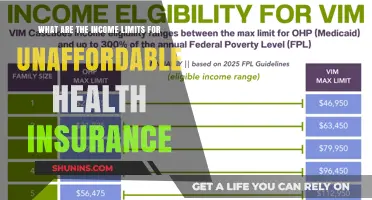

The Affordable Health Care Act (AHCA) was a significant piece of legislation in the United States aimed at reforming the healthcare system. One of the key aspects of the AHCA was its approach to pre-existing conditions. Prior to the AHCA, individuals with pre-existing health conditions often faced challenges in obtaining affordable health insurance, as insurers could deny coverage or charge higher premiums based on their health status. The AHCA sought to address this issue by implementing protections for those with pre-existing conditions, ensuring that they could access health insurance without being discriminated against due to their health history.

Explore related products

What You'll Learn

- Pre-existing Conditions Coverage: Explains how the AHCA addresses coverage for individuals with pre-existing health conditions

- High-Risk Pools: Discusses the creation of high-risk pools to manage costs associated with insuring those with pre-existing conditions

- Essential Health Benefits: Outlines whether the AHCA mandates coverage for essential health benefits, which can include pre-existing conditions

- Waiting Periods: Details any waiting periods imposed by the AHCA before coverage for pre-existing conditions becomes effective

- State Waivers: Describes how states can apply for waivers under the AHCA to modify pre-existing conditions coverage requirements

![]()

Pre-existing Conditions Coverage: Explains how the AHCA addresses coverage for individuals with pre-existing health conditions

The American Health Care Act (AHCA) has specific provisions regarding coverage for individuals with pre-existing health conditions. Unlike some previous health care policies, the AHCA does not guarantee that individuals with pre-existing conditions will be able to obtain health insurance at the same rates as those without such conditions. Instead, it allows states to opt out of certain protections for people with pre-existing conditions, potentially leading to higher premiums or denial of coverage for this group.

Under the AHCA, insurers are permitted to charge higher premiums to individuals with pre-existing conditions, as long as the state in which they operate has opted out of the pre-existing condition protections. This could result in significant financial burdens for those with chronic illnesses or other health issues that existed prior to the enactment of the AHCA. Additionally, the AHCA establishes a high-risk pool to provide coverage for individuals who are unable to obtain insurance through traditional means due to their pre-existing conditions. However, the funding and effectiveness of these high-risk pools have been a subject of debate and uncertainty.

One of the key criticisms of the AHCA's approach to pre-existing conditions is that it undermines the principle of guaranteed issue, which ensures that all individuals, regardless of their health status, can obtain health insurance. By allowing states to opt out of these protections, the AHCA creates a fragmented health care system where the availability and affordability of coverage for individuals with pre-existing conditions vary significantly from state to state. This can lead to disparities in access to care and outcomes for those with chronic health conditions.

Furthermore, the AHCA's provisions regarding pre-existing conditions have raised concerns about the potential for discrimination against individuals with certain health issues. By permitting insurers to charge higher premiums or deny coverage based on pre-existing conditions, the AHCA may inadvertently encourage discrimination against those with chronic illnesses or disabilities. This is particularly concerning given that many individuals with pre-existing conditions are already facing challenges in accessing affordable and comprehensive health care.

In conclusion, the AHCA's approach to pre-existing conditions represents a significant shift from previous health care policies, potentially leading to increased financial burdens and reduced access to care for individuals with chronic health conditions. The effectiveness of the AHCA's provisions, particularly the high-risk pools, remains uncertain, and the potential for discrimination against those with pre-existing conditions is a pressing concern. As such, it is crucial for policymakers and stakeholders to carefully consider the implications of these provisions and work towards ensuring that all individuals, regardless of their health status, have access to affordable and comprehensive health care.

Understanding the Complex Structure of Health Insurance in the USA

You may want to see also

Explore related products

$106.72 $245.95

![]()

High-Risk Pools: Discusses the creation of high-risk pools to manage costs associated with insuring those with pre-existing conditions

High-risk pools are a mechanism designed to manage the costs associated with insuring individuals who have pre-existing medical conditions. These pools are typically created by state governments or private insurance companies and are intended to provide a safety net for those who might otherwise be denied coverage or face exorbitant premiums due to their health status. By pooling the risks of many individuals with pre-existing conditions, these programs aim to spread the financial burden more evenly, making health insurance more accessible and affordable for this vulnerable population.

