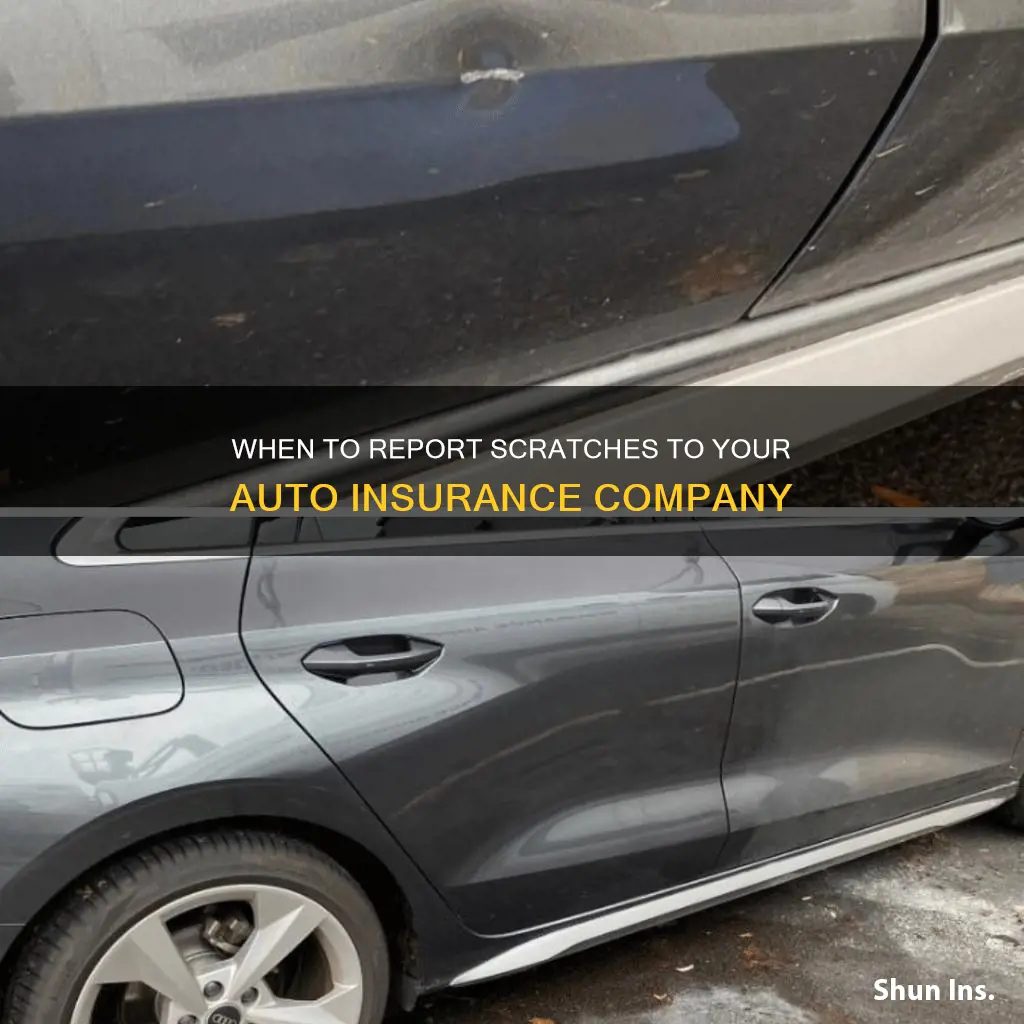

Whether or not you should report a scratch to your insurance provider depends on several factors. These include the severity of the scratch, whether you were at fault, and the type of insurance coverage you have. If the scratch is minor, it may be more cost-effective to pay for repairs out of pocket rather than risk an increase in your insurance rates. However, if the scratch is deep or extensive, it may be worth filing a claim, especially if the damage was caused by another driver or an act of vandalism. It's important to review your insurance policy to understand what types of scratches are covered and whether there is a deductible that you would need to pay. Additionally, consider getting repair estimates from a body shop and weighing the potential costs and benefits before deciding whether to report the scratch to your insurance company.

| Characteristics | Values |

|---|---|

| When to report a scratch to insurance | If the scratch was caused by a covered peril in your policy, like a car accident or vandalism. If you have comprehensive coverage, you need to file a police report, and then a claim with your insurance carrier. |

| Repair costs | If the repair costs are less than your car insurance deductible, pay for the damage out of pocket. If the damage is more extensive and costly, file a claim. |

| Collision coverage | Collision coverage includes damage caused by a collision with another car or object. Collision coverage also includes single-car accidents like hitting a guardrail or a curb. |

| Comprehensive coverage | Comprehensive coverage includes unexpected damage that is outside of your control and isn't caused by a collision with another vehicle or object. Covered events may include acts of vandalism, hitting a deer, a tree falling on your car, or damage to your windshield from a rock. |

| Minor scratches | If the damage is minor, it may be smarter to pay out of pocket. Filing small claims can cause your rates to increase. |

| Major scratches | Major cosmetic damage includes large dents, deep scratches, cracked windshields, or significant body panel damage. These issues may lower your car's resale value or lead to further deterioration if left unaddressed. Depending on the severity, they may be worth repairing through insurance. |

Explore related products

What You'll Learn

![]()

Weigh the costs: paying out of pocket vs filing a claim

When deciding whether to pay out of pocket or file a claim, it's important to consider the costs involved in both options. Paying for repairs out of pocket can help you avoid a potential increase in your insurance rates, which is a common outcome of filing a claim. Additionally, if the repairs cost less than your deductible, it is often more cost-effective to pay for them yourself rather than filing a claim.

