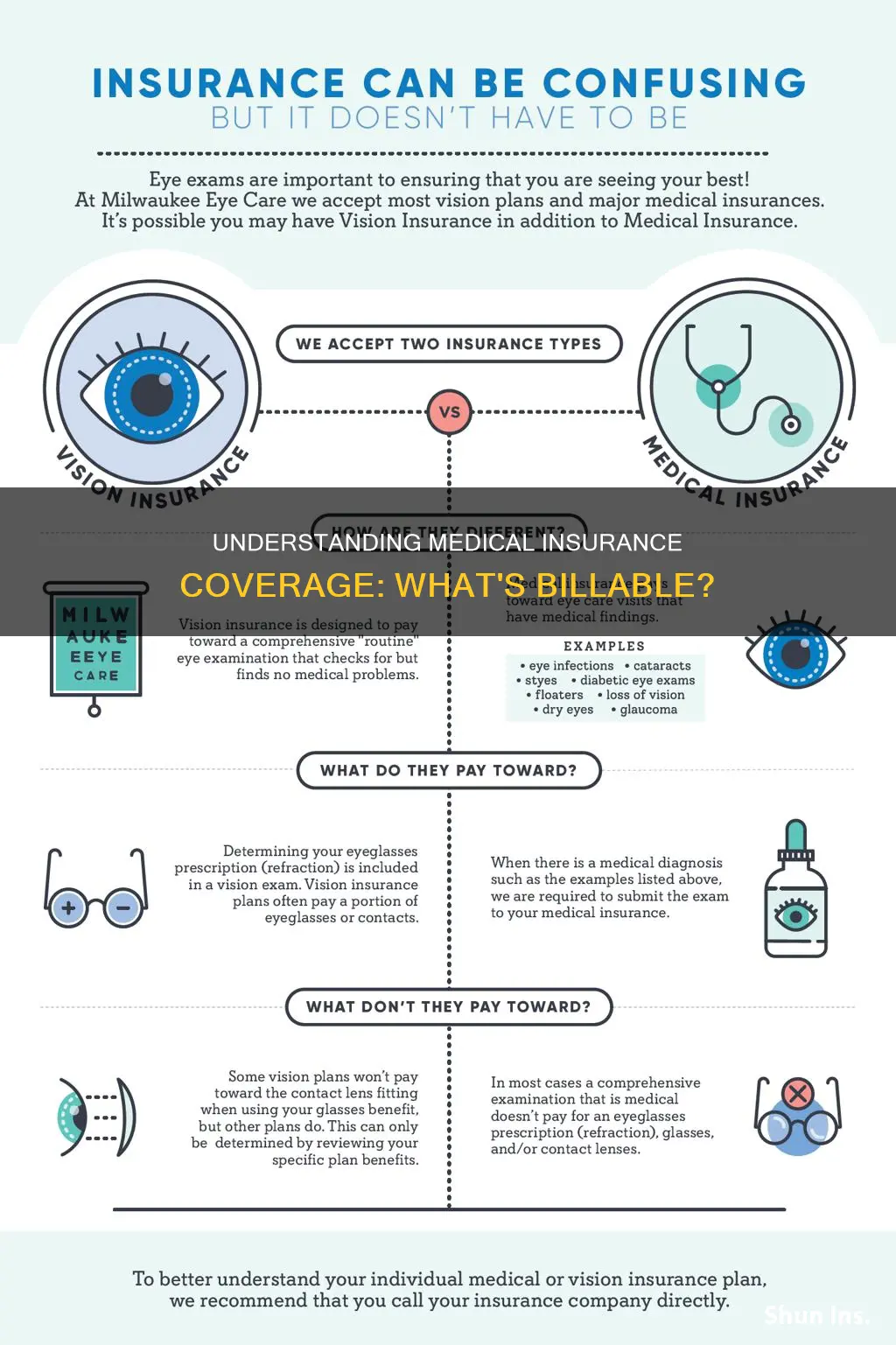

Understanding what can be billed to medical insurance is an important aspect of healthcare. The billing process involves submitting a claim to the insurance company, listing the services provided by healthcare professionals. This claim is then used by the insurance company to reimburse the healthcare provider, with the patient potentially covering the remaining balance. It is essential to differentiate between in-network and out-of-network providers, as this affects billing and patient costs. Federal laws protect individuals from unexpected out-of-network charges for emergency services, and certain plans offer continued in-network rates for a period after a provider leaves the network. Additionally, specific services like diagnostic care, virtual care, and follow-up treatments may be billed separately from preventive care, and patients may be responsible for a portion of the cost. Understanding billing statements, Explanation of Benefits (EOB), and insurance terms is crucial for patients to effectively navigate their financial responsibilities and rights within the healthcare system.

