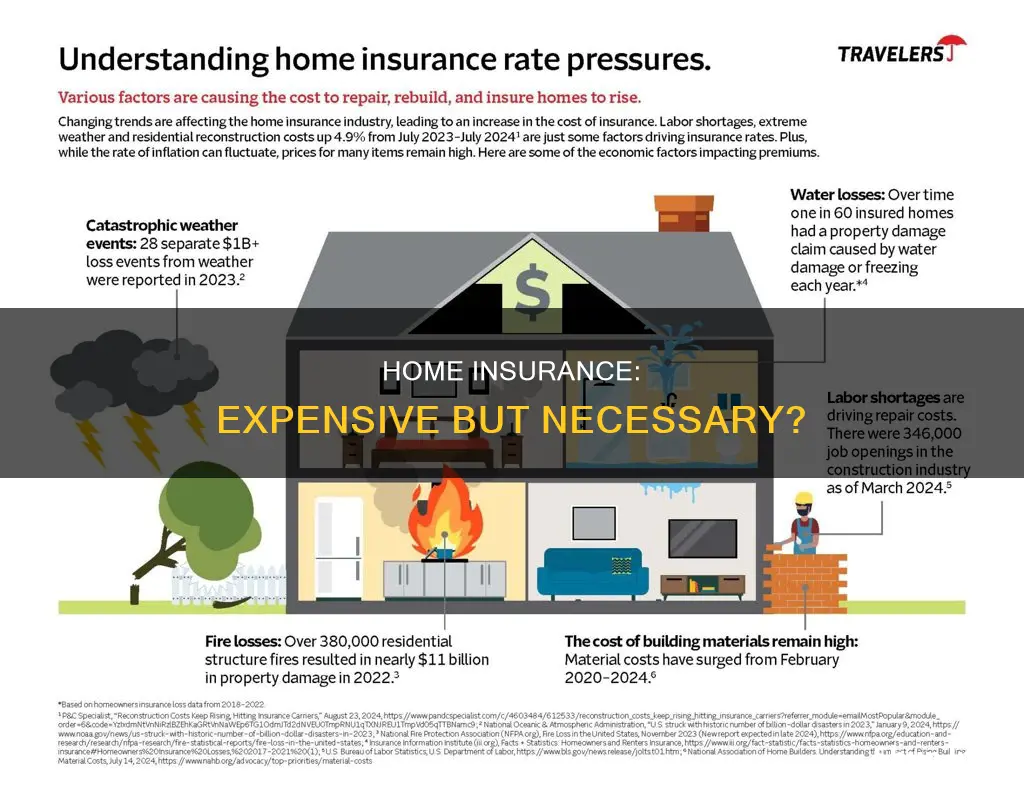

Homeowners insurance premiums have been rising significantly across the United States, and this trend is expected to continue. The national average cost of home insurance is $2,466 per year for a policy with a $300,000 dwelling limit, but rates vary widely depending on location and other factors. For example, in 2024, the average annual cost of homeowners insurance in Vermont was $918, while in Florida, it was nearly $11,000. The cost of homeowners insurance is influenced by factors such as the location, age, and square footage of the home, the cost of building materials and labour, and the risk of weather-related damage.

Explore related products

$14.99 $14.99

What You'll Learn

- Home insurance rates vary across the country, with Vermont homeowners paying the least and Florida homeowners paying the highest

- The cost of insurance is influenced by the risk of severe weather events, with states prone to hurricanes, wildfires, and tornadoes paying more

- Inflation and rising homebuilding costs are contributing to higher insurance rates

- Credit scores can impact insurance rates, with poor credit potentially resulting in higher premiums

- Homeowners can take preventive measures, such as installing protective devices, to reduce insurance costs

![]()

Home insurance rates vary across the country, with Vermont homeowners paying the least and Florida homeowners paying the highest

Home insurance rates vary significantly across the United States, with several factors influencing the cost of premiums. Notably, Vermont homeowners pay the least for insurance, while Florida homeowners pay the highest rates in the country.

Vermont has the lowest homeowner insurance rates in the US, with an average annual premium of around $799 to $1,248, which is significantly below the national average. Vermonters pay approximately $67 per month for their home insurance. In contrast, Florida has the highest home insurance rates, with homeowners paying a whopping $481 per month or $5,770 per year on average.

