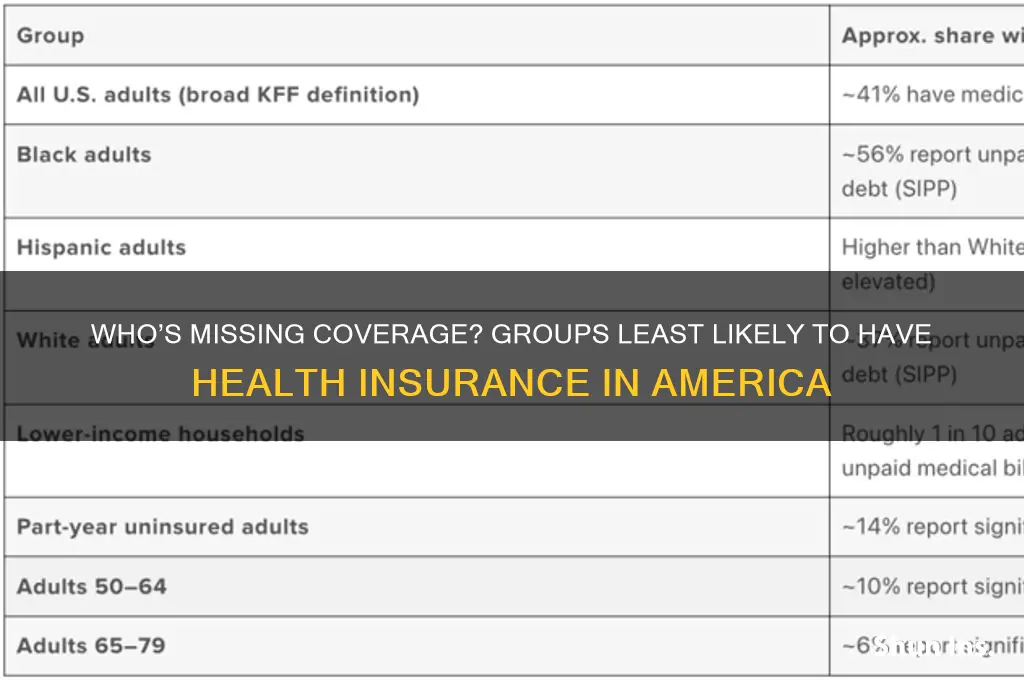

In the United States, disparities in health insurance coverage persist, with certain demographic groups being disproportionately less likely to have health insurance. Factors such as income level, employment status, age, and race/ethnicity play significant roles in determining access to coverage. Low-income individuals, part-time or gig workers, young adults, and minority communities, particularly Hispanic and Native American populations, are among those least likely to have health insurance. These disparities are often exacerbated by gaps in employer-sponsored insurance, limited eligibility for public programs like Medicaid, and the higher costs associated with private plans, leaving millions of Americans vulnerable to financial and health-related hardships.

Explore related products

What You'll Learn

- Young adults (26-34): Least insured due to job instability and lack of employer-provided coverage

- Low-income workers: Often ineligible for Medicaid but unable to afford private insurance

- Part-time employees: Rarely offered health benefits, leaving many without coverage options

- Self-employed individuals: High costs of private plans deter many from purchasing insurance

- Undocumented immigrants: Excluded from most public and private insurance programs nationwide

![]()

Young adults (26-34): Least insured due to job instability and lack of employer-provided coverage

Young adults aged 26 to 34 are disproportionately uninsured, with job instability and the absence of employer-provided health coverage as primary culprits. This age group often finds itself in a precarious employment landscape, juggling part-time gigs, freelance work, or entry-level positions that rarely offer health benefits. According to the Kaiser Family Foundation, nearly 14% of adults in this age bracket lack health insurance, compared to just 8% of those aged 35 to 50. The transition from parental coverage at age 26, coupled with the financial strain of early adulthood, leaves many in this demographic vulnerable to medical debt or forgoing care altogether.

