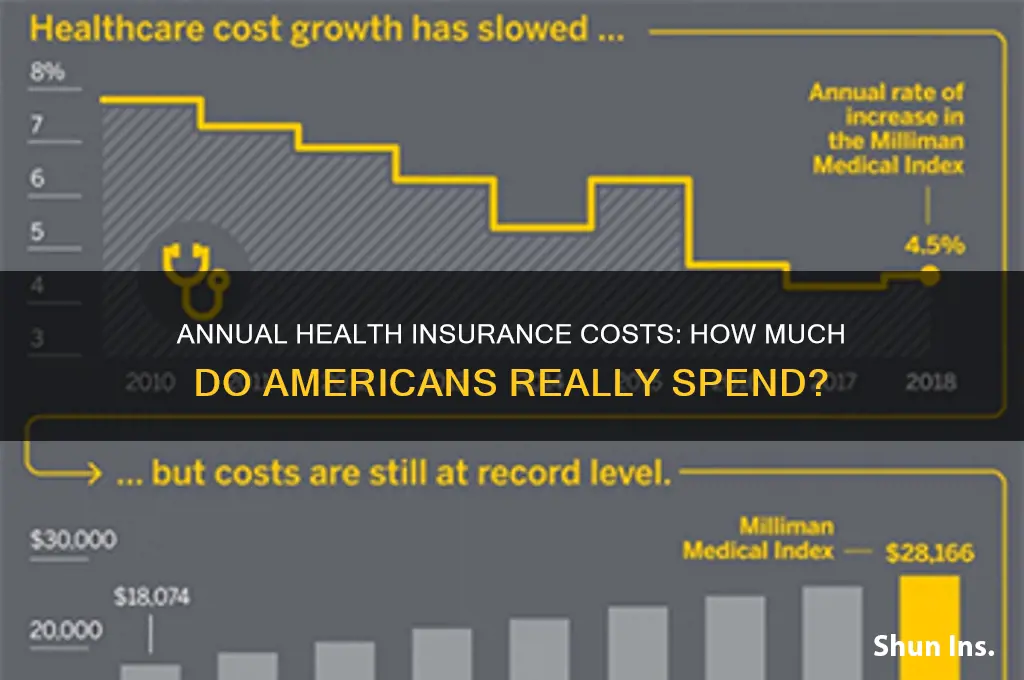

Every year, Americans collectively spend a staggering amount on health insurance, reflecting the high costs of healthcare in the United States. In 2022, the average annual premium for employer-sponsored family coverage exceeded $22,000, with employees contributing over $6,000 of that amount. For individual plans, the average premium was around $7,900 annually. These figures do not include out-of-pocket expenses such as deductibles, copayments, and coinsurance, which can add thousands more to an individual’s or family’s healthcare costs. The rising expenses highlight the financial burden of health insurance on American households, making it a critical issue in discussions about healthcare affordability and policy reform.

| Characteristics | Values |

|---|---|

| Average Annual Premium (2023) | $8,435 for single coverage, $23,968 for family coverage (employer-sponsored) |

| Average Annual Premium (Individual Market, 2023) | $514 per month ($6,168 annually) for a 40-year-old buying a benchmark plan |

| Percentage of Income Spent on Premiums (Employer-Sponsored) | 9.6% of median household income (2022) |

| Out-of-Pocket Costs (2022) | $1,250 single/$2,500 family (average deductible for employer plans) |

| Total Healthcare Spending per Capita (2022) | $12,914 (includes insurance premiums, out-of-pocket costs, and taxes) |

| Percentage of Americans with Employer Coverage (2022) | 54% of population |

| Percentage of Americans with Individual Market Coverage (2022) | 7% of population |

| Medicare Spending per Enrollee (2022) | $16,088 annually |

| Medicaid Spending per Enrollee (2022) | $8,969 annually |

| Uninsured Rate (2022) | 8.3% of population |

Explore related products

What You'll Learn

- Average Annual Premiums: Cost of health insurance plans for individuals and families nationwide

- Employer-Sponsored Coverage: Amount employers and employees contribute to health insurance annually

- Out-of-Pocket Expenses: Deductibles, copays, and coinsurance costs beyond premiums

- Medicare/Medicaid Spending: Government expenditures on public health insurance programs yearly

- State-by-State Variations: Differences in health insurance costs across U.S. states

![]()

Average Annual Premiums: Cost of health insurance plans for individuals and families nationwide

Americans spend a significant portion of their income on health insurance, with average annual premiums varying widely based on plan type, location, and coverage level. For individuals, the average annual premium for employer-sponsored health insurance in 2023 was approximately $8,435, with employees contributing about $1,327 of that total. Families face even higher costs, averaging $23,968 annually, with employees paying around $6,575. These figures highlight the substantial financial commitment required to maintain health coverage, even with employer subsidies.

