Travel insurance is designed to give travellers peace of mind and financial protection against travel risks. But is it worth it? The answer depends on several factors, including whether your trip is refundable, your destination, the coverage provided by your credit card, and your risk appetite. Travel insurance can reimburse non-refundable trip costs in the event of cancellation due to covered reasons, such as illness, injury, or job loss. It also covers lost or delayed luggage, travel delays, medical emergencies, and evacuation. While it may be tempting to skip travel insurance to save money, especially for cheaper or domestic trips, it can provide valuable protection against unforeseen events and expenses.

| Characteristics | Values |

|---|---|

| Cost | The average comprehensive travel insurance plan with flight coverage costs around $30/day. The average premium for these plans is $415, with an average trip length of 14 days. All-in-one policies cost about 56% more than basic trip insurance. |

| Coverage | Travel insurance covers a number of travel-related risks, including flight cancellations, delays, lost luggage, medical emergencies, accidental death, rental car damage, trip cancellation, trip delay, trip interruption, and emergency evacuation. |

| Necessity | Travel insurance is likely worth it if you've paid a considerable sum for a non-refundable vacation, if you're travelling internationally, or if you want peace of mind. It is also recommended by the U.S. State Department. |

| Alternatives | Some credit cards offer travel protection benefits, but these may not be as extensive as separate travel insurance plans. |

Explore related products

What You'll Learn

![]()

Peace of mind and financial protection

Travel insurance is designed to offer peace of mind and financial protection against travel risks. It covers a range of travel-related risks, from flight cancellations to lost bags and medical emergencies. It can also provide coverage for accidental death, rental car issues, trip delays, and trip interruptions.

The value of travel insurance depends on several factors, including whether your trip is refundable, your destination, and the coverage provided by your credit card. If you've paid a substantial amount for a non-refundable vacation or require coverage for medical needs while travelling, purchasing travel insurance is a good idea.

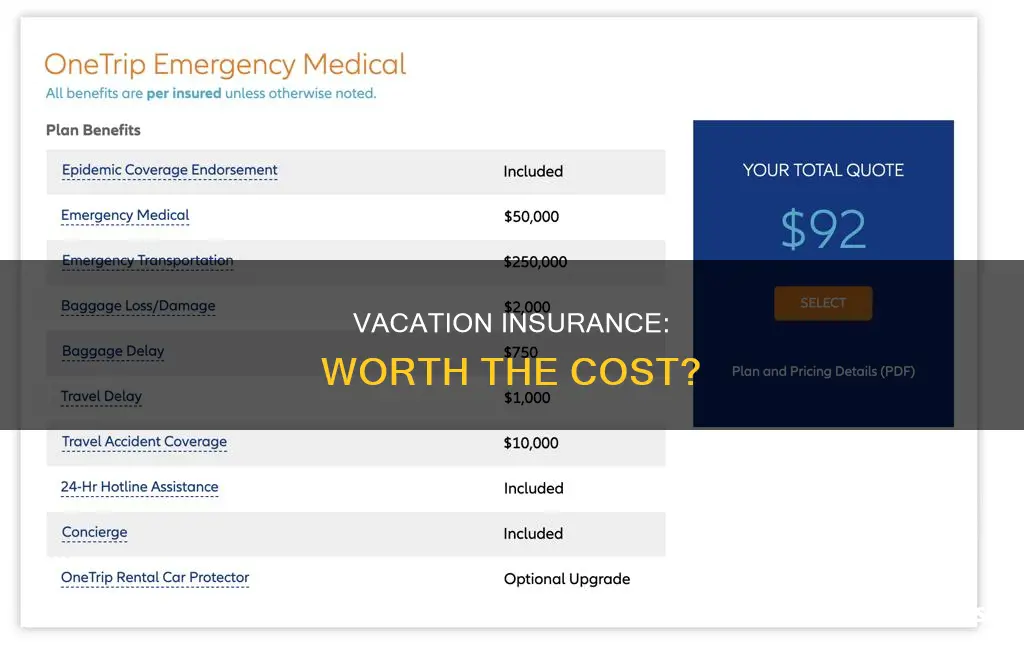

Comprehensive travel insurance typically covers trip cancellation protection, reimbursements for missed connections, refunds for illness or injury, and expenses related to medical or dental emergencies, disaster evacuations, and accidental deaths. It provides a combination of travel and medical cost coverage.

