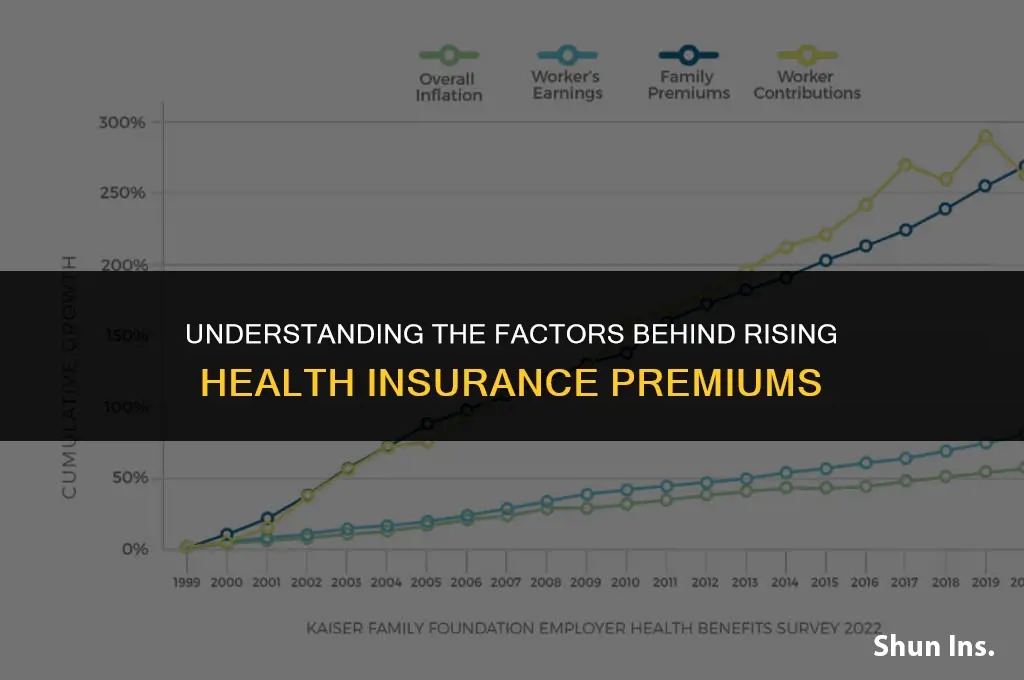

Health insurance rates can increase due to a variety of factors, including rising healthcare costs, changes in government regulations, and shifts in the overall health of the population. Insurers may also adjust rates based on the number of claims filed, the severity of those claims, and the demographic profiles of their policyholders. Additionally, market competition and the introduction of new, more expensive medical treatments and technologies can contribute to higher premiums. Understanding these factors can help individuals and policymakers alike navigate the complexities of the healthcare system and make informed decisions about coverage and cost management.

| Characteristics | Values |

|---|---|

| Increased healthcare costs | Higher prices for medical services and treatments |

| Aging population | Older individuals tend to have more health issues |

| Chronic diseases | Conditions like diabetes and heart disease require ongoing care |

| Prescription drug prices | High costs of medications contribute to rising premiums |

| Medical technology advancements | New technologies and treatments can be expensive |

| Administrative costs | Insurance companies' operational expenses impact rates |

| Government regulations | Changes in healthcare laws and policies affect pricing |

| Market competition | Lack of competition among insurers can lead to higher rates |

| Fraud and abuse | Illegal activities increase costs for insurers |

| Natural disasters and pandemics | Events like hurricanes and COVID-19 can cause significant healthcare expenses |

Explore related products

What You'll Learn

- Rising Healthcare Costs: Increased expenses for medical services, treatments, and prescription drugs drive up insurance rates

- Aging Population: As the population ages, older individuals require more healthcare, leading to higher insurance premiums

- Chronic Diseases: The prevalence of chronic conditions like diabetes and heart disease increases healthcare costs, affecting insurance rates

- Regulatory Changes: Government policies and regulations, such as the Affordable Care Act, can impact insurance rates

- Market Competition: The level of competition among insurance providers can influence premium rates in different regions

![]()

Rising Healthcare Costs: Increased expenses for medical services, treatments, and prescription drugs drive up insurance rates

The escalating cost of healthcare is a significant driver behind the rising rates of health insurance. This phenomenon is multifaceted, influenced by various factors including the increasing expenses of medical services, treatments, and prescription drugs. One of the primary reasons for this upward trend is the advancement in medical technology. While these innovations have undoubtedly improved patient outcomes, they come at a steep price. For instance, the cost of developing and manufacturing new drugs is substantial, often running into billions of dollars. These expenses are inevitably passed on to consumers in the form of higher drug prices, which in turn contribute to the overall increase in healthcare costs.

