It is important to verify insurance coverage before receiving dental treatment to avoid unexpected bills. While dental offices typically verify insurance, provide estimates, and file claims as a courtesy, they are not obligated to do so. Ultimately, patients are responsible for ensuring their provider is in-network and understanding their coverage limits. Patients with PPO dental insurance have more flexibility in choosing their dentist, but some offices may be out of network. It is advisable to confirm insurance details and address any changes to avoid confusion and unexpected financial burdens.

| Characteristics | Values |

|---|---|

| Responsibility of checking insurance coverage | Patient |

| Responsibility of verifying insurance coverage | Dental office |

| Dental office's obligation to verify insurance coverage | No obligation |

| Importance of insurance verification | Lays the foundation for how quickly the dental office will get paid by the patient and insurance company |

| Importance of knowing the patient's benefits | Helps communicate the patient's out-of-pocket expense and expected amount to collect from the insurance claim |

| Waiting period for new insurance plans | There might be a waiting period before patients can benefit from their insurance coverage |

Explore related products

What You'll Learn

![]()

Patient responsibility to check insurance coverage

Ultimately, it is the patient's responsibility to check their insurance coverage and understand their insurance plan's terms and conditions. Dental insurance is the patient's insurance, and when signing up for a plan, the patient agrees to be responsible for what the insurance does or does not cover, as well as any coverage limits and fine print. While a dental office will often verify insurance, provide an estimate, and file a claim as a courtesy, they are not obligated to do so.

Patients are expected to know what types of medical care require prior authorization and approval from their insurance carriers. For example, if a patient's insurance company requires a referral and they do not have one, they will be responsible for the full payment of their bill. Similarly, if a specialist requires more visits or tests than the insurer approves, the patient must obtain another referral and/or prior authorization from their primary care physician. It is also the patient's responsibility to notify their physician of their insurance and any changes to their insurance coverage.

Patients can take several steps to understand their insurance plan's benefits and financial obligations. They should consult their insurance plan's member handbook to learn its terms and conditions. While these handbooks can be lengthy and dense, patients are still held responsible for understanding and abiding by the terms of their plans. Additionally, patients can call the customer service or member services department of their insurance company to clarify what their plan covers and their financial responsibility. They can also reach out to their employer's human resources department for assistance.

It is important to distinguish between "in-network" and "out-of-network" providers when discussing insurance coverage. An "in-network" provider has agreed to honor the prices set by the insurance company, and charging anything other than the contracted pricing is considered insurance fraud. An "out-of-network" provider may still accept your insurance, but they are allowed to use a higher set of pricing since they are not contracted with the insurance company. For out-of-network providers, the insurance may cover only a portion of the bill, leaving the patient responsible for the remaining amount. Therefore, patients should confirm whether their insurance plan considers a specialist an in-network or out-of-network provider, as it will affect their financial responsibility for the bill.

Amazon Insurance: A Guide to Checking Your Coverage

You may want to see also

Explore related products

![]()