The cost of travel insurance varies, with all-in-one policies costing about 56% more than basic trip insurance. The price is determined by factors such as trip cost, traveller age, trip duration, destination, coverage type, and timing of purchase.

Ultimately, travel insurance gives you the peace of mind that you are protected financially in case of unexpected events or emergencies. It helps you manage the financial impact of travel delays, cancellations, interruptions, and medical issues, ensuring that you don't lose the money you've invested in your vacation.

When to Report Rental Insurance Claims

You may want to see also

Explore related products

![]()

Trip cancellation and reimbursement

Trip cancellation insurance can provide peace of mind and financial protection in the event of unforeseen circumstances. It covers reimbursement for non-refundable prepaid expenses, such as flights, accommodation, tours, and transportation, if a trip is cancelled or interrupted due to covered reasons. These reasons can include illness, injury, natural disasters, or other unforeseen events. For example, if you fall sick before your trip and your physician advises you to cancel, or if your airline ceases operations due to severe weather, trip cancellation insurance can safeguard you from financial loss.

The importance of trip cancellation insurance is emphasised by the potential costs incurred from unforeseen events. On average, a family of four budgets around $2,000 to $3,999 for a vacation, and a single-week trip for one person in the US costs more than $2,200. Without insurance, travellers are vulnerable to losing these funds due to unforeseen cancellations or interruptions. Trip cancellation insurance ensures reimbursement for these non-refundable expenses, providing financial relief.

Additionally, trip cancellation insurance can offer benefits beyond financial reimbursement. Some policies provide emergency evacuation services, ensuring travellers are transported to safety or appropriate medical facilities in the event of a natural disaster, political unrest, or medical emergency. This aspect of trip cancellation insurance is particularly valuable for travellers visiting regions prone to natural disasters or political instability.

When considering trip cancellation insurance, it is essential to carefully review the policy's covered reasons for cancellation. While illness, injury, and severe weather are typically included, other reasons may be excluded. For instance, some policies offer cancellation for any reason (CFAR) upgrades, allowing travellers to cancel for reasons not specified in the original policy. These upgrades often reimburse a percentage of the trip cost, usually between 50% and 75%, and are purchased within a specific timeframe of the initial trip deposit.

In conclusion, trip cancellation and reimbursement coverage is a valuable aspect of travel insurance, offering financial protection and peace of mind. By reimbursing non-refundable expenses and providing emergency assistance, trip cancellation insurance safeguards travellers from unforeseen events that may disrupt their plans and budgets. When considering trip cancellation insurance, travellers should carefully review the covered reasons for cancellation and select policies that align with their specific needs and destinations.

PSIP: Worth the Cost?

You may want to see also

Explore related products

$8.99 $9.99

![]()

Medical emergencies and evacuation

Travel insurance can help cover the costs of medical emergencies, from transportation to treatment and hospital stays. Medical evacuation insurance, sometimes called medical evacuation and repatriation insurance, covers the expense of transporting you from a remote area or inadequate medical facility to a better-equipped medical centre. This can cost tens of thousands of dollars, especially if you are in a remote location. The best travel insurance plans provide up to $1 million per person for medical evacuation.

When purchasing travel health and medical evacuation insurance, consider whether the insurer:

- Arranges with hospitals to guarantee direct payment

- Provides assistance via a 24-hour physician-backed support centre, which can help coordinate care and keep relatives informed

- Offers emergency medical transport to facilities in your home country or equivalent medical centres

- Covers medical services related to high-risk activities (e.g. scuba diving)

Before travelling, it is important to understand your existing insurance coverage and any additional coverage needed. Supplemental medical insurance is strongly recommended for travellers with pre-existing conditions, those who are pregnant, those engaging in high-risk activities, and those travelling to remote destinations or places with inadequate medical facilities.

Travellers should also be prepared to pay out of pocket for medical services and then initiate reimbursement with their insurers. Credit card companies may offer travel protection benefits, but these should not be considered a substitute for travel health insurance or medical evacuation insurance.

CI Insurance: Worth the Cost?

