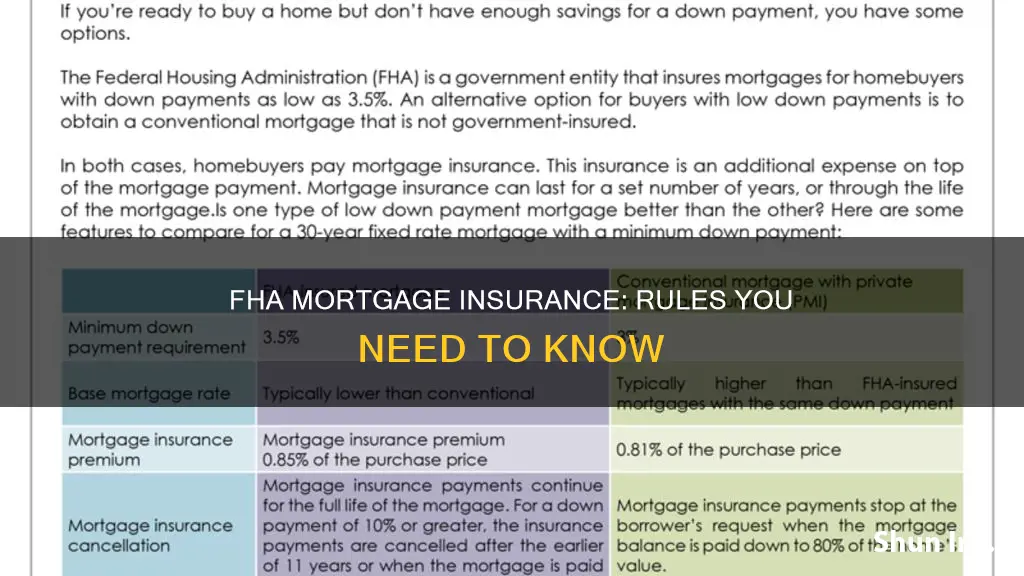

FHA loans are a great option for first-time homebuyers as they require a low down payment of just 3.5%. However, FHA loans come with the added expense of mortgage insurance premiums (MIP) which are paid to protect lenders against losses that result from defaults on home mortgages. The FHA MIP includes an upfront cost, paid as part of the closing costs, and a monthly cost included in the monthly payment. The upfront MIP payment is 1.75% of the total loan value and is due when the loan is closed, or it can be added to the loan balance. The annual MIP is calculated as a percentage of the base loan value and is paid monthly. The length of the loan term also affects the amount paid towards FHA MIP. While FHA MIP is beneficial to homebuyers as it allows them to qualify for a mortgage with a smaller down payment, it increases the overall cost of the loan.

| Characteristics | Values |

|---|---|

| FHA requirements | Include mortgage insurance (MIP) for FHA loans to protect lenders against losses that result from defaults on home mortgages |

| Mortgage insurance premiums | Required when down payments are less than 20% of the appraised value |

| FHA MIP | An additional payment to secure the mortgage loan |

| FHA loan MIP | Involves two payments: an upfront premium and an additional annual payment |

| Upfront MIP payment | Equal to 1.75% of the total value of the loan |

| Annual mortgage insurance premium costs | Vary depending on the base loan amount |

| FHA MIP reduction | The U.S. Department of Housing and Urban Development (HUD) reduced the annual FHA MIP by 30 basis points (BPS) as of February 2023 |

| FHA MIP removal | Options include automatic termination and refinancing |

| FHA MIP refund | Eligible if the loan is refinanced or the home is sold within the first 3 years of the loan term |

| FHA MIP removal eligibility | Depends on when the FHA loan was taken out and the original down payment amount |

| FHA loans without MIP | Available for eligible service members or those buying in qualifying rural areas |

Explore related products

What You'll Learn

![]()

FHA mortgage insurance premium (MIP)

FHA MIP is beneficial to homebuyers as it reduces the risk to the lender of making a loan to the borrower. This means that the borrower may qualify for a loan that they might not otherwise be able to get. However, it increases the cost of the loan. If a borrower defaults on their FHA loan, the Federal Housing Administration (FHA) will compensate the lender for the outstanding balance. The MIP payments go to the Mutual Mortgage Insurance Fund (MMIF), which the FHA uses to pay out claims to lenders.