The concept of high-risk pools is rooted in the idea of risk sharing, where the collective risk of a group is shared among all members. This approach helps to mitigate the financial impact of insuring individuals with costly medical conditions by distributing the costs across a larger pool of insured individuals. As a result, high-risk pools can help to stabilize insurance premiums and ensure that those with pre-existing conditions are not priced out of the market.

One of the key challenges associated with high-risk pools is determining eligibility. Typically, individuals must have a pre-existing condition that would otherwise make them uninsurable or result in significantly higher premiums. The specific conditions covered can vary depending on the program, but common examples include chronic illnesses such as diabetes, heart disease, and cancer, as well as conditions that require ongoing medical treatment or have a high likelihood of recurrence.

Another important consideration is the funding of high-risk pools. These programs often require substantial financial resources to operate effectively, and funding can come from a variety of sources, including government appropriations, insurance company contributions, and premiums paid by insured individuals. The sustainability of these pools depends on a careful balance between the number of individuals covered, the severity of their conditions, and the available funding.

In practice, high-risk pools can take different forms, ranging from state-run programs to private insurance offerings. State-run pools are often more comprehensive and may offer a wider range of benefits, while private pools may be more limited in scope but can provide more flexibility in terms of coverage options and provider networks. Regardless of the specific model, the goal remains the same: to provide affordable and accessible health insurance to those who need it most.

Overall, high-risk pools represent an important tool in the effort to ensure that all individuals, regardless of their health status, have access to quality health care. By managing the costs associated with insuring those with pre-existing conditions, these programs help to promote a more equitable and sustainable health insurance system.

Do Twitch Streamers Have Health Insurance? Exploring Coverage Options

You may want to see also

Explore related products

![]()

Essential Health Benefits: Outlines whether the AHCA mandates coverage for essential health benefits, which can include pre-existing conditions

The Affordable Health Care Act (AHCA) has been a subject of much debate, particularly regarding its provisions on essential health benefits and pre-existing conditions. Essential health benefits are a set of health care services and items that the AHCA requires insurance plans to cover. These benefits are designed to ensure that individuals have access to necessary medical care, including preventive services, emergency care, and treatment for chronic conditions.

One of the key aspects of the AHCA's approach to essential health benefits is its impact on individuals with pre-existing conditions. Prior to the AHCA, many insurance plans could deny coverage or charge higher premiums to individuals with pre-existing health conditions. The AHCA aimed to address this issue by mandating that insurance plans cover essential health benefits for all individuals, regardless of their health status. This means that individuals with pre-existing conditions cannot be denied coverage or charged higher premiums based on their health history.

However, the AHCA's provisions on essential health benefits and pre-existing conditions have faced significant challenges and changes. In 2017, the Tax Cuts and Jobs Act repealed the individual mandate, which required individuals to have health insurance or face a penalty. This change has led to concerns that the AHCA's protections for individuals with pre-existing conditions may be weakened, as insurance plans may no longer be required to cover essential health benefits if individuals are not mandated to have insurance.

Additionally, the AHCA has faced legal challenges, including a lawsuit filed by several states arguing that the law's provisions on pre-existing conditions are unconstitutional. In 2019, a federal judge ruled that the AHCA's protections for individuals with pre-existing conditions are unconstitutional, leading to further uncertainty about the future of these provisions.

Despite these challenges, the AHCA remains in effect, and its provisions on essential health benefits and pre-existing conditions continue to shape the health insurance landscape. Individuals with pre-existing conditions should be aware of their rights under the AHCA and should consult with a health insurance professional to understand how these provisions may impact their coverage options.

Company Insurance vs. Alternatives: Which Option Saves You More?

