A High Deductible Health Plan (HDHP) is a health insurance plan that offers lower monthly premiums but higher out-of-pocket costs before the insurance company starts to pay its share. This type of plan can be combined with a Health Savings Account (HSA), allowing individuals to save money on a pre-tax basis to cover qualified medical expenses. The funds in an HSA can be used for certain out-of-pocket health care costs, such as dental, drug, and vision expenses, providing greater flexibility in managing healthcare expenses. However, it is important to note that HDHPs may not be suitable for everyone, especially those who anticipate frequent doctor visits or unplanned urgent care.

| Characteristics | Values |

|---|---|

| Type of Plan | Health insurance plan with a high deductible |

| Monthly Premium | Lower than traditional insurance plans |

| Health Care Costs | Pay more before insurance company pays its share |

| Combination with HSA | Can be combined with a Health Savings Account (HSA) |

| HSA Contributions | Tax-deductible or pre-tax |

| HSA Usage | Used to pay for certain out-of-pocket health care costs |

| HSA Perks | Tax-free savings, employer contributions, portability |

| Eligibility | Determined by the health plan based on provided information |

| Disadvantages | Expensive out-of-pocket costs if actual care exceeds plans |

Explore related products

What You'll Learn

![]()

HDHPs and HSAs: How they work together

A High Deductible Health Plan (HDHP) is a health insurance plan with a higher deductible than a traditional insurance plan. The monthly premium is usually lower, but you pay more healthcare costs yourself before the insurance company pays its share.

A Health Savings Account (HSA) is a tax-advantaged savings account that lets you set aside money on a pre-tax basis to pay for qualified out-of-pocket medical expenses that your HDHP doesn't cover. This includes expenses for yourself, your spouse, and your tax dependents. You can use an HSA to pay for certain expenses with untaxed money, and any funds left in your HSA roll over from year to year.

You must be enrolled in an HDHP to participate in an HSA, but you are not required to have an HSA if you are enrolled in an HDHP. However, the two work well together. HDHPs have higher deductibles, so you need to budget for your out-of-pocket healthcare costs. An HSA can be used to pay for these costs with untaxed money, helping you manage your healthcare expenses.

If you enrol in an HDHP and an HSA, you can benefit from lower monthly premiums and tax-free savings that can be used to pay for eligible medical expenses. HSAs are also flexible, remaining with you regardless of your employment status or place of work. This means you can use an HSA to save for future healthcare expenses, even if you switch jobs.

Medical Insurance Acceptance: Can Your Practice Advertise This?

You may want to see also

Explore related products

![]()

Pros and cons of HDHPs

A High Deductible Health Plan (HDHP) is a type of health insurance plan that has a higher deductible than a traditional insurance plan. HDHPs usually have lower monthly premiums but higher out-of-pocket costs, which means that individuals may face financial strain if they need medical services before meeting the deductible.

Pros of HDHPs

- Lower monthly premiums: HDHPs typically offer lower monthly premiums compared to traditional health plans, which can result in significant cost savings.

- Tax benefits: HDHPs can be paired with Health Savings Accounts (HSAs) or Health Reimbursement Arrangements (HRAs), which offer tax advantages. You can contribute pre-tax dollars to an HSA, and these funds can roll over year to year, providing a long-term savings option for healthcare costs.

- Discounted rates: Healthcare providers who are in-network for an HDHP may offer discounted rates to those with coverage. These discounts can range from 20% to 50% and can make necessary healthcare services more affordable once the deductible is met.

Cons of HDHPs

- Higher out-of-pocket costs: HDHPs have higher deductibles, which means you will pay more for out-of-pocket medical expenses before your insurance coverage kicks in. This can be a financial burden, especially if you require frequent healthcare services, have unplanned medical emergencies, or have chronic conditions that need ongoing treatment.

- Reluctance to seek medical care: Due to the high out-of-pocket costs, individuals may delay or avoid seeking medical treatment to avoid expensive bills. This reluctance may lead to a lack of preventative care and potentially worsen health conditions.

- Not ideal for families: HDHPs are generally not a good fit for families with young children, as children are more likely to get sick and need frequent visits to the pediatrician.

- Limited coverage: HDHPs typically only cover preventive care, so accidents, emergencies, or unexpected health issues may result in very high out-of-pocket costs.

It is important to carefully consider your expected medical expenses, health status, and financial situation before choosing an HDHP. While HDHPs can offer cost savings for relatively healthy individuals, they may not be suitable for those with frequent or unpredictable healthcare needs.

Switching Insurance: Medicaid to Private, What You Need to Know

You may want to see also

Explore related products

![]()

Lower monthly premiums

A High-Deductible Health Plan (HDHP) is a health insurance plan with a higher deductible than a traditional insurance plan. The monthly premium is usually lower, but the policyholder must pay more healthcare costs themselves before the insurance company starts to pay its share. This is known as the deductible.