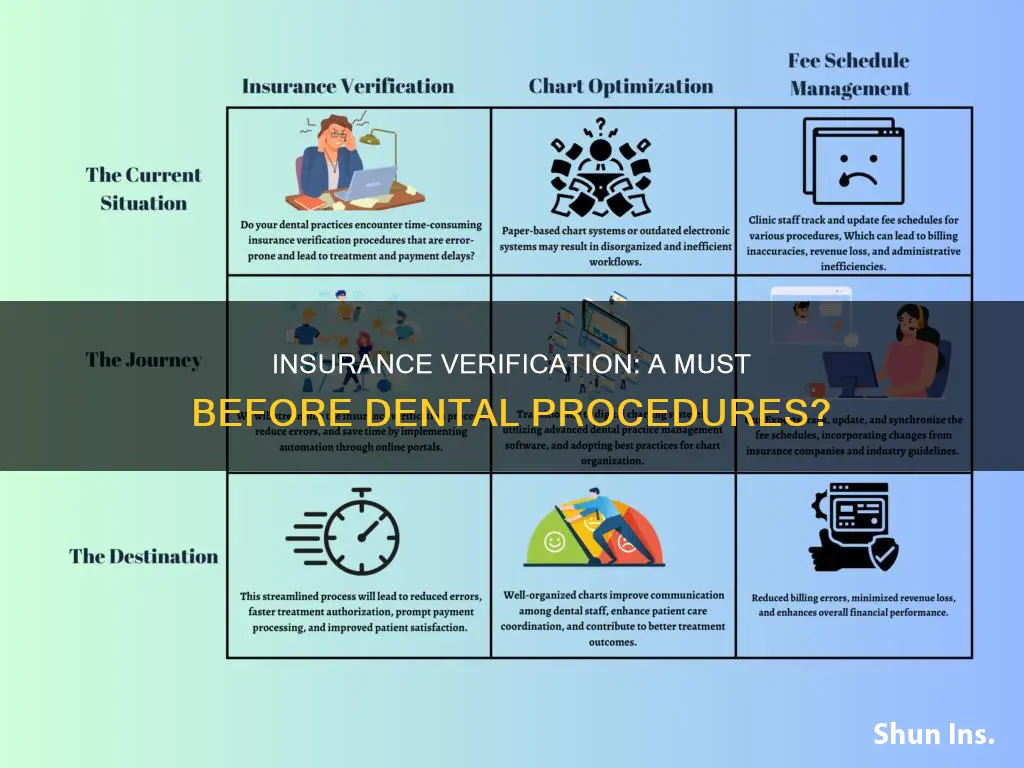

Dental office's insurance verification process

For a dental office, insurance verification is a critical step in the billing process. It is the foundation for how quickly the office will get paid by the patient and the insurance company. It is also key to building a clean claim reputation. An insurance company is less likely to deny or underpay a claim if the dental office follows the appropriate insurance verification process.

The insurance verification process typically involves the following steps:

- Collecting the patient’s health insurance information, including the insurance provider, insurance plan policy number, and potentially the group number.

- Contacting the insurance company to verify coverage benefits through the healthcare provider contact number or patient care portal.

- Generating medical billing estimates for the insurance provider’s responsibility and patient deductible.

- Built-in prior authorization management.

- Creating a patient eligibility verification report for office and medical billing management.

To streamline the insurance verification process, dental offices can:

- Use automated insurance verification software.

- Use an online form or system to input patient information, such as an Excel spreadsheet.

- Request patient insurance eligibility verification at several stages, as coverage can change with changing jobs, unemployment, or personal finance changes.

- Have the patient's address and other basic information on file.

Botox for Spasticity: Is Healthnet Federal Insurance On Board?

You may want to see also

Explore related products

![]()

In network vs out of network

When you enrol in dental insurance, you receive an insurance card that provides information about your coverage. This card often includes information about "in-network" and "out-of-network" healthcare providers. In-network providers are contracted with your insurance company and have agreed to provide services at pre-negotiated discounted rates. This means that if you choose an in-network dentist, you will typically pay less at the time of service, as you are only responsible for a copay and/or a percentage of the cost, which is usually lower than the fees for out-of-network providers. By choosing in-network providers, you can get 100% coverage for preventative care and some plans offer 50% coverage for more complex restorative treatments.

Out-of-network providers, on the other hand, have not agreed to your insurance plan's contracted rates. This means that you will typically pay more out-of-pocket expenses when choosing an out-of-network dentist. The insurance plan usually covers a lesser percentage of the higher charges, leading to higher overall costs. However, there are situations where choosing an out-of-network provider may be preferable. For example, an out-of-network dentist may have unique skills and expertise for a specific procedure or condition, or they may be more accessible in rural or remote areas. Additionally, you may prefer to continue seeing an out-of-network provider with whom you have an established relationship.

It is important to understand the financial implications of choosing an out-of-network dentist to effectively manage your dental care costs. Before scheduling an appointment, it is recommended to verify that the provider is part of your plan's network and to check for different payment plans and options. You can request a current list of network providers from your insurance company and use tools like the Ameritas Dental Cost Estimator to estimate potential costs. Additionally, knowing the full breakdown of your insurance benefits can help you communicate the patient's out-of-pocket expenses and expected insurance claim amounts. Insurance verification is the first step of the dental billing process and can help streamline the overall billing process. Using online forms or systems can aid in keeping track of patient data and insurance information.

