or restrictions, such as eligibility requirements, enrollment periods, and caps on the amount of financial assistance provided. Therefore, it is crucial to carefully review the terms and conditions of any subsidy program before enrolling to ensure that it meets your needs and expectations.

In conclusion, subsidies can be a valuable tool for reducing the cost of health insurance and making it more accessible to a wider range of people. By exploring the availability of subsidies in your area and understanding their specific requirements and limitations, you can take advantage of these financial aids to help manage your healthcare expenses more effectively.

Report Medical Insurance Issues: Who to Call and Why

You may want to see also

Explore related products

![]()

Tax Credits: Information on tax credits that can lower the health insurance penalty

Tax credits can significantly reduce the health insurance penalty for individuals and families. These credits are essentially discounts on your health insurance premiums, and they're available to those who meet certain income and eligibility requirements. The amount of the credit varies based on your income level and the size of your family, but it can substantially lower the cost of health insurance, making it more affordable and reducing the penalty for not having coverage.

To qualify for these tax credits, you must purchase health insurance through the Health Insurance Marketplace or a state-based exchange. You cannot receive tax credits if you buy insurance directly from an insurance company or through an employer-sponsored plan. Additionally, your income must fall within a certain range – typically between 100% and 400% of the Federal Poverty Level (FPL) – to be eligible for tax credits.

The process of applying for tax credits is relatively straightforward. When you enroll in a health insurance plan through the Marketplace or a state exchange, you'll be asked to provide information about your income and family size. Based on this information, the exchange will determine if you're eligible for tax credits and will apply them to your monthly premiums. You'll receive a notice from the exchange detailing the amount of your tax credit and how it will be applied to your insurance costs.

It's important to note that tax credits are not the same as subsidies. Subsidies are payments made directly to insurance companies to reduce the cost of coverage, while tax credits are applied to your tax return and can be used to offset the cost of your premiums. This distinction is crucial because it affects how you receive and use the financial assistance.

To maximize the benefits of tax credits, it's essential to understand how they work and how they can be used to your advantage. For example, if you're eligible for a tax credit, you may want to consider purchasing a more comprehensive insurance plan than you would have otherwise, as the credit can help offset the additional cost. Additionally, it's important to be aware of any changes to the tax credit program, as these can impact your eligibility and the amount of assistance you receive.

In conclusion, tax credits can be a valuable tool for reducing the health insurance penalty and making coverage more affordable. By understanding the eligibility requirements and how to apply for tax credits, you can take advantage of this financial assistance and ensure that you have the health insurance coverage you need.

Understanding WPS Medicare Insurance Payments: What You Need to Know

You may want to see also

Explore related products

![]()

State-Specific Options: Variations in health insurance penalties and options by state

The landscape of health insurance penalties varies significantly from state to state, reflecting the diverse approaches to healthcare policy across the United States. While the Affordable Care Act (ACA) established a federal framework for health insurance, states have considerable leeway in implementing and enforcing their own regulations. This has led to a patchwork of penalties and options that can be both confusing and advantageous for consumers, depending on their state of residence.

In some states, such as California and New York, penalties for not having health insurance can be substantial, with fines reaching hundreds of dollars per year. These states often have their own health insurance exchanges and may offer additional subsidies or assistance programs to help residents afford coverage. On the other hand, states like Texas and Florida have opted not to expand Medicaid under the ACA and may have fewer state-specific resources available to help reduce health insurance penalties.

One unique approach is seen in states like Massachusetts and Hawaii, which have implemented their own individual mandates and penalty structures separate from the federal government. Massachusetts, for example, requires residents to have health insurance that meets certain minimum standards, and those who fail to comply may face penalties assessed by the state's Department of Revenue. Hawaii, meanwhile, has a more complex system that includes both employer and individual mandates, with penalties for non-compliance ranging from fines to tax credits.

Other states have taken a more laissez-faire approach, with minimal state-specific penalties or options. In these states, residents may be more reliant on federal programs and subsidies to help afford health insurance. However, even in these states, there may be local resources and assistance programs available to help navigate the complexities of health insurance and reduce penalties.

Understanding the state-specific options and penalties for health insurance is crucial for consumers looking to minimize their costs and maximize their coverage. By researching their state's unique approach to health insurance, individuals can make informed decisions about their coverage options and potentially reduce their financial burden.

Is Silver Health Insurance Worth It? Pros, Cons, and Cost Analysis

You may want to see also

Frequently asked questions

Yes, there are several ways to potentially reduce the health insurance penalty. One common method is to qualify for a hardship exemption, which may be granted if you can prove that you cannot afford coverage or that coverage is not available to you. Additionally, some states have expanded Medicaid under the Affordable Care Act, which can provide low-cost or free health insurance to eligible individuals. It's also important to shop around for plans during open enrollment periods to find the most affordable option available to you.

To qualify for a hardship exemption from the health insurance penalty, you must demonstrate that you have experienced a significant hardship that prevented you from obtaining health insurance. This could include situations such as homelessness, bankruptcy, or a serious medical condition that has left you unable to work. You will need to provide documentation to support your claim, and the specific criteria may vary depending on your state and the marketplace where you are applying for coverage.

Medicaid expansion under the Affordable Care Act helps reduce the health insurance penalty by providing low-cost or free health insurance to eligible individuals who may not be able to afford private coverage. By expanding Medicaid eligibility to include more low-income adults, the ACA has made it easier for people to access affordable health care and avoid the penalty for not having insurance. If you live in a state that has expanded Medicaid, you may be able to qualify for coverage even if you do not meet the traditional eligibility requirements.