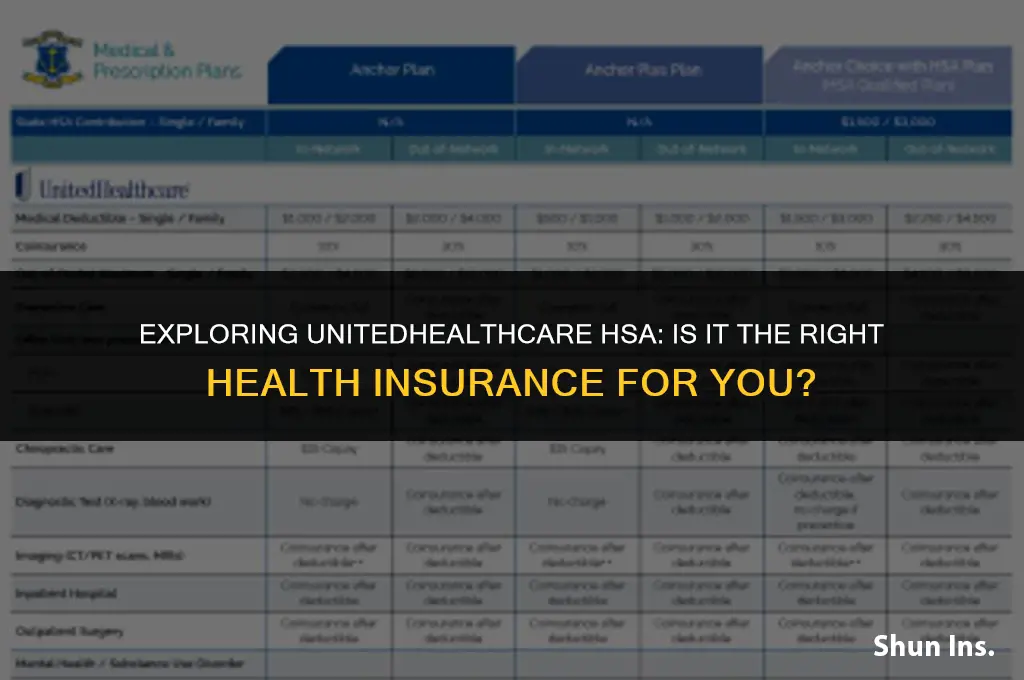

UnitedHealthcare HSA (Health Savings Account) is a type of health insurance plan that combines a high-deductible health plan (HDHP) with a tax-advantaged savings account. This plan is designed to help individuals and families save money on healthcare costs while also providing comprehensive coverage. With a UnitedHealthcare HSA, members can contribute pre-tax dollars to their HSA, which can then be used to pay for qualified medical expenses, such as deductibles, copays, and coinsurance. Additionally, the HSA funds can be invested and grow tax-free, providing a long-term savings solution for healthcare costs. UnitedHealthcare HSA plans are available to individuals and families who are not enrolled in Medicare and are not covered by an employer-sponsored health plan.

Explore related products

What You'll Learn

- Eligibility: Requirements to qualify for UnitedHealthcare HSA health insurance plans

- Coverage: Types of medical services and treatments covered under the HSA plans

- Costs: Premiums, deductibles, and out-of-pocket expenses associated with the HSA plans

- Benefits: Advantages of choosing UnitedHealthcare HSA plans, including tax benefits

- Enrollment: Steps and procedures to enroll in UnitedHealthcare HSA health insurance plans

![]()

Eligibility: Requirements to qualify for UnitedHealthcare HSA health insurance plans

To qualify for UnitedHealthcare HSA health insurance plans, individuals must meet specific eligibility requirements. These plans are designed for people who have a high-deductible health plan (HDHP) and are not enrolled in Medicare. The primary requirement is that you must have an HDHP with a minimum deductible amount, which varies by plan and year. For example, in 2023, the minimum deductible for an individual is $1,400, while for a family it is $2,800. Additionally, you must not have any other health coverage, with the exception of certain types of plans like dental, vision, or long-term care insurance.

Another key requirement is that you must be under the age of 65, unless you are disabled. If you are disabled, you may be eligible for an HSA plan regardless of your age, but you must provide proof of your disability status. Furthermore, you must not be enrolled in Medicare, as HSA plans are not compatible with Medicare coverage. If you are eligible for Medicare but have not yet enrolled, you may still qualify for an HSA plan.

