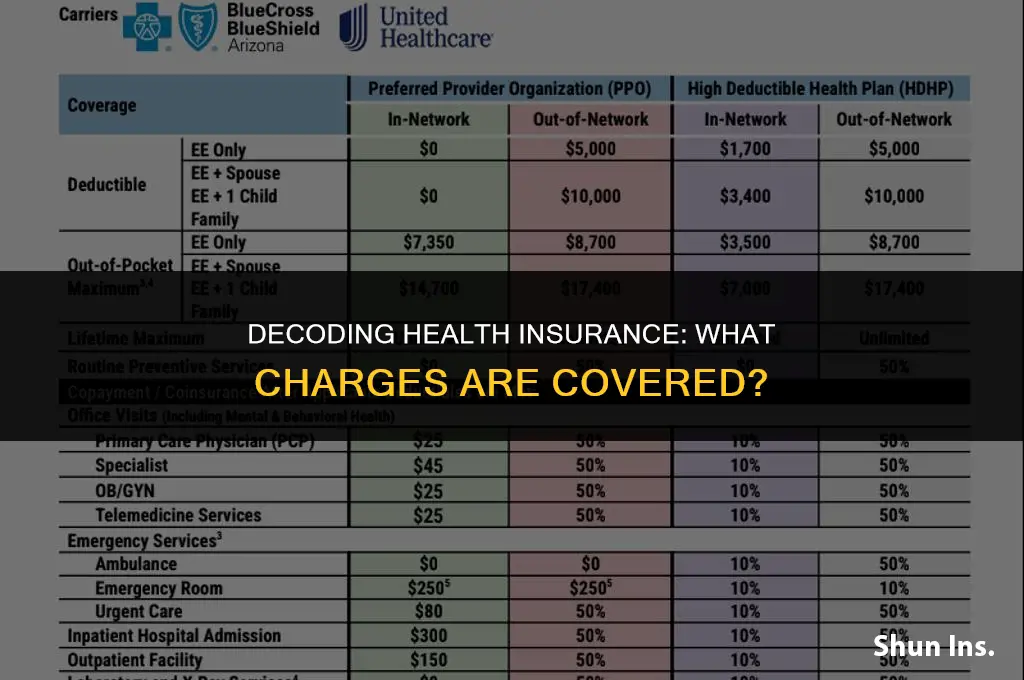

Health insurance is a critical aspect of modern healthcare, providing financial protection against the high costs of medical services. When it comes to understanding what charges health insurance covers, it's essential to delve into the specifics of different policies and providers. Generally, health insurance plans cover a wide range of medical expenses, including doctor visits, hospital stays, prescription medications, and diagnostic tests. However, the extent of coverage can vary significantly depending on the type of plan, such as HMO, PPO, or EPO, and the insurance company offering it. Some plans may also include additional benefits like dental and vision care, mental health services, and wellness programs. It's crucial for individuals to carefully review their policy documents and consult with their insurance providers to fully understand the scope of their coverage and any potential out-of-pocket expenses they may incur.

| Characteristics | Values |

|---|---|

| Coverage Type | In-network, Out-of-network |

| Services Covered | Doctor visits, Hospital stays, Prescription drugs, Preventive care, Mental health services, Dental care, Vision care |

| Limits and Deductibles | Annual limits, Lifetime limits, Deductibles, Co-pays, Co-insurance |

| Premiums | Monthly premiums, Annual premiums |

| Eligibility | Age, Income, Employment status, Pre-existing conditions |

| Enrollment Periods | Open enrollment, Special enrollment |

| Appeals Process | Denial appeals, Grievance appeals |

| Provider Network | In-network providers, Out-of-network providers |

| Cost Sharing | Coinsurance, Copayments |

| Essential Health Benefits | Ambulatory care, Emergency care, Hospitalization, Maternity care, Mental health care, Prescription drugs, Preventive care, Pediatric care |

Explore related products

What You'll Learn

- Inpatient Services: Covers hospital stays, including room and board, nursing care, and medical treatments

- Outpatient Services: Includes doctor visits, specialist consultations, diagnostic tests, and minor procedures not requiring hospitalization

- Prescription Medications: Coverage for prescribed drugs, with varying levels of copayments or coinsurance depending on the plan

- Preventive Care: Routine check-ups, vaccinations, screenings, and counseling to prevent or detect health issues early

- Mental Health Services: Therapy sessions, counseling, and treatment for mental health conditions, including substance abuse disorders

![]()

Inpatient Services: Covers hospital stays, including room and board, nursing care, and medical treatments

Inpatient services are a critical component of health insurance coverage, encompassing a range of essential medical care provided during hospital stays. This includes room and board, which covers the cost of accommodation and meals; nursing care, which involves the services of registered nurses and other healthcare professionals; and medical treatments, which may include medications, therapies, and diagnostic procedures. Understanding what is covered under inpatient services can help individuals make informed decisions about their healthcare and insurance needs.