For example, if the repairs cost $1,000 and your deductible is $100, you would only need to pay the deductible amount if you file a claim, resulting in a net cost of $100. On the other hand, if you choose to pay out of pocket, you will be responsible for the full $1,000. In this case, filing a claim would be more financially advantageous.

However, it's important to keep in mind that filing multiple claims within a short period can lead to issues with insurance renewal. Some insurance companies may not renew your policy if you have filed too many claims. Therefore, paying for minor repairs out of pocket can sometimes be a wiser decision to maintain eligibility for insurance renewal.

Another factor to consider is the severity of the scratch. Minor scratches may be repairable through DIY methods or minor touch-ups, eliminating the need to file a claim. On the other hand, deeper scratches that affect the paint may require professional repairs to prevent corrosion and rust. In such cases, filing a claim might be more appropriate, especially if the repairs are likely to be costly.

Ultimately, the decision to pay out of pocket or file a claim depends on various factors, including the cost of repairs, your deductible amount, the potential impact on insurance rates, and the severity of the scratch. It is recommended to review your insurance policy, obtain repair estimates, and carefully weigh the pros and cons before making a decision.

Reporting Cobra Insurance: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Comprehensive coverage and collision coverage

When deciding whether to report a scratch to your insurance, it's important to understand the differences between comprehensive coverage and collision coverage. Both are optional but important protections for your vehicle, and they differ in the type of incident they cover.

Comprehensive coverage includes damage to your vehicle from unexpected non-collision incidents. This includes theft, animal damage, falling trees, weather damage, vandalism, and more. For example, if your car is vandalised and scratched, comprehensive coverage would apply. This type of coverage usually comes with a deductible, which must be covered by the policyholder before the insurance coverage begins. Comprehensive claims do not typically increase insurance rates as much as collision claims because they are generally less costly for insurance companies and car owners have less control over the causes of these claims.

Collision coverage, on the other hand, is for damage to your car caused by accidents involving a collision with another vehicle or object. This could include hitting a guardrail, a curb, a mailbox, or another car. Collision coverage also includes single-car accidents. For example, if you scrape against a pole and scratch your car, collision coverage would apply. Collision coverage also comes with a deductible that you are responsible for if you file a claim. The cost of repairs will depend on what part of your car was scratched and how deep the scratches are.

The decision to report a scratch to insurance depends on several factors, including the cost of repairs, your deductible, and the potential increase in your insurance rates. If the repair costs are less than your deductible, it is often more cost-effective to pay for the damage yourself rather than filing a claim. Additionally, filing a claim may cause your insurance rates to increase, so it is important to weigh the costs and benefits before deciding.

It is worth noting that comprehensive and collision coverage can be purchased together, and some insurers may require this. The coverage limits for both are determined by the value of the vehicle and the deductible amounts selected. Ultimately, the decision to purchase comprehensive or collision coverage, or both, depends on your budget, your vehicle's value, and your risk assessment.

Family Leave Insurance: Tax Reporting Guide

You may want to see also

Explore related products

![]()

Vandalism and acts of God

When it comes to car insurance, vandalism and acts of God are typically covered under comprehensive coverage. Comprehensive coverage includes damage to your vehicle caused by anything other than a collision, such as natural disasters, auto theft, and vandalism. While insurance policies may not use the term "acts of God," they may cover them under this type of coverage. Examples of acts of God include natural disasters like hail, flooding, wildfires, and fallen trees. It's important to note that insurance companies will investigate other causes of damage before approving a claim. For instance, if a tree falls on your car during a storm, it would likely be covered. However, if the tree was rotten and should have been cut down, negligence could be considered a contributing factor, and your claim may be denied.

Comprehensive coverage for car insurance often includes a deductible, which is the amount you must pay before insurance coverage takes effect. The deductible can range from $100 to $2,000, depending on the insurer. When deciding whether to file a claim for vandalism or an act of God, consider the cost of repairs and whether it exceeds your deductible. If the repair costs are less than your deductible, it may be more cost-effective to pay for the repairs yourself to avoid potential increases in your insurance rates.