| Characteristics | Values |

|---|---|

| Medical Imaging | X-ray, MRI, Ultrasound |

| Care for Newborn Babies | Neonatology |

| Diagnostic Services | Radiology, Laboratory Services |

| Emergency Services | Emergency Room Services, Post-Stabilization Services |

| Virtual Care | MyUCLAHealth Messages, Telemedicine |

| Preventative Check-ups | Preventative Care, Follow-up or Diagnostic Care |

| Third-Party Payer | Insurance Companies, Government Agencies, Employers |

| Type of Service | CPT Treatment Codes |

| Usual, Customary and Reasonable (UCR) Charges | Base Amount Insurance Company Will Pay |

| Cost-Sharing | Co-payment, Deductible, Coinsurance |

| Electronic Data Interchange (EDI) | Link Between Billing System and Insurance Company |

| Electronic Funds Transfer (EFT) | Direct Deposit of Insurance Claims Payments |

Explore related products

![]()

Virtual care

Insurance Coverage for Virtual Care

Many insurance plans cover virtual care services, including major insurance carriers and government-funded programs. For example, MinuteClinic Virtual Care accepts some insurance plans, including certain Medicaid and Medicare options. MultiCare also accepts insurance for virtual visits, billing them the same as in-person visits. NYU Langone Virtual Urgent Care is also covered by most major insurance carriers.

Self-Pay Options

If you don't have insurance, some providers offer self-pay options for virtual visits. For instance, MultiCare charges a flat fee of $250 for a video visit if you don't have insurance, while MinuteClinic Virtual Care accepts credit, debit, flexible spending accounts (FSA), and health savings account (HSA) cards.

Insurance Verification

Before scheduling a virtual care visit, it is essential to verify that your insurance plan covers telehealth services. Some providers, such as NYU Langone, require you to call their customer service to verify your insurance plan details. This step ensures that you won't be charged the self-pay fee, which can be as high as $126 for some providers.

Technology Requirements

To access virtual care services, you typically need a device with a camera and a microphone, such as a smartphone, along with a stable internet connection. Some providers may have specific requirements, so it's important to review their instructions before your appointment.

Availability

In conclusion, virtual care offers a convenient and accessible option for receiving medical care, and many providers accept insurance billing for these services. However, it is important to verify your insurance coverage and understand the billing process to avoid unexpected charges.

Understanding Medical Insurance Deductibles: Managing Your Out-of-Pocket Expenses

You may want to see also

Explore related products

![]()

Emergency services

If you have health insurance and require emergency services, you are generally protected from out-of-network charges for emergency medical services. This means that you cannot be charged more for emergency medical services than the in-network rate. However, it is important to note that some health plans do not cover emergency care, so it is advisable to check with your insurance company or health plan to understand your specific coverage.

When you visit an emergency room, federal law protects you from out-of-network bills for emergency services in hospitals, hospital outpatient departments, and independent freestanding emergency departments. This means that you cannot be asked to sign a notice and consent form for these emergency services, and providers are not allowed to ask you to give up these protections. However, this protection does not extend to post-stabilization services, where you may be asked to sign a consent form for out-of-network care if you are able to travel to a nearby in-network provider without needing emergency transportation.

It is important to understand the distinction between emergency services and post-stabilization services. Emergency services refer to the immediate medical attention and treatment provided to stabilize a patient's condition. On the other hand, post-stabilization services refer to the additional care and treatment required after the patient's condition has stabilized to maintain their health. These services may include follow-up treatments, diagnostic tests, or specialized care.

In terms of billing, emergency rooms typically charge a facility fee for the use of their facilities and related ancillary services. This fee is separate from the charges for physician services, which are billed separately. It is essential to review your billing statements carefully and understand the breakdown of charges to ensure that your insurance coverage is applied correctly.

Additionally, virtual care, such as myUCLAhealth messages, may also be billed to your insurance in certain cases. If a message requires a doctor's time and medical expertise to evaluate a new problem or symptom, or for follow-up treatment after a recent operation, it may be considered billable virtual care. However, not all virtual care messages incur a cost, and some may be covered under your insurance plan.

Entering Medical Insurance in Open Dental: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Vaccines

In the United States, Medicare Part D prescription plans cover most vaccines, while Part B covers vaccines like COVID-19, influenza, and pneumococcal vaccines. Medicare Advantage plans are required to offer benefits that are equal to or greater than original Medicare, and many include Part D prescription coverage. However, it's important to note that some vaccines may not be covered under Part D, and plans without Part D coverage may require alternative arrangements.

Private health insurance plans, including ACA marketplace plans, usually cover certain vaccines without charging coinsurance or copayments. This is also true for Medicaid, which offers free or reduced-cost healthcare to eligible individuals, including children. Additionally, the Vaccines for Children (VFC) program ensures that children under 19 who are uninsured or underinsured have access to necessary vaccines.