You may want to see also

Explore related products

$34.99 $36.99

![]()

Lost, delayed, or stolen luggage

Baggage insurance provides coverage for lost, damaged, stolen, or delayed luggage. It can help reimburse you for the cost of replacing items or for the value of your lost or stolen belongings. This coverage usually includes per-person, per-item, and specific limits for high-end items. For example, if you have a $63 plan, it may cover up to $750 of lost or stolen luggage, while a $103 plan might cover up to $2,500.

In addition to purchasing a separate baggage insurance plan, some comprehensive travel insurance plans also include coverage for baggage loss and delay. This means that if your baggage is delayed, you may be reimbursed for the purchase of necessary clothing or personal items. However, it's important to note that there is usually a waiting period before this coverage kicks in, typically between 12 and 24 hours.

Some airlines also offer baggage insurance when booking a flight or cruise. However, this coverage may have limitations, such as only covering certain issues on domestic flights and not extending to international trips or theft during your trip. Additionally, airlines may only provide travel vouchers instead of cash reimbursements, and only up to the depreciated value of your items.

Before purchasing baggage insurance, it's important to understand the coverage details and limitations to ensure it meets your needs. It's also a good idea to familiarize yourself with your airline's policies and your rights as a passenger. By taking these steps, you can ensure that you're prepared in the event of lost, delayed, or stolen luggage and make the most of your vacation.

Airline Insurance: Clark Howard's Take

You may want to see also

Explore related products

$33.99 $39.99

![]()

Travel credit cards and their coverage

When deciding whether to purchase travel insurance, it's worth considering the coverage you already have from your credit card. Credit card travel insurance is a complimentary benefit that often comes with credit cards. While it may not provide the most comprehensive coverage, it can be extremely useful in the event of travel-related emergencies and inconveniences.

To qualify for credit card travel insurance, cardholders usually need to use their card to book travel arrangements such as flights, hotels, or rental cars. Some credit card providers require you to book the entirety of your trip on their card, while others only require you to book the main transportation to your destination. It's important to review the specific terms and conditions outlined in the card agreement.

Credit card travel insurance typically includes coverage for trip cancellations, trip interruptions, and delays, as well as lost or delayed baggage. Some cards also provide coverage for emergency medical expenses, evacuation, and rental car insurance. The extent and specifics of the coverage vary among credit cards and may depend on factors such as the card type, the issuer, and the terms and conditions.

For example, the Chase Sapphire Reserve offers generous travel protections, including trip cancellation or interruption worth up to $10,000 per person and $20,000 per trip, reimbursement for trip delays, and lost or delayed baggage coverage. It also provides up to $75,000 in rental car insurance, which is primary insurance, meaning you don't need to file a claim with your personal auto insurance provider.

Other credit cards that offer robust travel insurance benefits include the Southwest Rapid Rewards Plus Credit Card, the Platinum Card from American Express, the Ink Business Preferred Credit Card, and the Bank of America Premium Rewards Card. These cards provide benefits such as trip cancellation, trip delay coverage, and, in some cases, less common perks.

When deciding whether to rely solely on credit card travel insurance or purchase additional coverage, consider your destination, the cost of your trip, and your risk tolerance. If you're travelling internationally or have paid a significant sum for a non-refundable vacation, purchasing comprehensive travel insurance may be a wise decision. Review the coverage provided by your credit card and assess if it adequately meets your needs.

Out-of-Service Insurance: Worth the Cost?

You may want to see also

Frequently asked questions

Vacation insurance is generally considered more necessary for international trips, as they are more expensive and require more advance planning. However, if you've paid a lot for your trip, travel insurance is a good idea to protect your investment.

Vacation insurance covers a number of travel-related risks, including trip cancellations and interruptions, lost luggage, medical emergencies, accidental death, and emergency evacuations.

The cost of vacation insurance depends on several factors, including trip cost, traveller age, trip duration, destination, and coverage type. Basic trip insurance usually covers lost bags, reimbursements for missed connections, and refunds if you can't travel due to illness or injury. Comprehensive insurance covers all of the above, plus medical and dental emergencies, disaster evacuations, and costs associated with accidental deaths. Comprehensive insurance costs about 56% more than basic insurance.

Credit card coverage is generally not as extensive as a separate travel insurance plan. Review the policy details to understand what is and isn't covered.