One unique aspect of inpatient services is the varying levels of care that may be required depending on the patient's condition. For instance, some patients may need intensive care, which involves close monitoring and specialized medical attention, while others may require general medical-surgical care. The costs associated with these different levels of care can vary significantly, and insurance coverage may differ accordingly. It is important for individuals to review their insurance policies to understand the specific coverage provided for different types of inpatient care.

Another important consideration is the duration of hospital stays. While some medical conditions may require only a short hospitalization, others may necessitate extended stays. Insurance coverage for inpatient services typically includes a certain number of days, after which additional costs may be incurred. Patients should be aware of these limitations and plan accordingly, potentially exploring options for extended coverage or supplemental insurance if necessary.

In addition to the direct medical costs, inpatient services may also cover ancillary expenses such as laboratory tests, imaging studies, and rehabilitation services. These additional costs can add up quickly, making comprehensive insurance coverage essential for protecting against financial hardship. Furthermore, some insurance plans may offer additional benefits, such as coverage for mental health services or substance abuse treatment, which can be crucial for individuals facing complex health challenges.

When evaluating health insurance options, it is crucial to consider the specific inpatient services covered and the associated costs. This includes understanding deductibles, copayments, and coinsurance, as well as any pre-authorization requirements or restrictions on coverage. By carefully reviewing and comparing insurance plans, individuals can select the option that best meets their healthcare needs and financial circumstances, ensuring they have access to the necessary inpatient services when needed.

Switching Health Insurance: A Step-by-Step Guide to Changing Coverage

You may want to see also

Explore related products

![]()

Outpatient Services: Includes doctor visits, specialist consultations, diagnostic tests, and minor procedures not requiring hospitalization

Outpatient services encompass a broad range of medical care options that do not require hospitalization. These services are typically covered by health insurance plans, albeit with varying degrees of coverage and out-of-pocket costs. Understanding what is included in outpatient services can help individuals navigate their healthcare options more effectively.

Doctor visits are a fundamental component of outpatient services. These can include routine check-ups, consultations for specific health concerns, and follow-up appointments. Health insurance generally covers these visits, but the extent of coverage may depend on the plan's specifics, such as copays or deductibles.

Specialist consultations are another key aspect of outpatient care. These involve visits to healthcare providers who specialize in particular areas of medicine, such as cardiology, dermatology, or neurology. Insurance coverage for specialist consultations often requires a referral from a primary care physician and may be subject to higher out-of-pocket costs compared to general doctor visits.

Diagnostic tests, such as blood work, imaging studies (e.g., X-rays, MRIs), and other laboratory tests, are essential for diagnosing and monitoring various health conditions. Health insurance typically covers these tests when they are deemed medically necessary, but the coverage may vary based on the type of test and the insurance plan's provisions.

Minor procedures that do not require hospitalization, such as vaccinations, biopsies, and certain types of surgery (e.g., outpatient surgery), are also considered outpatient services. Coverage for these procedures can vary widely depending on the insurance plan, the procedure's complexity, and whether it is performed in a doctor's office or an outpatient facility.

In summary, outpatient services include a variety of medical care options that do not necessitate hospitalization, such as doctor visits, specialist consultations, diagnostic tests, and minor procedures. Health insurance coverage for these services can vary based on the plan's specifics, the type of service, and the healthcare provider. Understanding the nuances of outpatient service coverage can help individuals make informed decisions about their healthcare and manage their insurance costs more effectively.

Discover the Advantages of Health Net Health Insurance Today

You may want to see also

Explore related products

![]()

Prescription Medications: Coverage for prescribed drugs, with varying levels of copayments or coinsurance depending on the plan

Prescription medications are a critical component of healthcare, and understanding how they are covered by health insurance is essential for managing medical expenses. Coverage for prescribed drugs varies significantly depending on the insurance plan, with different levels of copayments or coinsurance. Copayments are fixed amounts paid by the insured for each prescription, while coinsurance is a percentage of the drug's cost shared between the insured and the insurer.

Insurance plans often categorize prescription drugs into tiers, with each tier having a different level of coverage. For example, generic drugs may be covered with a lower copayment, while brand-name drugs might have a higher copayment or coinsurance rate. Some plans may also have a deductible that must be met before prescription drug coverage kicks in. It's important for individuals to review their plan's formulary, which lists the covered medications and their corresponding tiers, to understand their out-of-pocket costs.

In addition to the type of medication, the pharmacy where the prescription is filled can also impact coverage and costs. Insurance plans may have preferred pharmacies or mail-order options that offer lower copayments or coinsurance rates. Furthermore, some plans may cover prescription drugs used for preventive care, such as statins for heart disease prevention, with little to no out-of-pocket cost.

Navigating prescription drug coverage can be complex, but there are resources available to help. Insurers often provide online tools or mobile apps that allow members to search for covered medications, compare costs, and track their prescription drug spending. Additionally, pharmacists can be a valuable resource in understanding coverage options and finding ways to reduce medication costs.