Vandalism, in the context of insurance, refers to intentional damage or destruction of property without theft. Vandalism and malicious mischief insurance is a type of coverage that protects property owners from losses due to intentional damage caused by vandals. This type of insurance is commonly included in basic commercial and homeowner policies, especially for properties that are unoccupied during certain periods, such as churches and schools. It is essential to review your insurance policy carefully, as some types of vandalism, such as damage caused by ex-partners or named insured individuals, may not be covered.

When filing a claim for vandalism on your vehicle, it is generally recommended to obtain a police report. This helps support your claim and demonstrates that the damage was a result of vandalism. Additionally, comprehensive coverage may be required to insure against acts of vandalism. It is worth noting that standard car insurance typically does not cover cosmetic damage, such as minor scratches, dents, or paint damage, unless specific coverage options like Progressive Vehicle Protection are added to your policy.

Farmers Insurance: Exploring Their Cat Insurance Options

You may want to see also

Explore related products

$18.95 $19.95

![]()

When to report an accident

If you have been in an accident, it is generally recommended to report it to your insurance company as soon as possible. This is because failing to report an accident may violate the terms of your contract and put your coverage at risk. Additionally, it makes it more challenging for your insurance provider to defend you if the other party claims you are at fault and tries to collect damages.

However, it's important to consider the costs and benefits of reporting minor accidents, such as scratches, to your insurance. Filing a claim can cause your insurance rates to increase, and these increases can last for an average of three years. Therefore, if the repair costs are less than your deductible, it may be more cost-effective to pay for the damage yourself. This is especially true if the damage is minor, as filing a claim for minor cosmetic issues is often denied by insurance companies.

On the other hand, if the damage is more severe or costly, it may be worth filing a claim. This is especially true if the damage is covered by your insurance policy, such as in the case of a collision or comprehensive coverage. Collision coverage protects your vehicle from damage caused by a collision with another car or object, while comprehensive coverage includes unexpected damage outside of your control, such as vandalism. If you have comprehensive coverage, you will likely need to file a police report before filing a claim with your insurance carrier.

It's also important to consider the circumstances of the accident when deciding whether to report it to your insurance company. For example, if you accidentally scratched someone else's car, it's generally recommended to contact your insurance provider. This is because causing damage and failing to report it can result in legal consequences, such as tickets or jail time. Additionally, if you don't report the accident and the other party files a claim against you, your insurance company may deny you coverage.

Home Insurance: 80% Affordable?

You may want to see also

Explore related products

![]()

The effect on insurance rates

When deciding whether to report a scratch to an insurance company, it is important to consider the effect it may have on insurance rates. Filing a claim can lead to a rate increase, particularly if the damage was a result of an accident caused by the policyholder. In such cases, insurance rates may increase and remain higher for an average of three years. However, this is dependent on the insurance company's policies, with some offering accident forgiveness programs.

If the scratch is minor, it may be more cost-effective to pay for repairs out of pocket, as filing a claim may result in higher costs in the long run. This is because small claims can cause insurance rates to increase, and the final cost of repairs may exceed the initial estimate. Additionally, standard insurance policies do not typically cover minor cosmetic issues such as scratches, dents, and overall paint damage resulting from general wear and tear. Therefore, filing a claim for such issues would likely be denied.

On the other hand, if the scratch is major or caused by another driver, filing a claim can help cover the cost of repairs. Comprehensive and collision coverage, which are optional additions to insurance policies, can cover repairs for scratches resulting from covered perils such as vandalism or a collision. However, both types of coverage usually include a deductible, and if the repair costs are less than this amount, filing a claim may not be worthwhile.

It is important to review the specific details of an insurance policy before filing a claim, as coverage for scratches depends on the policy's terms and conditions. Additionally, providing clear photos, a detailed incident report, and supporting evidence can help strengthen a claim. While filing a claim may result in a rate increase, not reporting an accident may violate the terms of the contract and put coverage at risk. Therefore, it is essential to carefully consider the circumstances surrounding the scratch before deciding whether to report it to the insurance company.

House-Flipping Insurance: Essential Coverage for Startups

You may want to see also

Frequently asked questions

It depends on the severity of the scratch and whether you have comprehensive or collision coverage. Deeper scratches are more likely to need repair to prevent rust. If you have comprehensive coverage, you should file a police report and then a claim with your insurance carrier. If you have collision coverage, you may need to pay a deductible before insurance covers the rest.

Yes, if you are driving someone else's car and it gets scratched, you can still file a claim and your liability insurance should cover you. However, the owner of the car will have to contact their insurer and they may pay for the damages too.

Yes, if you caused an accident that led to a scratch on your car, you should report it to your insurance company. Not doing so may violate the terms of your contract and put your coverage at risk.

Yes, if someone else caused an accident that led to a scratch on your car, you should file a claim with their insurance company. If you don't, and the other person later files a claim against you, your insurance company might deny you coverage.

Yes, if you suspect your car was scratched as an act of vandalism, you should file a police report and then a claim with your insurance carrier. Comprehensive coverage includes unexpected damage that is outside of your control and is usually required for vandalism claims.