It's worth noting that travel vaccinations are typically not covered by basic insurance policies, and even supplementary health insurance plans may not always include them. Therefore, it's essential to carefully review the policy conditions of your insurance plan to understand what vaccinations are covered and to what extent.

Furthermore, some vaccines may have slight copayments, while others are covered entirely by insurance. This can vary depending on factors such as age, health condition, and the recommended vaccination schedule for different age groups. For example, children and adolescents follow a different vaccination schedule than adults, and older adults may qualify for additional covered vaccines based on their age and risk of serious illness.

Overall, health insurance plays a crucial role in ensuring access to vaccines, and it's important for individuals to understand their insurance coverage to take full advantage of the benefits offered.

Herpes Medication Costs Without Insurance: What You Need to Know

You may want to see also

Explore related products

![]()

Post-stabilization care

In the context of insurance, post-stabilization care services are covered by the patient's health insurance plan. The insurance company is responsible for paying for these services, which can include treatments, therapies, procedures, medications, or equipment usage. The patient may still be responsible for cost-sharing, such as copayments, deductibles, or coinsurance, depending on their specific insurance plan.

It is important to note that post-stabilization care services are typically provided in-network to avoid unexpected out-of-network charges. Federal law protects patients from out-of-network bills for emergency services, but this protection does not always extend to post-stabilization services. Patients should carefully review any consent forms and understand their insurance coverage to avoid unexpected charges.

In some cases, patients may receive post-stabilization care from out-of-network providers if certain conditions are met. For example, if the patient can safely travel to a nearby in-network provider without needing emergency transportation, they may be responsible for out-of-network charges. It is the responsibility of the healthcare provider to inform the patient of their options and any potential financial implications.

Overall, post-stabilization care is an important aspect of a patient's recovery process, and understanding insurance coverage for these services can help patients make informed decisions about their care and avoid unexpected financial burdens.

Colorado Medical Insurance: Monthly Costs and Coverage

You may want to see also

Explore related products

![]()

Laboratory services

Understanding Laboratory Services:

Insurance Coverage for Laboratory Services:

Most health insurance plans cover at least some laboratory services as part of diagnostic services. However, the extent of coverage can vary significantly between plans. It is essential to carefully review your insurance policy or contact your insurance provider to understand what specific laboratory services are covered and under what circumstances.

Billing Process for Laboratory Services:

When it comes to billing, laboratory services typically follow a standard process:

- Before receiving laboratory services, ensure your insurance information is up to date and confirm that your insurance company accepts claims from the laboratory performing the tests.

- After the tests are conducted, the laboratory will typically send a claim directly to your insurance company.

- Your insurance company will process the claim and determine the amount they will cover based on your plan's benefits.

- You will receive an Explanation of Benefits (EOB) from your insurance company, outlining the services provided, the amount covered, and any remaining balance for which you are responsible.

- If there is a remaining balance, the laboratory will send you a bill for that amount, which may include your copayment, deductible, or other costs as outlined in your insurance coverage terms.

It is important to note that if you do not have insurance or if your insurance does not cover clinical laboratory testing services, you will be responsible for the full cost of the tests. Some laboratories offer discounted rates or payment options for self-paying patients.

Additionally, in certain cases, you may receive protection from surprise billing or balance billing, as outlined in the No Surprises Act. This act ensures that when receiving services from an in-network facility, you cannot be charged more than your plan's in-network cost-sharing amount, even if specific providers within that facility are out-of-network. However, this may vary depending on the state, as some states have their own laws regarding surprise billing for laboratory services.

In conclusion, laboratory services are often billable to medical insurance, but it is essential to understand your specific coverage details. Staying informed about your insurance benefits and staying proactive in reviewing bills and EOBs can help you effectively manage your healthcare finances.

Whole Life Insurance and Medicaid: Can You Have Both?

You may want to see also

Frequently asked questions

If your health insurance covers emergency care, you are protected from out-of-network charges for emergency services in hospitals, hospital outpatient departments, and independent, freestanding emergency departments.

If you believe your provider isn't following the No Surprises Act, you can submit a complaint by calling the No Surprises Help Desk at 1-800-985-3059.

An EOB is a statement sent by the insurance company after processing a claim received from the provider. It shows what the insurance company is paying for, what it’s not paying for, and why.

In-network coverage refers to services provided by healthcare providers who have agreed to a contract with your insurance company. Out-of-network charges refer to services provided by healthcare providers who do not have a contract with your insurance company and are typically more expensive.

Some common examples of services that may not be covered by medical insurance include retinal imaging during eye exams, immunizations, and facility fees for the use of clinics and related ancillary services during preventive check-ups.