You may want to see also

Explore related products

![]()

Waiting Periods: Details any waiting periods imposed by the AHCA before coverage for pre-existing conditions becomes effective

Under the Affordable Health Care Act (AHCA), waiting periods for pre-existing conditions vary significantly depending on the specific circumstances of the individual and the state in which they reside. Generally, the AHCA imposes a waiting period of up to 12 months before coverage for pre-existing conditions becomes effective for individuals who have a gap in their health insurance coverage. This waiting period is designed to prevent individuals from purchasing health insurance only when they need it, which could lead to higher premiums for everyone.

However, there are several exceptions to this waiting period. For example, individuals who have been continuously covered by health insurance for at least 12 months prior to applying for a new plan are not subject to the waiting period. Additionally, individuals who have been diagnosed with a pre-existing condition while they are covered by health insurance are also not subject to the waiting period.

It is important to note that the AHCA allows states to waive the waiting period for pre-existing conditions. As of now, several states have taken advantage of this waiver, including California, Colorado, and Maryland. In these states, individuals with pre-existing conditions can obtain health insurance coverage without having to wait for the standard 12-month period.

To determine if you are subject to a waiting period for pre-existing conditions under the AHCA, it is important to review your individual circumstances and consult with a health insurance professional. They can help you understand your options and determine if you are eligible for coverage without a waiting period.

Does Buckeye Health Insurance Cover Your Needs? A Comprehensive Guide

You may want to see also

![]()

State Waivers: Describes how states can apply for waivers under the AHCA to modify pre-existing conditions coverage requirements

Under the Affordable Health Care Act (AHCA), states have the option to apply for waivers that allow them to modify the coverage requirements for pre-existing conditions. This provision is designed to provide states with greater flexibility in managing their healthcare systems and addressing the unique needs of their populations. To apply for a waiver, states must submit a detailed proposal to the Department of Health and Human Services (HHS), outlining the specific changes they wish to make and the expected impact on healthcare access and affordability.

The waiver process is governed by a set of guidelines established by HHS, which require states to demonstrate that their proposed changes will not significantly increase healthcare costs for individuals with pre-existing conditions or reduce access to essential health benefits. States must also show that their waiver will promote competition in the health insurance market and improve the overall quality of care.

One of the key considerations for states applying for waivers is the potential impact on individuals with pre-existing conditions. While the AHCA prohibits insurers from denying coverage or charging higher premiums based on pre-existing conditions, states with waivers may be able to implement alternative approaches that could affect the affordability and accessibility of care for these individuals. For example, a state might propose a high-risk pool to cover individuals with pre-existing conditions, or it might seek to modify the essential health benefits required under the AHCA.

The waiver process is complex and requires careful consideration of a range of factors, including the potential impact on healthcare access, affordability, and quality. States must also navigate the political and regulatory landscape, as waivers are subject to review and approval by HHS and may face opposition from consumer advocacy groups and other stakeholders. Despite these challenges, the waiver process provides states with an opportunity to innovate and develop tailored solutions to meet the healthcare needs of their populations.

In conclusion, state waivers under the AHCA offer a mechanism for states to modify pre-existing conditions coverage requirements, but they must carefully consider the potential impact on healthcare access and affordability. The waiver process is governed by HHS guidelines and requires states to demonstrate that their proposed changes will promote competition and improve the quality of care. By navigating this complex process, states can develop innovative solutions to address the unique healthcare needs of their populations.

Navigating Medical Insurance: Accessing Coverage for Your Health

You may want to see also

Frequently asked questions

The AHCA covers a wide range of pre-existing conditions including, but not limited to, chronic illnesses such as diabetes, heart disease, and asthma, as well as mental health conditions and substance abuse disorders. It also protects individuals with pre-existing conditions from being charged higher premiums or being denied coverage.

The AHCA prohibits insurance companies from denying coverage or charging higher premiums to individuals based on their pre-existing conditions. It also requires insurers to provide essential health benefits, which include coverage for pre-existing conditions, ensuring that all individuals have access to necessary healthcare services.

The AHCA introduced significant changes to the healthcare system by mandating that insurance companies cannot discriminate against individuals with pre-existing conditions. Prior to the AHCA, many people with pre-existing conditions were either denied coverage or faced exorbitant premiums. The AHCA aimed to make healthcare more accessible and affordable for all, regardless of their health status.