Another factor contributing to the rise in healthcare costs is the growing demand for specialized care. As the population ages and chronic diseases become more prevalent, there is an increased need for specialized medical services. These services, which include everything from physical therapy to home healthcare, are often more expensive than general medical care. Furthermore, the shortage of healthcare professionals in certain fields can drive up the cost of these specialized services, as providers can command higher fees due to the limited supply.

The administrative costs associated with healthcare also play a significant role in driving up expenses. The complexity of the healthcare system, with its myriad of regulations and requirements, necessitates a substantial amount of administrative work. This includes everything from billing and coding to compliance and risk management. These administrative tasks require a significant amount of time and resources, which contribute to the overall cost of healthcare.

In addition to these factors, the increasing prevalence of lifestyle-related diseases is also contributing to the rise in healthcare costs. Conditions such as obesity, diabetes, and heart disease, which are often linked to lifestyle choices, are becoming more common. The treatment of these conditions can be expensive, particularly when they require ongoing care and management. Furthermore, the cost of preventative measures, such as screenings and vaccinations, can also contribute to the overall increase in healthcare costs.

The impact of these rising healthcare costs is felt most acutely by individuals and families who are struggling to afford their health insurance premiums. As the cost of healthcare continues to increase, it is likely that health insurance rates will continue to rise as well. This underscores the importance of addressing the underlying factors contributing to these costs, in order to make healthcare more affordable and accessible for all.

Will Your Insurance Company Contact Your Bank? What You Need to Know

You may want to see also

Explore related products

![]()

Aging Population: As the population ages, older individuals require more healthcare, leading to higher insurance premiums

The aging population is a significant contributor to the rising cost of health insurance premiums. As people live longer, they tend to require more medical care, which increases the overall demand for healthcare services. This heightened demand, coupled with the limited supply of healthcare providers, drives up costs. Insurance companies must then pass these increased costs on to policyholders in the form of higher premiums.

Older individuals are more likely to have chronic conditions such as diabetes, heart disease, and arthritis, which require ongoing medical attention and treatment. Additionally, the likelihood of needing long-term care increases with age, further adding to healthcare expenses. The cost of treating these conditions can be substantial, and as the population ages, the number of people requiring such care grows, putting additional strain on the healthcare system.

Advances in medical technology and treatments have also contributed to the rising cost of healthcare for older individuals. While these advancements can improve quality of life and extend lifespan, they often come with a high price tag. Insurance companies must factor in the cost of these treatments when setting premiums, which can lead to higher rates for all policyholders.

Another factor to consider is the impact of the aging population on the workforce. As more people retire, there is a decrease in the number of working individuals contributing to the economy. This can lead to a reduction in tax revenue, which may affect government-funded healthcare programs such as Medicare and Medicaid. As a result, private insurance companies may need to absorb some of these costs, leading to increased premiums for their policyholders.

In conclusion, the aging population is a complex issue that has far-reaching implications for the healthcare system and insurance premiums. As the demand for healthcare services increases and the supply of providers remains limited, costs will continue to rise. Insurance companies must adapt to these changes by adjusting their premiums, which can have a significant impact on policyholders. It is essential for individuals to understand these factors when considering their health insurance options and planning for their future healthcare needs.

Does United Health Insurance Cover Breast Pumps? A Comprehensive Guide

You may want to see also

Explore related products

$24.99

![]()

Chronic Diseases: The prevalence of chronic conditions like diabetes and heart disease increases healthcare costs, affecting insurance rates

The rising prevalence of chronic diseases such as diabetes and heart disease is a significant contributor to the increasing costs of healthcare, which in turn impacts health insurance rates. Chronic conditions require ongoing medical attention and management, leading to higher healthcare expenditures over time. For instance, diabetes management involves regular blood sugar monitoring, insulin or medication, and frequent doctor visits, all of which add up to substantial costs. Similarly, heart disease may necessitate expensive procedures like angioplasty or bypass surgery, along with long-term medication and monitoring.

These increased costs are passed on to insurance companies, which must then adjust their premiums to cover the higher expenses. Additionally, the prevalence of chronic diseases often leads to a greater demand for specialized healthcare services and facilities, further driving up costs. For example, the need for advanced imaging technologies, specialized clinics, and skilled healthcare professionals to manage these conditions can significantly increase the overall healthcare budget.

Moreover, chronic diseases often result in complications that require additional medical interventions, exacerbating the financial burden. For instance, diabetes can lead to complications such as kidney disease, neuropathy, and retinopathy, each requiring its own set of treatments and care. This not only increases the direct costs of healthcare but also leads to indirect costs such as lost productivity and increased disability claims.

To mitigate these rising costs, there is a growing emphasis on preventive care and lifestyle interventions aimed at reducing the incidence and severity of chronic diseases. By promoting healthy behaviors such as regular exercise, balanced diets, and smoking cessation, healthcare providers and insurers hope to lower the overall burden of chronic diseases and, consequently, the costs associated with their management. Additionally, advancements in medical technology and research are continually improving the efficiency and effectiveness of treatments, offering hope for more cost-effective solutions in the future.

