Workers' compensation insurance is a type of commercial insurance that covers employees who become sick or injured at work. It is required in almost every state, with the guidelines depending on location, the nature of work, and the number of employees. This type of insurance helps employees cover medical expenses, lost wages, rehabilitation costs, and disability benefits. It also protects employers by reducing their liability for work-related accidents and preventing employee lawsuits. While workers' compensation insurance is essential, businesses may also need general liability insurance to protect against common business risks such as customer injury, property damage, and copyright infringement.

| Characteristics | Values |

|---|---|

| Purpose | To provide financial support to employees who are injured or become sick as a result of their work |

| Coverage | Medical expenses, lost wages, rehabilitation costs, disability benefits, death benefits, dependent support payments, employer's liability expenses |

| Applicability | Required in almost every state, but guidelines depend on location, type of work, and number of employees |

| Cost | Median cost of $45 per month for small business owners; national median cost of $80 per month through Progressive |

| Importance | Protects employees' finances, reduces employer liability for work-related accidents, and helps businesses adhere to state laws |

Explore related products

What You'll Learn

- Workers' comp insurance covers medical expenses for employees injured or sick from their job

- It also covers lost wages and rehabilitation costs for injured employees

- Workers' comp insurance protects employers from lawsuits filed by injured workers

- Most states require businesses to have workers' comp insurance, especially with one or more employees

- Workers' comp insurance is distinct from general liability insurance, which covers third-party injuries and property damage

![]()

Workers' comp insurance covers medical expenses for employees injured or sick from their job

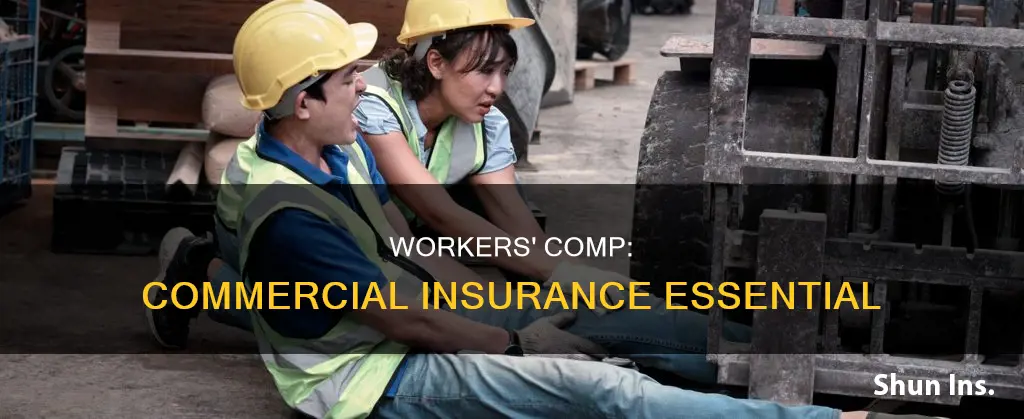

Workers' compensation insurance, also known as workers' comp, is a type of commercial insurance that provides benefits and coverage to employees who are injured or become sick due to their job. It is required in almost every state, and laws vary depending on location and the number of employees a business has. For example, in Nevada, every business with at least one employee is mandated to carry workers' comp insurance.

Workers' comp insurance covers medical expenses for employees, including doctor visits, hospital stays, surgeries, medications, and other treatments related to their work injury or illness. It can also cover ongoing care costs, such as physical therapy or occupational therapy, to help employees recover and return to work. This insurance helps protect employees' finances and ensures they can access the necessary medical treatments without incurring significant personal costs.

In addition to medical expenses, workers' comp insurance can also cover lost wages for employees who are unable to work due to their injury or illness. This helps provide financial support during their recovery period. Furthermore, workers' comp may provide disability benefits for employees who become partially or permanently disabled due to a work-related accident. These benefits can help supplement their income and support them in the long term.

It is important to note that workers' comp insurance typically only covers injuries or illnesses that are directly related to an employee's job duties. For example, it would cover an injury caused by lifting heavy equipment or slipping on a wet surface at work. However, if an employee is injured outside of work or during personal activities, such as playing football on a day off, workers' comp insurance would not apply.