The annual MIP payment is calculated as a percentage of the base loan value. The length of the loan term also affects the amount paid toward FHA MIP. For example, as of February 2023, for FHA loan terms greater than 15 years, borrowers pay 0.50% annually toward FHA MIP. The annual MIP payment is usually added to the monthly mortgage payment by lenders.

There are two main ways to remove FHA MIP: automatic termination and refinancing. Automatic termination of MIP depends on when the FHA loan was taken out and the original down payment amount. For loans taken out before June 3, 2013, with a down payment of at least 10%, MIP can be removed after 5 years. For loans taken out after this date with the same down payment conditions, MIP can be removed after 11 years. If the down payment was less than 10%, the borrower must pay MIP for the life of the loan, unless they refinance.

Reporting a House Break-In: When to Involve Insurance

You may want to see also

Explore related products

$13.25

![FHA Multi-Family Housing Mortgage Insurance Program... Hearing... S. Hrg. 107-534... Committee On Banking, Housing, & Urban Affairs, United States Senate... 107th Congress, 1st Session [Leather Bound]](https://m.media-amazon.com/images/I/61IX47b4r9L._AC_UY218_.jpg)

![]()

MIP protects lenders against defaults

Mortgage Insurance Premium (MIP) is an insurance policy that is mandatory for all Federal Housing Administration (FHA) loans. MIP is an additional payment made by the borrower to secure the mortgage loan. It is an insurance policy that protects the lender in the event of borrower default.

FHA loans are considered riskier for lenders because they often cater to borrowers with lower credit scores and smaller down payments. MIP, therefore, acts as a safeguard for lenders, compensating them in the event of borrower default. This insurance allows lenders to expand access to loans for borrowers who may not otherwise qualify.

MIP includes two types of payments: upfront MIP (UFMIP) and annual MIP. The upfront premium is typically paid at closing and amounts to 1.75% of the total loan amount. The annual payment is based on the total loan amount, the loan term, and the down payment, ranging from 0.15% to 0.75% of the outstanding loan amount.

The FHA sets the rates for MIP, and the payments go directly to the FHA to fund and operate the mortgage insurance program. Should a borrower default on an FHA loan, the FHA compensates the lender for the outstanding balance. This protection allows lenders to mitigate the risk associated with providing mortgages to higher-risk borrowers.

It is important to note that MIP does not protect the borrower; it is solely for the lender's protection. Borrowers with FHA loans may be required to pay MIP for the entire loan term, depending on the loan's origination date and the down payment amount.

Tort Insurance: Is Full Coverage Worth the Cost?

You may want to see also

Explore related products

![]()

MIP upfront and annual payments

Mortgage Insurance Premium (MIP) is an additional payment made by homeowners to secure an FHA loan. It is a type of mortgage insurance that protects lenders against losses that may result from defaults on home mortgages. The upfront MIP payment is typically due when the loan is issued or closed, and it is usually equal to 1.75% of the total loan value. Borrowers have the option to pay this upfront cost in cash or add it to their loan balance. This upfront MIP payment is a one-time fee unless the borrower takes out another FHA loan or refinances their existing loan.

The annual MIP payment, on the other hand, is an ongoing expense that is typically included in the monthly mortgage payments. The annual MIP rate varies between 0.15% to 0.75% of the loan amount and is determined by factors such as the loan amount, loan term, and loan-to-value (LTV) ratio. For instance, if you have a $200,000 FHA loan, your annual MIP payment would range from $300 to $1,500, depending on the specific rate applied. It's important to note that the U.S. Department of Housing and Urban Development (HUD) reduced the annual FHA MIP by 30 basis points in February 2023, resulting in lower MIP payments for borrowers.

The length of the loan term also affects the duration of MIP payments. For FHA loans with terms greater than 15 years, borrowers can expect to pay MIP for the entire loan term if their down payment is less than 10%. If the down payment is 10% or higher, the MIP payments will last for the first 11 years of the loan. Additionally, it's worth mentioning that FHA loans with down payments of 3.5% or lower may require MIP payments for the entire loan term, regardless of the loan amount.