In conclusion, the prevalence of chronic diseases like diabetes and heart disease plays a crucial role in driving up healthcare costs, which are then reflected in higher health insurance rates. Addressing this issue requires a multifaceted approach that includes preventive care, lifestyle interventions, and ongoing advancements in medical technology and research. By working together, healthcare providers, insurers, and individuals can help to manage the financial impact of chronic diseases and improve overall health outcomes.

Adding Family Health Insurance: A Step-by-Step Guide for You

You may want to see also

Explore related products

$41.99 $33.29

$23.74 $24.99

![]()

Regulatory Changes: Government policies and regulations, such as the Affordable Care Act, can impact insurance rates

Government policies and regulations, such as the Affordable Care Act (ACA), have a profound impact on health insurance rates. The ACA, for instance, introduced several provisions aimed at expanding coverage and improving healthcare quality, but these changes also led to increased costs for insurers. One significant factor was the requirement for insurers to cover pre-existing conditions, which increased the risk pool and, consequently, the premiums. Additionally, the ACA mandated essential health benefits, such as maternity care and mental health services, which further drove up costs.

Another regulatory change that affects insurance rates is the implementation of the Medical Loss Ratio (MLR) rule. This rule requires insurers to spend a certain percentage of premium dollars on healthcare services and quality improvement, rather than on administrative costs or profits. While this rule aims to ensure that consumers receive better value for their premiums, it can also lead to higher rates if insurers struggle to meet the MLR requirements.

Furthermore, state-level regulations can also influence health insurance rates. For example, some states have imposed rate review laws, which require insurers to justify rate increases and can lead to lower premiums. However, other states have more lenient regulations, allowing insurers to raise rates more freely. This variation in state regulations can result in significant differences in insurance rates across the country.

In conclusion, regulatory changes can have a substantial impact on health insurance rates. While some policies, like the ACA, aim to improve coverage and healthcare quality, they can also lead to increased costs for insurers, which are then passed on to consumers in the form of higher premiums. Understanding the complex interplay between government policies and insurance rates is crucial for consumers and policymakers alike.

Au Pairs' Medical Insurance: What's Covered and What's Not

You may want to see also

Explore related products

![]()

Market Competition: The level of competition among insurance providers can influence premium rates in different regions

The dynamics of market competition play a pivotal role in shaping health insurance premium rates across various regions. In areas where multiple insurance providers vie for market share, consumers often benefit from lower premiums as companies strive to offer competitive pricing. Conversely, regions with fewer providers may experience higher rates due to the reduced competitive pressure. This phenomenon is rooted in the principles of supply and demand, where a higher supply of insurance options tends to drive down costs, making coverage more affordable for the average consumer.

Analyzing the impact of market competition on health insurance rates involves examining several key factors. Firstly, the number of active providers in a given region is a primary indicator of competitive intensity. A higher number of insurers typically leads to more aggressive pricing strategies, as each company seeks to attract and retain customers. Secondly, the market share distribution among providers can reveal the level of dominance held by any single insurer. If one company holds a significant majority of the market share, it may have less incentive to lower premiums, potentially leading to higher rates for consumers.

Furthermore, the strategic responses of insurance providers to competitive pressures can also influence premium rates. For instance, some companies may focus on differentiating their products through enhanced coverage options or superior customer service, which can justify higher premiums. Others may engage in price wars, undercutting competitors to gain market share, which can drive down overall rates in the short term. Additionally, the regulatory environment in which insurers operate can impact their ability to compete effectively. States with more stringent insurance regulations may limit the flexibility of providers to adjust their pricing strategies, potentially dampening competition and leading to higher premiums.

In conclusion, understanding the interplay between market competition and health insurance rates is crucial for consumers, policymakers, and industry stakeholders alike. By recognizing the factors that contribute to competitive dynamics in the insurance market, individuals can make more informed decisions about their coverage options, while regulators can craft policies that promote a more competitive and affordable insurance landscape.

Understanding Self-Insured Health Plans: Benefits, Risks, and How They Work

You may want to see also

Frequently asked questions

Health insurance rates can rise due to several key factors, including increased healthcare costs, changes in government regulations, higher rates of chronic diseases, and the aging population.

As the cost of medical services, medications, and hospital stays increases, insurance companies must pay more out-of-pocket. To cover these higher expenses, they often raise premiums.

Government policies, such as the Affordable Care Act (ACA), can influence health insurance rates. Regulations that require insurers to cover more services or accept more patients can lead to increased costs, which are then passed on to consumers.

Older individuals generally require more medical care and have higher healthcare costs. As the population ages, the demand for healthcare services increases, driving up the overall cost of health insurance.

Yes, lifestyle choices such as smoking, poor diet, and lack of exercise can lead to higher rates of chronic diseases. Insurers may charge higher premiums to individuals with these risk factors to offset the potential costs of future healthcare needs.