Correcting Bulk Insurance Checks in SoftDent: A Step-by-Step Guide

You may want to see also

Explore related products

![ESSENTIAL Car Auto Insurance Registration BLACK Document Wallet Holders 2 Pack - [BUNDLE, 2pcs] - Automobile, Motorcycle, Truck, Trailer Vinyl ID Holder & Visor Storage - Strong Closure On Each -](https://m.media-amazon.com/images/I/61px7jy3NmL._AC_UL320_.jpg)

![]()

Waiting periods for new insurance plans

A dental insurance waiting period is the time after purchasing a new dental insurance plan during which you must wait before receiving benefits for treatment. Waiting periods vary depending on the plan and the type of treatment. Typically, there is no waiting period for preventive or diagnostic services such as routine cleanings, exams, and X-rays. However, there may be a waiting period for basic procedures such as fillings, and a longer waiting period for major procedures such as crowns, bridges, and dentures.

Waiting periods for basic care services can range from no waiting time to several months. For example, some plans may have a 6- to 12-month waiting period for restorative services like filings and non-surgical extractions. Major dental procedures usually have longer waiting periods, typically ranging from 6 to 12 months, and sometimes even 24 months. These procedures include crowns, bridges, dentures, and oral surgery.

It is important to carefully review the specifications of your new insurance plan to understand the applicable waiting periods. By knowing the full breakdown of your benefits, you can determine your out-of-pocket expenses and expected insurance claim amounts. This is crucial when planning for dental treatments, as receiving services during a waiting period may result in out-of-pocket payments for those services.

In certain cases, a waiting period may be waived. For instance, if you have had continuous coverage through another carrier or employer with no breaks in coverage when switching providers or jobs. Additionally, if you recently had comparable coverage, some insurers may waive the waiting period. Therefore, it is advisable to always ask for detailed information about new dental coverage and stay informed about your plan's specific waiting period requirements.

Insurance and Uber: What's the Deal?

You may want to see also

Explore related products

![]()

Dentists' contracts with insurance companies

It is important for a dentist's office to check a patient's insurance before performing any procedures, as it lays the foundation for how quickly the patient and insurance company will pay. This is a crucial step in the dental billing process. Knowing the full breakdown of a patient's benefits can help communicate what their out-of-pocket expenses will be and what the dentist can expect to collect from the insurance claim filed after the appointment.

Dentists often sign contracts with insurance companies, known as participating provider agreements, which are legal contracts between the dentist and a third-party payer. These contracts can include broad language that may place liability on the dentist for losses for which they would not normally be responsible. For example, if an insurance company is at least partially at fault for a situation that results in malpractice, a dentist may be solely liable. Dentists should carefully review these contracts and consult legal counsel to understand the legal and financial implications.

When negotiating contract terms, dentists should consider the following strategies:

- Limit the agreement to two years to allow for future renegotiations.

- Add language requiring the insurance company to notify the dentist in writing before establishing any third-party arrangements and allow the dentist to opt out.

- Clarify which plans or products the dentist will be expected to participate in and ensure they have the opportunity to decline individual plans.

- Include a reciprocal hold-harmless clause requiring the insurance company to pay the dentist for any losses incurred due to the company's acts or omissions.

By carefully reviewing and negotiating contract terms, dentists can protect themselves from unnecessary liability and ensure a better understanding of their expected participation and financial impact.

COBRA Insurance: Federal Program or Private Option?

You may want to see also

Frequently asked questions

No, it is the patient's responsibility to check their insurance coverage and present their insurance card before getting any work done. However, most dental offices will verify your insurance, provide you with an estimate, and file a claim on your behalf as a courtesy.

An "in-network" dentist has an agreement with your insurance company regarding the price of procedures, whereas an "out-of-network" dentist does not.

PPO stands for Preferred Provider Organization. PPO insurance allows you to go to any dentist you want, but some dentists may be "out-of-network".

DHMO stands for Dental Health Maintenance Organization. With DHMO insurance, you are assigned a specific dentist and/or office. This type of insurance tends to be less expensive than PPO.

You should always inform your dentist of any changes to your insurance information before your appointment. This will help the dentist communicate what your out-of-pocket expenses will be and streamline the billing process.