In conclusion, prescription medication coverage is a key aspect of health insurance, and it's crucial to understand the specifics of one's plan to effectively manage healthcare expenses. By reviewing the plan's formulary, considering pharmacy options, and utilizing available resources, individuals can make informed decisions about their prescription drug coverage and minimize their out-of-pocket costs.

Filing Health Insurance Exemption with H&R Block: A Step-by-Step Guide

You may want to see also

Explore related products

![]()

Preventive Care: Routine check-ups, vaccinations, screenings, and counseling to prevent or detect health issues early

Preventive care is a crucial aspect of maintaining good health and reducing healthcare costs in the long run. Routine check-ups, vaccinations, screenings, and counseling are all essential components of preventive care that can help detect health issues early, when they are often easier and less expensive to treat. In this section, we'll explore what preventive care services are typically covered by health insurance and why it's important to take advantage of these benefits.

One of the key benefits of health insurance is that it often covers preventive care services at little or no cost to the policyholder. This can include annual physical exams, vaccinations such as flu shots and HPV vaccines, and screenings for conditions like high blood pressure, diabetes, and certain types of cancer. Counseling services, such as those related to smoking cessation, weight management, and mental health, may also be covered. By taking advantage of these preventive care services, individuals can not only improve their overall health but also potentially avoid more costly medical treatments down the line.

It's important to note that the specific preventive care services covered by health insurance can vary depending on the policy and the insurance provider. Some policies may cover additional services, such as dental cleanings or vision exams, while others may have limitations on the frequency or type of preventive care services covered. To make the most of your health insurance benefits, it's a good idea to review your policy and talk to your healthcare provider about which preventive care services are right for you.

In addition to the financial benefits, preventive care can also have a significant impact on an individual's quality of life. By detecting health issues early, individuals can often avoid more serious complications and maintain their independence and well-being. Preventive care can also help individuals make informed decisions about their health, such as whether to pursue further testing or treatment for a particular condition.

Overall, preventive care is a valuable tool for maintaining good health and reducing healthcare costs. By understanding what preventive care services are covered by health insurance and taking advantage of these benefits, individuals can take an active role in their health and well-being.

Setting Up Medical Insurance Deductions in Sage 50

You may want to see also

Explore related products

![]()

Mental Health Services: Therapy sessions, counseling, and treatment for mental health conditions, including substance abuse disorders

Health insurance coverage for mental health services can vary widely depending on the specific plan and provider. However, most comprehensive health insurance plans will cover some form of mental health treatment, including therapy sessions, counseling, and treatment for mental health conditions such as depression, anxiety, and substance abuse disorders. It's important to note that the extent of coverage may differ based on the plan's terms and conditions.

When seeking mental health services, it's crucial to understand the difference between in-network and out-of-network providers. In-network providers have a contractual agreement with the insurance company and typically offer services at a lower cost to the insured. Out-of-network providers, on the other hand, do not have such an agreement and may charge higher rates, which could result in higher out-of-pocket expenses for the patient.

Many health insurance plans also have deductibles, copays, and coinsurance requirements for mental health services. A deductible is the amount the insured must pay out-of-pocket before the insurance company begins to cover costs. A copay is a fixed amount the insured pays for each service, while coinsurance is a percentage of the cost the insured is responsible for. It's essential to review your plan's details to understand these financial responsibilities.

Some plans may also have limitations on the number of therapy sessions or counseling appointments covered per year. Additionally, certain treatments or medications may require prior authorization from the insurance company before they are covered. This means that the healthcare provider must submit a request to the insurance company, outlining the medical necessity of the treatment, before the patient can receive coverage.

In the case of substance abuse disorders, coverage may include detoxification, inpatient and outpatient rehabilitation, and ongoing counseling and support. However, the specific services covered and the duration of treatment may vary based on the insurance plan and the individual's needs.

To maximize your insurance coverage for mental health services, it's important to choose a plan that aligns with your needs and to carefully review the terms and conditions. If you're unsure about your coverage, reach out to your insurance provider directly for clarification. Remember, seeking mental health treatment is a crucial step towards overall well-being, and understanding your insurance coverage can help ensure that you receive the care you need without facing unexpected financial burdens.

Choosing the Right International Health Insurance: A Comprehensive Guide

You may want to see also

Frequently asked questions

Health insurance typically covers a range of medical services including doctor visits, hospital stays, emergency room visits, prescription medications, and preventive care such as vaccinations and screenings.

Many health insurance plans do not cover dental and vision care, but some plans may offer these benefits as optional add-ons or through separate policies.

Yes, health insurance plans often have out-of-pocket costs such as deductibles, copayments, and coinsurance. These costs are paid by the insured individual at the time of service.

In-network providers are healthcare providers who have a contract with the health insurance company to provide services at a discounted rate. Out-of-network providers do not have such a contract and may charge higher rates for their services.

To find out what specific charges your health insurance covers, you can review your plan's benefits summary or contact your insurance company directly. They can provide you with detailed information about your coverage and any associated costs.