The disparity in insurance costs between states is influenced by various factors, including the risk of natural disasters, the cost of living, and the frequency of severe weather events. Florida's high insurance rates can be attributed to its vulnerability to hurricanes, tornadoes, and other natural disasters. The state's location makes it prone to severe weather, leading to skyrocketing insurance premiums. Additionally, the threat of natural disasters plays a significant role in determining home insurance costs. States with a higher risk of widespread home damage from disasters tend to have higher insurance rates.

Other factors that contribute to the variation in insurance rates across the country include the location, age, and square footage of the home, the chosen deductibles and policy limits, and the cost of building materials. Inflation has also impacted insurance rates, as repairing and rebuilding houses has become more expensive. Furthermore, insurance rates are expected to continue rising due to the increasing frequency and severity of climate change-induced disasters.

It is worth noting that insurance rates are not static and can fluctuate over time. Homeowners should regularly review their insurance policies and consider shopping around for the best rates. Additionally, maintaining a good credit score can positively impact insurance premiums, as insurers in many states use credit-based insurance scores in their pricing.

Navigating the Path to Becoming a Farmers Insurance Vendor

You may want to see also

Explore related products

![]()

The cost of insurance is influenced by the risk of severe weather events, with states prone to hurricanes, wildfires, and tornadoes paying more

The risk of severe weather events is heightened by climate change, which has increased the frequency and severity of hurricanes, wildfires, and tornadoes. As a result, insurance payouts for losses sustained in these disasters have increased, and the uncertainty about future losses has grown. This has led to higher insurance premiums in high-risk areas. For example, in 2023, residents of wildfire-prone Arizona saw an average spike of 21.8% in their insurance rates, while Texans experienced a 23.3% increase.

The location of a property is a significant factor in determining the cost of homeowners insurance. States with a higher risk of natural disasters, such as Nebraska, Louisiana, Florida, Oklahoma, and Kansas, tend to have higher insurance premiums. On the other hand, states with a lower risk of natural disasters, such as Vermont, Alaska, and Delaware, have lower insurance costs.

The impact of severe weather events on insurance rates is also evident in Tornado Alley, where insurance costs have been soaring. In Kentucky, which was recently affected by a deadly tornado, insurance premiums have increased by 35% in recent years. Similar increases have been observed in Nebraska (35%), Arkansas (34%), Minnesota (32%), and Texas, Colorado, and Iowa (27%).

The frequency and severity of hailstorms have also contributed to rising insurance costs in these regions, as hail has become an increasingly significant contributor to insurance claims. The average cost of homeowners insurance in the United States is about $2,110 per year for $300,000 worth of dwelling coverage, but rates can vary significantly by state and the specific location within a state.

AAA Homeowners Insurance: Legit or a Scam?

You may want to see also

Explore related products

![]()

Inflation and rising homebuilding costs are contributing to higher insurance rates

Inflation and rising homebuilding costs are major contributors to higher insurance rates. Inflation has had a significant impact on the cost of construction materials and labour, with construction trade services labour costs rising by 40% between June 2019 and June 2024. This has made it more expensive for insurers to rebuild or repair homes after disasters, leading to higher premiums for homeowners.

In addition, the increasing frequency and severity of climate-related disasters, such as hurricanes, wildfires, and tornadoes, have resulted in more substantial financial losses for insurers. From 2018 to 2022, insurers in the highest-risk ZIP codes paid $24,000 on average in claims, compared to $19,000 for the lowest-risk areas. As a result, insurers charge higher rates in these high-risk areas to ensure they have enough reserves to handle a large volume of claims.

The combination of inflation and rising homebuilding costs has led to a perfect storm of increasing insurance rates. Homeowners insurance premiums have risen significantly across the nation, with an average annual increase of 12% in 2023 and an additional 6.9% in the first half of 2024, far exceeding the historical average of 5% yearly increases.

Furthermore, certain states have been disproportionately affected by rising insurance costs. For example, Utah experienced a staggering 59% increase in insurance premiums between 2021 and 2025, with the primary factors being the construction of homes in wildfire-prone areas and the insurance market adjusting for inflation. Other states, such as Florida, Louisiana, Oklahoma, Kentucky, and Nebraska, are also among the most expensive for homeowners insurance due to their vulnerability to natural disasters.

The impact of inflation and rising homebuilding costs on insurance rates has significant implications for homeowners, insurers, and local governments. As insurance becomes more costly and challenging to obtain, it affects housing expenses, property values, and tax bases, highlighting the urgent need for regulatory intervention to protect consumers and ensure the availability of affordable insurance coverage.