HDHPs are often combined with a Health Savings Account (HSA). An HSA is a tax-free savings account that lets you set aside money to pay for qualified medical expenses. The money deposited into an HSA is tax-free, which can help you save money. HSAs can be used to pay for certain out-of-pocket healthcare costs and get you closer to reaching your deductible. They also come with other perks, like employer contributions and the freedom to take your HSA with you if you switch jobs.

It is important to carefully weigh the pros and cons of high-deductible health insurance to find the coverage that's right for you. HDHPs may not be a good fit if you anticipate unplanned urgent care visits or frequent doctor's appointments. Additionally, not all preventive care services may be covered, such as immunizations for travel.

Oscar Health Insurance: Is It Medicaid?

You may want to see also

Explore related products

![]()

Out-of-pocket costs

Deductibles refer to the amount you spend on covered health services and prescription drugs before your insurance plan starts to pay. For example, you may have to pay the first $2,000 of covered services yourself.

Copayments are fixed amounts you pay for a covered health service after meeting your deductible. For example, you may pay $20 for a doctor visit.

Coinsurance is the percentage of covered health service costs you pay after meeting your deductible. For example, if your plan covers 80% of a $125 service, you pay 20% or $25.

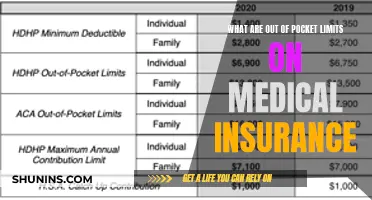

The Affordable Care Act (ACA) has introduced an annual limit on out-of-pocket costs. For 2024, the maximum out-of-pocket costs for an individual are $9,450, and for a family, they are $18,900. These caps change each year and will decrease in 2025 to $9,200 and $18,400, respectively.

Health plans can set out-of-pocket spending caps below the maximum allowable limits, so these limits vary across plans. Additionally, eligible enrollees who select silver-level plans may benefit from the ACA's cost-sharing subsidies, resulting in lower out-of-pocket limits.

High Deductible Health Plans (HDHPs) are a type of insurance plan with higher deductibles than traditional plans. They usually have lower monthly premiums but can lead to higher out-of-pocket costs, especially if you require more care than anticipated. Combining an HDHP with a Health Savings Account (HSA) can help manage these costs by allowing you to pay for certain out-of-pocket expenses with tax-free savings.

Insurance Card Scanners: Medical Office Cost-Saving Solutions

You may want to see also

Explore related products

![]()

Tax advantages of HSAs

A High Deductible Health Plan (HDHP) is a health insurance plan with a higher deductible than a traditional insurance plan. The monthly premium is usually lower, but you pay more healthcare costs yourself before the insurance company pays its share.

A Health Savings Account (HSA) is a savings account that lets you set aside money on a pre-tax basis to pay for qualified medical expenses. It is a type of account that is recognised by the IRS and is one of the most tax-advantaged accounts available.

- Funds spent from an HSA are not taxed as long as they are spent on qualified medical expenses. Qualified medical expenses include doctor visits, dental and vision care, and prescription drugs. If HSA funds are spent on non-qualified medical expenses, taxes and a 20% penalty apply. However, once the accountholder turns 65, HSA funds can be used for any reason without penalty, although the money will be taxed.

- Contributions to an HSA are not taxed. This is in contrast to other retirement accounts, which are taxed either when funds go into the account or when funds are withdrawn.

- Interest and investment earnings on HSA funds are not taxed. Accountholders can grow their HSA funds over time through interest and investing, and these increases in funds are not subject to taxes.

- HSAs have no expiration date and no required minimum distribution. This means accountholders can spend years growing their HSA funds tax-free.

- The HSA stays with the accountholder even if they change employers, and the money in the HSA remains shielded from tax.

- Employer contributions to an HSA are excluded from the employee's income and are not subject to employment taxes.

Getting Medical Insurance for Your Child: A Step-by-Step Guide

You may want to see also

Frequently asked questions

HD stands for High Deductible Health Plan. This type of insurance plan offers lower monthly premiums but higher out-of-pocket costs before the insurance company starts to pay its share.

A High Deductible Health Plan (HDHP) has a higher deductible and lower monthly premiums than a traditional insurance plan. The deductible is the amount you pay for covered health care services before your insurance plan starts to pay.

An HSA is a Health Savings Account. It is a type of savings account that lets you set aside money on a pre-tax basis to pay for qualified medical expenses. An HDHP can be combined with an HSA to help pay for certain out-of-pocket health care costs.

High Deductible Health Plans are not for everyone. They are more suitable for people who rarely visit the doctor or need urgent care. If you frequently visit the doctor or take medication, an HDHP may not be the best option as the out-of-pocket costs can be high.