Workers' comp insurance is essential for businesses to protect their employees and comply with state regulations. It provides financial support and ensures employees can access the medical care they need without facing financial hardship. By providing this coverage, businesses can also reduce their liability for work-related accidents and protect themselves from potential lawsuits.

Navigating the Path to Becoming a FEMA Insurance Adjuster

You may want to see also

Explore related products

![]()

It also covers lost wages and rehabilitation costs for injured employees

Workers' compensation insurance is a type of commercial insurance that provides benefits to employees who are injured or become ill due to their work. It covers medical costs, healthcare, lost wages, job retraining, and disability. Most states require businesses to have workers' compensation insurance, and it is an essential protection for employees in small businesses. Even if it is not legally required, purchasing workers' compensation insurance is advisable to protect the business from liability and ensure employees receive benefits to aid their recovery.

Workers' compensation insurance covers lost wages for employees who are unable to work due to a work-related injury or illness. The benefit rate an injured worker receives is determined by the date of injury and does not increase if new maximum benefits are adopted into law. Typically, programs pay about two-thirds of the worker's gross pay. Lost wage benefits are not paid for the first seven days of the disability, unless it extends beyond fourteen days. After 14 days, workers may receive lost wage benefits from the first workday they were unable to work. If a worker is totally or partially disabled and unable to work for more than seven days, they may receive lost wage benefits.

Workers' compensation also covers rehabilitation costs for injured employees. Rehabilitation may include physical therapy to restore full range of motion and strength in injured limbs and joints, or it may involve re-training for the job. If an employee has been out of work for several months, they may need to be retrained to resume their previous work. In cases of life-altering injuries, such as the loss of a limb, employees may need to learn new ways to adapt to their regular work duties or take on new tasks. The employer or insurance company may refer the employee to specific rehabilitation service providers.

The cost of workers' compensation insurance varies depending on the state and the type of work being performed. It is generally more expensive for high-risk jobs than for low-risk jobs. In California, for example, workers' comp costs an average of 40 cents for every $100 in payroll for low-risk workers and $33.57 for high-risk jobs. In New York, the average is 7 cents per $100 for low-risk jobs and $29.93 per $100 for high-risk jobs. Employers are responsible for purchasing workers' compensation insurance or becoming self-insured to provide coverage for their employees.

Protect Your Commercial Property: Tips for Insurability

You may want to see also

Explore related products

![]()

Workers' comp insurance protects employers from lawsuits filed by injured workers

Workers' compensation insurance, commonly known as workers' comp, is a type of commercial insurance that protects employers from lawsuits filed by injured or sick employees. It provides coverage for work-related injuries and illnesses, helping employees cover their medical bills and lost wages while also protecting employers from legal liability.

Workers' comp is important for businesses as it reduces their liability for work-related accidents and illnesses. It provides benefits to employees, including covering medical expenses, rehabilitation costs, and lost wages, which can help prevent lawsuits from employees seeking compensation for these damages. Most states in the US require businesses to have workers' comp insurance, with specific regulations varying by state.

By having workers' comp insurance, employers can protect themselves from most lawsuits filed by injured employees. This insurance acts as a safeguard, ensuring that employees receive the necessary benefits after sustaining a work-related injury or illness. Without this coverage, businesses may be held liable for sick or injured employees and could face legal consequences, including fines for non-compliance.

The specific protections provided by workers' comp insurance can vary depending on location and other factors. In most cases, workers' comp covers medical expenses related to doctor visits, hospital stays, surgeries, medications, and other treatments required by the injured employee. It may also cover lost wages, providing a portion of the employee's regular income if they are unable to work due to their injury or illness.

Additionally, workers' comp insurance can include rehabilitation costs, such as physical therapy or occupational therapy, to help employees recover and return to work. In some cases, it may also provide disability benefits for short- or long-term disabilities resulting from work-related injuries, although this is subject to the policy contract. While workers' comp protects employers from most lawsuits, there are exceptions, including claims involving acts of vicarious liability or negligence resulting in employee death.

Insurance Fraud: Pocketing Money, Illegal or Not?

You may want to see also

Explore related products

![]()

Most states require businesses to have workers' comp insurance, especially with one or more employees

Workers' compensation insurance is a type of commercial insurance that is required in almost every state. It is important for protecting employees in a business. It provides benefits to help cover medical bills and lost wages for employees who get hurt or sick from their job. This coverage is important because it protects employees' finances and helps reduce the employer's liability for work-related accidents.