It's important to note that HSA plans have contribution limits, which change annually. In 2023, the maximum contribution for an individual is $3,650, while for a family it is $7,300. These limits include any contributions made by your employer. If you exceed these limits, you may face tax penalties.

When considering an HSA plan, it's crucial to understand the tax implications. Contributions to an HSA are tax-deductible, and the funds can be used tax-free for qualified medical expenses. However, if you use the funds for non-qualified expenses, you will be subject to taxes and a 20% penalty. It's also important to keep track of your medical expenses, as you will need to provide documentation to substantiate your HSA withdrawals.

In summary, to qualify for a UnitedHealthcare HSA health insurance plan, you must have an HDHP, be under the age of 65 (unless disabled), not be enrolled in Medicare, and meet the contribution limits. Understanding the tax implications and keeping accurate records of your medical expenses are also essential aspects of managing an HSA plan effectively.

Does Your Health Insurance Cover Bariatric Surgery? What to Know

You may want to see also

Explore related products

![]()

Coverage: Types of medical services and treatments covered under the HSA plans

The HSA plans offered by UnitedHealthcare provide a comprehensive range of medical services and treatments, ensuring that members have access to essential healthcare when they need it. These plans typically cover preventive care, such as routine check-ups, vaccinations, and screenings, which are crucial for maintaining overall health and detecting potential issues early on. Additionally, HSA plans often include coverage for diagnostic services, such as lab tests, imaging, and other diagnostic procedures, which help healthcare providers accurately diagnose and treat medical conditions.

In terms of treatment coverage, HSA plans generally provide benefits for both inpatient and outpatient services. This includes hospital stays, surgeries, and other medical procedures performed in a hospital setting, as well as visits to specialists, primary care physicians, and other healthcare providers for ongoing treatment and management of chronic conditions. Prescription medications are also typically covered under HSA plans, with members often having access to a formulary of approved drugs at discounted rates.

One of the unique features of HSA plans is their flexibility in covering alternative and complementary therapies. Depending on the specific plan, members may have access to benefits for treatments such as acupuncture, chiropractic care, and massage therapy, which can be valuable for managing pain, improving mobility, and promoting overall wellness. Furthermore, HSA plans often provide coverage for mental health services, including counseling, therapy, and psychiatric care, recognizing the importance of addressing mental health concerns alongside physical health.

It's important to note that while HSA plans offer extensive coverage, there may be limitations and exclusions depending on the specific plan and state regulations. Members should always review their plan documents carefully to understand what services and treatments are covered, as well as any associated costs, such as copays, coinsurance, and deductibles. By doing so, they can make informed decisions about their healthcare and maximize the benefits of their HSA plan.

Affordable Health Insurance: Smart Strategies for Broke Individuals to Stay Covered

You may want to see also

Explore related products

![]()

Costs: Premiums, deductibles, and out-of-pocket expenses associated with the HSA plans

The cost structure of UnitedHealthcare's HSA plans is multifaceted, comprising several key components that policyholders must understand to make informed decisions about their health coverage. Premiums, which are the monthly payments made to maintain the insurance policy, vary based on factors such as age, location, and the specific plan chosen. Deductibles, on the other hand, represent the annual amount that insured individuals must pay out-of-pocket before the insurance company begins to cover their healthcare expenses. These deductibles can significantly impact the overall cost of care, especially for those with high healthcare needs.

In addition to premiums and deductibles, out-of-pocket expenses are another critical aspect of HSA plans. These expenses include copayments, coinsurance, and any costs incurred above the plan's maximum coverage limit. Understanding these out-of-pocket costs is essential for individuals to budget their healthcare expenses effectively. Furthermore, HSA plans often come with additional features such as prescription drug coverage, which may have its own set of costs and coverage limitations.

One of the unique aspects of HSA plans is their tax advantages. Contributions to an HSA are tax-deductible, and the funds can be used tax-free for qualified medical expenses. This can provide significant savings for policyholders, especially those in higher tax brackets. However, it is important to note that these tax benefits are contingent upon the individual meeting certain eligibility criteria, such as having a high-deductible health plan and not being enrolled in Medicare.

When evaluating the costs of UnitedHealthcare's HSA plans, it is also important to consider the potential long-term financial implications. For example, individuals should assess whether the lower premiums of an HSA plan are offset by the higher deductibles and out-of-pocket expenses. Additionally, policyholders should consider their expected healthcare needs and the likelihood of incurring significant medical expenses in the future. By carefully weighing these factors, individuals can determine whether an HSA plan is a cost-effective option for their health insurance needs.