Consider the case of a 28-year-old freelance graphic designer earning $35,000 annually. Without access to an employer-sponsored plan, their only options are individual marketplace plans, which can cost upwards of $300 per month for a mid-tier policy. For someone with fluctuating income, this expense is often deemed non-essential, especially when weighed against rent, student loans, and groceries. The Affordable Care Act (ACA) subsidies may help, but eligibility thresholds often exclude those in the "coverage gap"—earning too much for Medicaid but too little for substantial subsidies. This financial tightrope leaves many young adults uninsured, despite their desire for coverage.

To address this gap, young adults should explore all available options systematically. First, check if your income qualifies for Medicaid in your state, as eligibility varies. For instance, in New York, individuals earning up to $18,000 annually may qualify, while in Texas, the threshold is significantly lower. Second, use the ACA marketplace to compare plans during open enrollment (November 1 to January 15) or after a qualifying life event, such as job loss. Tools like Healthcare.gov’s subsidy calculator can estimate costs based on income. Third, consider short-term health plans as a temporary solution, though they often exclude pre-existing conditions and lack comprehensive coverage.

A comparative analysis reveals that young adults in this age group are not inherently averse to insurance but are trapped in a system that fails to meet their needs. Unlike older workers, who often benefit from decades of employer-provided coverage, 26- to 34-year-olds are more likely to work in industries like hospitality, retail, or the gig economy, where benefits are scarce. For example, only 35% of workers in the hospitality sector receive employer-sponsored insurance, compared to 70% in finance. This disparity underscores the need for policy reforms, such as expanding Medicaid eligibility or mandating benefits for part-time workers, to bridge the coverage gap.

In conclusion, the lack of insurance among young adults aged 26 to 34 is a systemic issue rooted in employment trends and policy shortcomings. Practical steps, such as leveraging Medicaid, ACA subsidies, and short-term plans, can provide temporary relief, but long-term solutions require addressing the root causes of job instability and employer-provided coverage gaps. Until then, this demographic will remain disproportionately vulnerable, highlighting the urgent need for reform in both labor and healthcare markets.

Understanding Stop Loss Limits in Health Insurance: A Comprehensive Guide

You may want to see also

Explore related products

![]()

Low-income workers: Often ineligible for Medicaid but unable to afford private insurance

Low-income workers in the United States often find themselves in a precarious health insurance gap. Despite their financial struggles, many earn too much to qualify for Medicaid, the government-funded health insurance program for low-income individuals and families. This eligibility cliff leaves them without a safety net, as private insurance premiums and out-of-pocket costs are frequently beyond their reach.

A 2022 study by the Kaiser Family Foundation found that 28% of uninsured adults were in this very situation, earning too much for Medicaid but not enough to comfortably afford private coverage. This translates to millions of Americans, often working full-time jobs, facing the constant threat of medical debt and delayed or forgone care due to cost concerns.

Consider a single mother working two minimum wage jobs. Her income might exceed the Medicaid eligibility threshold in her state, yet she struggles to pay rent, utilities, and childcare, leaving little for health insurance premiums. A single unexpected medical bill could push her into financial ruin. This scenario highlights the cruel irony: those who need health insurance the most are often the least likely to have it.

The consequences of this gap are dire. Uninsured individuals are more likely to delay preventive care, leading to more severe and costly health issues down the line. They are also more likely to forgo necessary medications and treatments, impacting their overall health and well-being. This not only affects individuals but also strains the healthcare system as a whole, as untreated conditions often lead to emergency room visits, the most expensive form of care.

Addressing this gap requires a multi-pronged approach. Expanding Medicaid eligibility in all states would be a significant step, ensuring that more low-income workers have access to affordable coverage. Additionally, subsidies for private insurance premiums and out-of-pocket costs could make coverage more attainable for those slightly above the Medicaid threshold. Finally, promoting awareness of existing programs and resources, such as community health centers and prescription assistance programs, can help bridge the gap for those currently uninsured.