When considering individual market plans purchased through healthcare exchanges, costs differ significantly. In 2023, the average annual premium for a benchmark silver plan (the second-lowest-cost silver plan, used to calculate subsidies) was roughly $510 per month, or $6,120 annually, before subsidies. However, 80% of enrollees received premium tax credits, reducing their average monthly cost to $150, or $1,800 annually. This disparity underscores the importance of understanding eligibility for financial assistance when budgeting for health insurance.

For families purchasing plans on the individual market, the financial burden is even more pronounced. A family of four might face average annual premiums exceeding $16,000 for a silver plan before subsidies. With tax credits, this could drop to around $4,000 annually, depending on income. These figures illustrate the critical role of subsidies in making health insurance affordable for many households, particularly those with moderate incomes.

To navigate these costs effectively, individuals and families should assess their healthcare needs and budget constraints. High-deductible health plans (HDHPs) paired with health savings accounts (HSAs) can offer lower premiums but require careful management of out-of-pocket expenses. Conversely, plans with higher premiums and lower deductibles may be more suitable for those anticipating frequent medical care. Additionally, comparing plans during open enrollment and leveraging available subsidies can significantly reduce annual costs.

Geography also plays a pivotal role in determining premiums. For instance, states like Alaska and Wyoming often have higher average premiums due to limited insurer competition and higher healthcare costs, while states like Minnesota and Rhode Island tend to have lower averages. Understanding regional trends can help individuals and families set realistic expectations and explore cost-saving strategies, such as choosing plans with narrower provider networks or utilizing telemedicine services to offset expenses.

Do Illegal Aliens Receive Free Health Insurance? Unraveling the Facts

You may want to see also

Explore related products

![]()

Employer-Sponsored Coverage: Amount employers and employees contribute to health insurance annually

Employer-sponsored health insurance is a cornerstone of the American healthcare system, covering approximately 155 million workers and their dependents. In 2023, the average annual premium for employer-sponsored family coverage reached $22,463, with employers contributing $16,269 (72%) and employees paying $6,194 (28%). This breakdown highlights a significant financial commitment from both parties, though the employee share has been steadily rising over the past decade, outpacing wage growth and inflation. For single coverage, the average premium was $7,911, with employers contributing $6,575 (83%) and employees $1,336 (17%). These figures underscore the shared burden of healthcare costs in the workplace.

Consider the implications for employees, particularly those in lower-wage jobs. While employer contributions offset a substantial portion of premiums, the employee share can still represent a sizable expense. For instance, a worker earning $30,000 annually and contributing $6,194 for family coverage is allocating over 20% of their income to health insurance premiums alone. This financial strain is exacerbated by rising deductibles and out-of-pocket costs, which averaged $2,000 for single coverage and $4,000 for family plans in 2023. Employers, meanwhile, face the challenge of balancing competitive benefits packages with controlling costs, often opting for high-deductible health plans (HDHPs) paired with health savings accounts (HSAs) to shift more financial responsibility to employees.

From a strategic perspective, employers must weigh the long-term benefits of offering robust health insurance against immediate cost concerns. Studies show that comprehensive coverage improves employee retention, productivity, and overall health outcomes, potentially reducing absenteeism and presenteeism. However, small businesses, which employ nearly half of the U.S. workforce, often struggle to provide competitive benefits due to higher per-employee premium costs. For example, firms with fewer than 50 employees paid an average of $600 more per employee for health insurance than larger firms in 2022. This disparity highlights the need for policy interventions, such as tax credits or pooled insurance options, to level the playing field for smaller employers.

A comparative analysis reveals that the U.S. system contrasts sharply with those in countries like Canada or the UK, where government-funded healthcare eliminates the need for employer-sponsored insurance. In the U.S., however, this model remains dominant, with 54% of non-elderly Americans relying on workplace coverage. As healthcare costs continue to rise, employers and employees must navigate this complex landscape together. Practical tips for employees include evaluating plan options during open enrollment, maximizing employer-offered wellness programs, and contributing to HSAs for tax advantages. Employers, on the other hand, can explore value-based care models, telemedicine, and preventive care initiatives to curb costs while maintaining comprehensive coverage.

Ultimately, the employer-sponsored insurance system reflects a delicate balance between shared responsibility and financial sustainability. While it remains a vital mechanism for accessing healthcare, its future hinges on addressing affordability challenges for both employers and employees. Policymakers, businesses, and workers must collaborate to ensure this system evolves in a way that prioritizes accessibility, equity, and long-term viability. Without such efforts, the growing burden of healthcare costs risks undermining the very benefits employer-sponsored coverage is intended to provide.