Comcast Health Insurance: Domestic Partner Coverage Explained

You may want to see also

![]()

Benefits: Advantages of choosing UnitedHealthcare HSA plans, including tax benefits

UnitedHealthcare HSA plans offer several distinct advantages, particularly in terms of tax benefits. One of the primary benefits is the ability to contribute to your HSA with pre-tax dollars, which can significantly reduce your taxable income. This means that the money you set aside for healthcare expenses is not subject to federal income tax, and in many cases, state and local taxes as well.

Another key advantage is the tax-free growth of your HSA funds. Unlike other types of savings accounts, the interest and investment earnings in your HSA grow tax-free. This allows your healthcare savings to compound more quickly, providing you with a larger pool of funds to cover future medical expenses.

Additionally, UnitedHealthcare HSA plans often come with lower premiums compared to traditional health insurance plans. This is because HSAs are designed to encourage individuals to take a more active role in managing their healthcare costs, which can lead to more cost-effective care. By choosing an HSA plan, you may be able to save money on your monthly insurance premiums while still maintaining comprehensive coverage.

Furthermore, HSA plans typically offer more flexibility in terms of how you can use your funds. Unlike FSAs (Flexible Spending Accounts), which often have strict rules about what expenses can be covered, HSAs allow you to use your funds for a wide range of qualified medical expenses, including deductibles, copays, and even some over-the-counter medications.

Finally, UnitedHealthcare HSA plans may also provide access to additional resources and tools to help you manage your healthcare costs more effectively. This can include online portals to track your expenses, mobile apps to find in-network providers, and personalized health coaching to help you make informed decisions about your care.

In summary, choosing a UnitedHealthcare HSA plan can offer significant tax benefits, lower premiums, and greater flexibility in managing your healthcare costs. By taking advantage of these features, you can build a more secure financial future while still maintaining access to high-quality healthcare.

Medical Insurance: Getting the Right Coverage for Peace of Mind

You may want to see also

![]()

Enrollment: Steps and procedures to enroll in UnitedHealthcare HSA health insurance plans

To enroll in a UnitedHealthcare HSA health insurance plan, you must follow a series of steps that ensure you are properly registered and covered. First, you need to determine your eligibility for an HSA plan, which typically requires you to be enrolled in a high-deductible health plan (HDHP) and not be enrolled in Medicare. Once you have confirmed your eligibility, you can begin the enrollment process.

The enrollment process for UnitedHealthcare HSA plans can be completed online, over the phone, or through a paper application. If you choose to enroll online, you will need to visit the UnitedHealthcare website and follow the prompts to select your plan and provide the necessary personal and health information. If you prefer to enroll over the phone, you can call the UnitedHealthcare customer service number and speak with a representative who will guide you through the process. Alternatively, you can request a paper application by mail or download it from the UnitedHealthcare website, fill it out, and submit it by mail or fax.

Regardless of the enrollment method you choose, you will need to provide certain information, such as your name, address, date of birth, social security number, and health insurance information. You may also need to provide information about your employer, if you are enrolling through a workplace plan. Once you have submitted your enrollment application, UnitedHealthcare will review it and notify you of your acceptance or rejection.

If you are accepted into a UnitedHealthcare HSA plan, you will receive a confirmation letter and a member ID card. You will also need to set up your HSA account, which can be done through the UnitedHealthcare website or by contacting the HSA administrator directly. Once your HSA account is set up, you can begin contributing funds and using your HSA to pay for eligible health expenses.

It is important to note that enrollment in a UnitedHealthcare HSA plan is subject to certain deadlines and restrictions. For example, you may only be able to enroll during certain times of the year, such as during the annual open enrollment period or during a special enrollment period if you experience a qualifying life event. Additionally, you may be subject to waiting periods or pre-existing condition exclusions, depending on the specific plan you choose.

In conclusion, enrolling in a UnitedHealthcare HSA health insurance plan involves determining your eligibility, choosing an enrollment method, providing the necessary information, and setting up your HSA account. By following these steps and being aware of the deadlines and restrictions, you can successfully enroll in a plan that meets your health insurance needs.

Insurance Rate Changes in Georgia: Medical Factors and Your Premiums

You may want to see also