Farmers Insurance Golf: Unraveling the Wednesday Start Mystery

You may want to see also

Explore related products

![]()

Credit scores can impact insurance rates, with poor credit potentially resulting in higher premiums

Homeowners insurance premiums have been rising significantly across the United States and are expected to continue doing so. Several factors contribute to the variability in insurance rates, including the location, age, and square footage of the home, the cost of building materials, and the risk of natural disasters.

One critical factor that can significantly impact insurance rates is an individual's credit score. Insurers in 46 states are legally permitted to use a credit-based insurance score when determining the pricing of homeowners' insurance premiums. This means that individuals with poor credit scores may face higher insurance premiums.

The impact of credit scores on insurance rates is not limited to homeowners' insurance but also extends to auto insurance. Studies have shown that 92% of insurers consider credit scores when calculating auto insurance premiums.

While credit scores can influence insurance rates, it is important to note that insurance companies cannot use certain events as a basis for denying coverage or charging higher premiums. These events include major illnesses or injuries, the death of a close family member, temporary job loss, divorce, or identity theft. Individuals who believe their credit scores have been affected by such events can request reconsideration from the insurance company.

To mitigate the impact of poor credit scores on insurance rates, individuals should regularly review their credit reports to identify and correct any errors. Additionally, it is advisable to manage debt wisely, avoid taking on excessive credit card debt, and pay bills on time. By improving their credit scores, individuals can potentially lower their insurance premiums.

State Farm: Self-Storage Insurance Coverage Explained

You may want to see also

Explore related products

![]()

Homeowners can take preventive measures, such as installing protective devices, to reduce insurance costs

Homeowners insurance is becoming increasingly expensive due to inflation and the rising costs of repairing and rebuilding houses. The price of construction materials and labour has increased, and natural disasters such as hurricanes, wildfires, and floods are becoming more frequent and destructive. As a result, insurance companies are charging higher rates in high-risk areas to ensure they have enough reserves to handle a large volume of claims.

However, there are preventive measures that homeowners can take to reduce their insurance costs. One way is to install protective devices such as smoke detectors, fire extinguishers, and security systems. Many insurance companies offer discounts for homes with upgraded safety features. Additionally, homeowners can consider raising their deductible, which is the amount they pay when making a claim. A higher deductible can result in lower insurance premiums, with potential savings of up to 25% according to the Insurance Information Institute.

Another factor that affects insurance costs is credit history. Insurers in 46 states use credit-based insurance scores to price homeowners' insurance premiums. Homeowners with poor credit may pay significantly more for insurance, with NerdWallet's rate analysis showing an average increase of 71% compared to those with good credit. Therefore, it is essential to establish a solid credit history by paying bills on time, keeping credit card balances low, and regularly checking credit reports for errors.

Location also plays a significant role in determining insurance costs. Homeowners in disaster-prone areas, such as states vulnerable to tornadoes, hurricanes, or wildfires, typically face higher insurance rates. Additionally, the age and square footage of a home can impact insurance costs, with older and larger homes requiring more coverage. By being mindful of these factors and taking preventive measures, homeowners can help reduce their insurance costs.

Finally, it is worth noting that insurance rates can vary between insurance companies. Homeowners should shop around and compare rates from different insurers to find the best deal. They can also ask about available discounts, such as those offered for long-term policyholders or for bundling home and auto policies with the same insurer. By being proactive and informed, homeowners can take control of their insurance costs and ensure they are getting the best coverage for their needs.

Home Insurance: Does It Cover Your Boat?

You may want to see also

Frequently asked questions

Homeowners insurance rates are rising due to inflation and the increasing costs of repairing and rebuilding houses. The location of your home is a big factor in determining how much you'll pay for insurance. If you live in an area that's prone to severe weather events, you'll likely pay more for insurance.

The national average cost of home insurance is $2,466 per year for a policy with a $300,000 dwelling limit. However, rates vary by state, with some states having much higher or lower average costs.

In addition to location, the age, size, and features of your home, as well as the cost of building materials and labour, can impact the cost of homeowners insurance. Your credit score can also affect your insurance premiums in most states.

You can save money on homeowners insurance by installing protective devices, such as smoke detectors and security systems. Bundling your home insurance with other policies, such as car insurance, can also help lower your premiums. Shopping around and comparing quotes from different companies can also help you find the best rates.