Selecting Medical Insurance in the USA: A Step-by-Step Guide

You may want to see also

Explore related products

$18.95 $8.99

![Life and Health Insurance Study Cards: Life Health Insurance License Exam Prep with Practice Test Questions [Full Color]](https://m.media-amazon.com/images/I/51Pox87Z5lL._AC_UY218_.jpg)

![]()

Out-of-Pocket Expenses: Deductibles, copays, and coinsurance costs beyond premiums

Americans spend an average of $7,000 to $12,000 per year on health insurance premiums, but this is just the tip of the financial iceberg. Beyond these recurring costs lie out-of-pocket expenses—deductibles, copays, and coinsurance—that can significantly inflate the total annual healthcare expenditure. For instance, a family with a high-deductible plan might pay $5,000 out of pocket before insurance coverage kicks in, while copays for specialist visits or prescriptions can add hundreds more. Understanding these costs is crucial for budgeting and avoiding unexpected financial strain.

Consider deductibles, the amount you pay before insurance coverage begins. For a 40-year-old individual with a Bronze plan, a $6,000 deductible means every doctor’s visit, lab test, or medication is paid entirely out of pocket until that threshold is met. This can be particularly burdensome for chronic conditions requiring frequent care. Coinsurance, typically 20% of costs after the deductible, adds another layer of expense. For example, a $10,000 surgery would require $2,000 out of pocket, even after the deductible is paid. Copays, while smaller, accumulate quickly—a $40 specialist visit copay twice a month totals $960 annually.

To mitigate these costs, analyze your healthcare usage patterns. If you rarely visit the doctor, a high-deductible plan with a Health Savings Account (HSA) might save money, as HSA contributions are tax-deductible. However, if you manage a condition like diabetes or asthma, a plan with lower out-of-pocket maximums—capped at $8,000 for individuals or $16,000 for families in 2023—may be more cost-effective. Always compare the total annual cost, including premiums and estimated out-of-pocket expenses, rather than focusing solely on monthly premiums.

A practical tip: keep a healthcare expense journal. Track every copay, prescription cost, and procedure to identify trends and anticipate future expenses. For families, consider plans with embedded deductibles, which allow individual family members to meet their deductible independently, preventing the entire family deductible from applying to each person’s care. Additionally, negotiate medical bills—hospitals and providers often offer discounts for upfront payments or payment plans.

In conclusion, out-of-pocket expenses are a hidden yet substantial component of healthcare costs. By understanding deductibles, copays, and coinsurance, and strategically choosing a plan based on your health needs, you can minimize financial surprises. Proactive management, from tracking expenses to negotiating bills, ensures that health insurance works as a safety net, not a financial burden.

Missouri Seasonal Home Insurance: Top Providers for Vacation Homes

You may want to see also

Explore related products

![]()

Medicare/Medicaid Spending: Government expenditures on public health insurance programs yearly

In 2022, the U.S. government spent over $1.3 trillion on Medicare and Medicaid, accounting for approximately 25% of the federal budget. This staggering figure underscores the critical role these programs play in providing healthcare coverage to millions of Americans, particularly the elderly, disabled, and low-income populations. Medicare, which primarily serves individuals aged 65 and older, along with certain younger people with disabilities, consumed about $828 billion, while Medicaid, a joint federal-state program for low-income individuals, cost roughly $512 billion. These numbers highlight not only the scale of government commitment but also the growing financial pressures as the population ages and healthcare costs rise.

Analyzing the breakdown, Medicare spending is largely driven by hospitalization (Part A) and physician services (Part B), with prescription drug coverage (Part D) also contributing significantly. Medicaid, on the other hand, varies by state due to its joint funding structure, with expenditures influenced by state policies, eligibility criteria, and the health needs of the enrolled population. For instance, states with expanded Medicaid under the Affordable Care Act tend to have higher enrollment and spending but also better health outcomes for low-income residents. This variability emphasizes the need for tailored approaches to manage costs while ensuring access to care.

From a comparative perspective, Medicare and Medicaid spending dwarfs private health insurance expenditures, which averaged about $7,000 per person annually in 2022. While private insurance is often employer-sponsored and varies widely in coverage and cost, public programs provide a safety net that is both comprehensive and consistent, albeit at a high price. The challenge lies in balancing fiscal sustainability with the moral imperative to provide healthcare to vulnerable populations. Policymakers must navigate this tension, considering reforms such as value-based care models, fraud prevention, and cost-sharing adjustments to curb escalating expenses.

For individuals and families, understanding Medicare and Medicaid spending is crucial for advocating for better policies and making informed decisions. For example, seniors approaching Medicare eligibility should explore supplemental plans (Medigap) or Medicare Advantage to address gaps in coverage. Low-income families should stay informed about Medicaid expansions in their state, as eligibility criteria can change. Practical tips include leveraging preventive services covered by Medicare, such as annual wellness visits and screenings, to manage health proactively and reduce long-term costs. Similarly, Medicaid beneficiaries can take advantage of managed care plans that offer coordinated services and additional benefits like dental or vision care.