Health Insurance and Taxable Income: What You Need to Know

You may want to see also

Explore related products

![]()

Part-time employees: Rarely offered health benefits, leaving many without coverage options

Part-time workers, often defined as those employed fewer than 30 hours per week, face a stark reality in the American healthcare system: they are among the least likely to receive employer-sponsored health insurance. This disparity stems from federal regulations like the Affordable Care Act (ACA), which mandates health coverage only for employees working 30 hours or more weekly. As a result, an estimated 24% of part-time workers lack health insurance, compared to just 8% of full-time employees, according to the Kaiser Family Foundation. This gap leaves millions vulnerable, particularly in industries like retail, hospitality, and food service, where part-time roles dominate.

Consider the case of Maria, a 28-year-old part-time barista working 25 hours a week at a coffee shop. Her employer, like many small businesses, does not offer health benefits to part-time staff. Maria earns too much to qualify for Medicaid in her state but too little to afford private insurance premiums, which average $456 per month for individual plans. Without coverage, she delays preventive care, risking undetected health issues that could escalate into costly emergencies. Maria’s situation is not unique; it reflects the systemic exclusion of part-time workers from the safety net of employer-provided healthcare.

The lack of health benefits for part-time employees perpetuates economic and health inequalities. Without insurance, these workers are more likely to forgo necessary medical care, leading to poorer health outcomes and higher out-of-pocket costs when issues arise. For instance, a study by the Commonwealth Fund found that uninsured adults are three times more likely to skip needed care due to cost. This not only harms individual well-being but also strains public health systems, as untreated conditions often result in emergency room visits funded by taxpayers. Employers, too, suffer indirectly, as unhealthy workers may experience reduced productivity and increased absenteeism.

To address this gap, part-time workers can explore alternative coverage options, though each comes with limitations. First, the ACA’s health insurance marketplace offers subsidized plans for those earning between 100% and 400% of the federal poverty level (FPL), which in 2023 ranges from $14,580 to $58,320 for an individual. However, subsidies phase out quickly, leaving those just above the threshold with high premiums. Second, short-term health plans provide temporary coverage at lower costs but exclude pre-existing conditions and essential benefits like maternity care. Lastly, joining a spouse’s employer plan, if available, can be a viable but not universal solution.

Advocacy for policy changes is critical to closing this coverage gap. Expanding Medicaid in non-expansion states would immediately benefit millions of low-income part-time workers. Additionally, revising the ACA’s employer mandate to include part-time employees or incentivizing businesses to offer prorated benefits could significantly reduce uninsured rates. Until such changes occur, part-time workers must navigate a fragmented system, balancing limited options with financial constraints. Their struggle underscores the need for a healthcare system that prioritizes accessibility over employment status.

Las Vegas Hospitals: Understanding Your Medicaid Blue Cross Options

You may want to see also

Explore related products

![]()

Self-employed individuals: High costs of private plans deter many from purchasing insurance

Self-employed individuals often face a stark financial dilemma when it comes to health insurance. Unlike traditional employees, they lack employer-sponsored plans, leaving them to navigate the costly landscape of private insurance on their own. This financial burden is a primary reason why self-employed Americans are among the least likely to have health coverage.

A 2022 study by the Kaiser Family Foundation revealed that 21% of self-employed workers were uninsured, compared to only 8% of those with employer-based coverage. This disparity highlights the significant barrier high premiums pose for this demographic.

Consider the case of Sarah, a freelance graphic designer. Her monthly income fluctuates, making it difficult to commit to a fixed premium. Private plans in her area start at $400 per month, a substantial chunk of her earnings. She’s forced to gamble, hoping to stay healthy while saving for potential medical emergencies. This precarious situation is shared by countless self-employed individuals, who are often priced out of the very protection they need.