While MIP increases the overall cost of an FHA loan, it is beneficial to borrowers as it enables them to qualify for a mortgage with a lower down payment. Without MIP, lenders would typically require a larger down payment to mitigate the risk of default. Therefore, MIP makes homeownership more accessible to individuals who may not have substantial savings for a large down payment.

Strategies to Sidestep CMHC Mortgage Insurance

You may want to see also

Explore related products

![]()

Removing FHA mortgage insurance

FHA mortgage insurance, also known as MIP (Mortgage Insurance Premium), is an additional payment made to secure an FHA loan. This insurance protects the lender in the event that the borrower defaults on the loan. While it increases the cost of the loan, it also makes it more likely that the borrower will qualify for the loan in the first place.

FHA mortgage insurance isn't permanent and can be removed in a few different ways. One way is to refinance into a conventional loan once you've built up 20% equity in your home. This option allows you to switch to a loan without PMI (private mortgage insurance). However, refinancing comes with its own costs, and current interest rates may be higher than when you originally took out your loan.

Another option for removing FHA mortgage insurance is to refinance into a VA loan if you have eligible current or former U.S. military service history. VA loans do not have ongoing mortgage insurance requirements, and you don't need to have equity in the home to qualify.

If you don't want to refinance, there are a few other options for removing FHA mortgage insurance. If your loan is from before June 3, 2013, or you put down 10% or more and your loan started after that date, your MIP will automatically drop off after 11 years. Additionally, if you refinance or sell your home within the first 3 years of your FHA loan, you may be eligible for a partial refund of your upfront MIP.

It's important to note that removing FHA mortgage insurance may not always be the best financial decision, as refinancing can come with its own costs and higher interest rates. It's essential to carefully consider your options and seek professional advice before making any decisions.

Mortgage Insurance: Money-Wasting or Necessary Evil?

You may want to see also

Explore related products

![]()

MIP costs and how they vary

Mortgage insurance premiums (MIP) are required for all FHA loans to protect lenders against losses that result from defaults on home mortgages. The MIP cost varies depending on the type of loan and the loan amount.

FHA MIP rates are set by the Federal Housing Administration and depend on the loan amount, down payment, and loan term. The upfront MIP payment is typically 1.75% of the total value of the loan, due when you close on your FHA loan or added to the balance of the loan. The upfront payment is only due once unless you refinance or take on another FHA loan in the future. The annual MIP ranges from 0.15% to 0.75% of the loan amount, depending on the base loan amount, loan-to-value (LTV) ratio, and duration of the mortgage term.

The length of time you are paying off your FHA loan also affects the amount you pay toward MIP. For example, for FHA loans with a term of more than 15 years, the annual MIP is 0.50% for loans less than or equal to $726,200. With a 10% or larger down payment on an FHA loan, you will pay MIP for the first 11 years, while a down payment of less than 10% will result in MIP lasting the entire loan term.

It is important to note that FHA MIP rates are standardized and generally cannot be canceled, even as you build equity. The only way to eliminate the MIP on an FHA loan is to refinance it into a non-FHA product or pay off the loan.

Reporting Insurance Proceeds: Rental Property Guide

You may want to see also

Frequently asked questions

An FHA mortgage insurance premium (MIP) is an additional fee that all FHA loan borrowers pay to secure the mortgage loan. It is paid upfront and over the mortgage term.

The upfront MIP payment is equal to 1.75% of the total value of your loan. For example, if you borrow $150,000 for your mortgage, you will make an upfront payment of $3,500. The upfront payment is due when you close on your FHA loan, or it can be added to the balance of the loan. Annual MIP costs vary depending on the base loan amount.

MIP protects the lender if you default on your loan. It also helps borrowers qualify for a loan that they might not otherwise be able to get.

Yes, there are two main ways to remove FHA mortgage insurance: automatic termination and refinancing. The eligibility criteria for automatic MIP cancellation depend on when you took out your FHA loan and your original down payment amount.