In conclusion, Medicare and Medicaid spending reflects a substantial investment in public health, but it also demands scrutiny and innovation to ensure efficiency and equity. As these programs continue to evolve, stakeholders—from policymakers to beneficiaries—must engage in informed dialogue to address challenges and sustain these vital lifelines for millions of Americans.

Understanding Medical Insurance Deductibles: What's the Meaning?

You may want to see also

Explore related products

![]()

State-by-State Variations: Differences in health insurance costs across U.S. states

Health insurance costs in the U.S. are far from uniform, with significant state-by-state variations that can leave families in one region paying nearly double what their counterparts in another state spend. For instance, in 2023, the average annual premium for a single individual in Massachusetts was approximately $7,500, while in Minnesota, it hovered around $4,200. These disparities are driven by a complex interplay of factors, including state regulations, provider networks, and the overall health of the population. Understanding these differences is crucial for anyone looking to optimize their healthcare spending or relocate to a more cost-effective area.

Analyzing the Drivers of Cost Disparities

One of the primary factors behind state-by-state variations is the regulatory environment. States like New York and California have mandated extensive coverage requirements, including mental health parity and maternity care, which drive up premiums. In contrast, states like Wyoming and Idaho have fewer mandates, allowing insurers to offer cheaper, albeit less comprehensive, plans. Additionally, the concentration of healthcare providers plays a role. States with a high density of specialists and hospitals, such as Massachusetts, often see higher costs due to increased utilization and negotiation power by providers. Conversely, rural states with fewer providers, like Mississippi, may have lower premiums but limited access to care.

Practical Tips for Navigating State Differences

If you’re considering a move or shopping for insurance, start by researching your state’s benchmark plan—the second-lowest-cost silver plan on the marketplace, which determines subsidy eligibility. For example, in 2023, Alaska’s benchmark plan cost $8,200 annually, while Alabama’s was $5,800. Use tools like Healthcare.gov to compare premiums and subsidies across states. If you’re self-employed or work remotely, consider relocating to a state with lower costs, but factor in the availability of specialists and the overall quality of care. For instance, while Texas has lower premiums, its high uninsured rate can strain local healthcare systems.

Comparative Insights: High-Cost vs. Low-Cost States

High-cost states like Massachusetts and Colorado often justify their premiums with better health outcomes and broader coverage. For example, Massachusetts’ near-universal coverage has led to lower rates of preventable hospitalizations. On the other hand, low-cost states like Utah and Idaho may offer affordable premiums but often have higher out-of-pocket costs or limited provider networks. A family in Utah might pay $12,000 annually for a bronze plan with a $7,000 deductible, while a similar plan in Colorado could cost $15,000 but include a $3,000 deductible. Weigh these trade-offs carefully, especially if you have chronic conditions or anticipate frequent medical needs.

The Role of State-Specific Policies

State policies can either exacerbate or mitigate cost disparities. For instance, states that expanded Medicaid under the Affordable Care Act, like Kentucky and Nevada, have seen lower average premiums due to a healthier risk pool. Conversely, states that did not expand Medicaid, such as Florida and Texas, often have higher premiums as insurers account for the cost of uncompensated care. Some states, like Vermont, are experimenting with public options or reinsurance programs to stabilize costs. If you live in or are moving to a state with such initiatives, take advantage of these programs to reduce your overall healthcare spending.

Navigating state-by-state health insurance costs requires a combination of research, flexibility, and strategic planning. Whether you’re leveraging subsidies in high-cost states or exploring low-premium options in others, understanding the unique drivers of costs in your area can save you thousands annually. Use state-specific data, compare plans meticulously, and consider the long-term implications of coverage trade-offs. In the patchwork of U.S. healthcare, being informed is your best defense against unexpected expenses.

Does Health Insurance Cover Dental Care? What You Need to Know

You may want to see also

Frequently asked questions

The average American spends approximately $7,500 to $8,500 per year on health insurance, including premiums, deductibles, and out-of-pocket costs, though this varies based on factors like employer contributions and plan type.

Americans typically spend about 8% to 10% of their annual income on health insurance, though this can be higher for lower-income individuals and lower for those with employer-sponsored plans.

Employees with employer-sponsored health insurance contribute an average of $1,200 to $2,000 annually for individual coverage and $5,000 to $6,000 for family coverage, with employers covering the majority of the premium.

Individuals without employer coverage pay an average of $400 to $700 per month ($4,800 to $8,400 annually) for health insurance, depending on factors like age, location, and plan tier.