While workers' compensation insurance is mandated across most states, the specific guidelines and regulations vary. The number of employees is a key factor in determining whether a business needs this type of insurance. Most states require businesses to have workers' compensation insurance as soon as they hire their first employee. For example, state laws in Nevada mandate that every business with at least one employee must carry workers' compensation insurance.

The cost of workers' compensation insurance also differs depending on the state and the specific characteristics of the business. The median cost for small business owners is $45 per month, while the national median cost through Progressive was $80 per month in 2024. The average monthly price was $125. The best way to determine the cost for a specific business is to get a quote from an insurance provider.

It is worth noting that workers' compensation insurance is not always mandatory. Some states, like Texas, do not require companies to purchase this type of insurance. Additionally, sole proprietors or self-employed individuals without employees may be exempt from this requirement in certain states. However, even if it is not legally mandated, purchasing workers' compensation insurance is still advisable to protect both the business and its employees.

Each state has its own set of workers' compensation laws, and employers must comply with the regulations in their respective state. These laws outline the requirements for coverage, the penalties for non-compliance, and the process for employees to receive benefits in the event of a work-related injury or illness. Therefore, it is essential for businesses to understand the specific workers' compensation laws in their state to ensure they are meeting their legal obligations and providing the necessary protection for their employees.

Navigating the Path to Becoming an Insurance Adjuster in Florida: A Comprehensive Guide

You may want to see also

Explore related products

![Compensation (The Criterion Collection) [Blu-ray]](https://m.media-amazon.com/images/I/71yx5jd1XCL._AC_UL320_.jpg)

![]()

Workers' comp insurance is distinct from general liability insurance, which covers third-party injuries and property damage

Workers' compensation insurance is distinct from general liability insurance. While both types of insurance are important for businesses, they serve different purposes and cover different risks.

General liability insurance protects your business from common risks such as bodily injury to customers, damage to a customer's property, copyright infringement, and advertising injury. It also typically includes product liability coverage, which covers claims related to injuries caused by your products. This type of insurance is important because it protects your business from financial losses in the event of a lawsuit. It covers attorney's fees, court costs, and settlements or judgments up to the policy limit. General liability insurance is often considered essential, even for small businesses or those with no employees, as it can protect you from unexpected accidents or oversights. For example, if a customer slips and falls at your business, general liability insurance would cover their medical expenses and any resulting legal costs.

On the other hand, workers' compensation insurance focuses on protecting your employees. It provides benefits to employees who are injured or become ill as a result of their work, helping to cover their medical expenses and lost wages. It can also cover rehabilitation costs, such as physical therapy, and provide disability benefits if the employee is left with a partial or permanent disability. In addition, workers' comp insurance can reduce your liability for work-related accidents and help your business comply with state laws, as most states require businesses to have this type of insurance. For example, if an employee injures themselves lifting heavy equipment or slipping on a wet surface, workers' comp would cover their medical bills and a portion of their wages if they are unable to work.

While general liability insurance covers third-party claims and property damage, workers' comp insurance is specifically designed to protect your employees and cover the costs associated with work-related injuries and illnesses. This distinction is important, as it ensures that your employees are taken care of and that your business is protected from financial and legal risks.

The cost of these insurance policies can vary depending on various factors, including the size and nature of your business, your location, and the number of employees. However, both types of insurance are considered essential for comprehensive business protection.

The Art of Damage Assessment: Unraveling the Insurance Adjuster's Process

You may want to see also

Frequently asked questions

Workers' compensation insurance covers employees who become sick, injured, or ill at work. It also covers lost wages and medical expenses.

General liability insurance protects your business from common business risks, including customer bodily injury, property damage, copyright infringement, and advertising injury. Workers' compensation insurance covers your employees for work-related injuries and illnesses.

Workers' compensation insurance is required in almost every state, but the guidelines depend on where you live, what you do, and how many employees you have. It is important to check your state and local laws to see if you need coverage.

The national median cost of workers' compensation insurance is $80 per month, and the average monthly price is $125. However, the cost will depend on specific qualities of your business, including your profession, state, payroll, and claims history.