The high cost of private plans isn’t just a financial strain; it’s a health risk. Without insurance, self-employed individuals are less likely to seek preventive care, delaying treatment for potential health issues until they become more serious and expensive. This not only impacts their well-being but also contributes to higher healthcare costs for everyone in the long run.

Addressing this issue requires a multi-pronged approach. Policymakers could explore subsidies or tax credits specifically targeted at self-employed individuals, making private plans more affordable. Expanding access to health savings accounts (HSAs) with higher contribution limits could also provide a safety net for unexpected medical expenses. Additionally, encouraging the development of more affordable, tailored insurance plans designed for the self-employed could increase coverage rates.

Does Oscar Health Insurance Cover Enbrel? A Comprehensive Guide

You may want to see also

Explore related products

![]()

Undocumented immigrants: Excluded from most public and private insurance programs nationwide

Undocumented immigrants in the United States face a stark reality: they are systematically excluded from most public and private health insurance programs. This exclusion is not an oversight but a deliberate policy decision with profound implications for both individuals and communities. The Affordable Care Act (ACA), for instance, explicitly bars undocumented immigrants from purchasing health plans through the marketplace, even if they use their own money. Similarly, Medicaid and the Children’s Health Insurance Program (CHIP) are off-limits, except in rare cases where states have opted to use their own funds to cover limited groups, such as pregnant women or children. This leaves millions without a safety net, forcing them to rely on emergency care, free clinics, or going without treatment altogether.

Consider the practical consequences of this exclusion. Undocumented immigrants often work in high-risk industries like agriculture, construction, and food service, where injuries and illnesses are common. Without insurance, a workplace accident or chronic condition can lead to financial ruin. For example, a broken bone treated in an emergency room can cost upwards of $16,000, a sum that most undocumented workers cannot afford. This financial burden not only affects individuals but also strains safety-net hospitals, which are legally required to provide emergency care regardless of insurance status. The result is a cycle of untreated health issues, delayed care, and higher costs for everyone.

From a policy perspective, the exclusion of undocumented immigrants from health insurance programs is both shortsighted and counterproductive. Healthy communities depend on the well-being of all members, regardless of legal status. When undocumented immigrants lack access to preventive care, treatable conditions like diabetes or hypertension often escalate into costly emergencies. Moreover, during public health crises, such as the COVID-19 pandemic, excluding this population from healthcare access undermines broader efforts to control disease spread. States like California have recognized this by expanding coverage to certain undocumented groups, but such initiatives remain the exception rather than the rule.

Advocates argue that expanding health insurance access to undocumented immigrants is not just a moral imperative but also an economic one. A 2020 study by the Commonwealth Fund found that providing coverage to undocumented immigrants could reduce uncompensated care costs by billions of dollars annually. Practical steps toward inclusion could include allowing undocumented individuals to purchase unsubsidized plans through the ACA marketplace or expanding state-funded programs. Employers could also play a role by offering private insurance options, though this would require federal policy changes to remove current restrictions.

In conclusion, the exclusion of undocumented immigrants from health insurance programs is a pressing issue that demands attention. It is a policy choice that perpetuates inequality, harms public health, and incurs unnecessary costs. By rethinking this exclusion and exploring inclusive solutions, policymakers can create a healthier, more equitable society for all. The first step is acknowledging that healthcare is a human right, not a privilege tied to legal status.

Uncovering Health Insurance Fraud: Essential Steps to Report and Protect Yourself

You may want to see also

Frequently asked questions

Young adults aged 18-24 are the least likely to have health insurance, often due to lower incomes, part-time employment, or transitioning between school and work.

Low-income individuals, particularly those earning below the federal poverty level, are the least likely to have health insurance, as they may not qualify for Medicaid in non-expansion states and cannot afford private plans.

Hispanic Americans are the least likely to have health insurance, primarily due to factors such as lower income, immigration status, and limited access to employer-sponsored coverage.